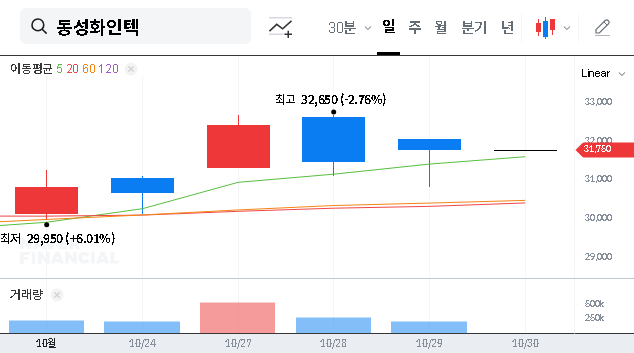

The DONGSUNG FINETEC stock has entered a period of significant turbulence, capturing the attention of investors following a critical disclosure. The company announced it is subject to a substantive review for listing eligibility, casting a shadow of uncertainty over its future on the stock exchange. This development has understandably created concern, but a deeper look reveals a complex situation where regulatory scrutiny clashes with robust corporate performance.

This comprehensive analysis will dissect the DONGSUNG FINETEC listing eligibility review, explore the company’s surprisingly strong fundamentals, outline potential future scenarios, and provide a prudent investment strategy for navigating this volatile period. For those invested or considering an investment, understanding these dynamics is crucial.

The Critical Announcement: What is a Listing Eligibility Review?

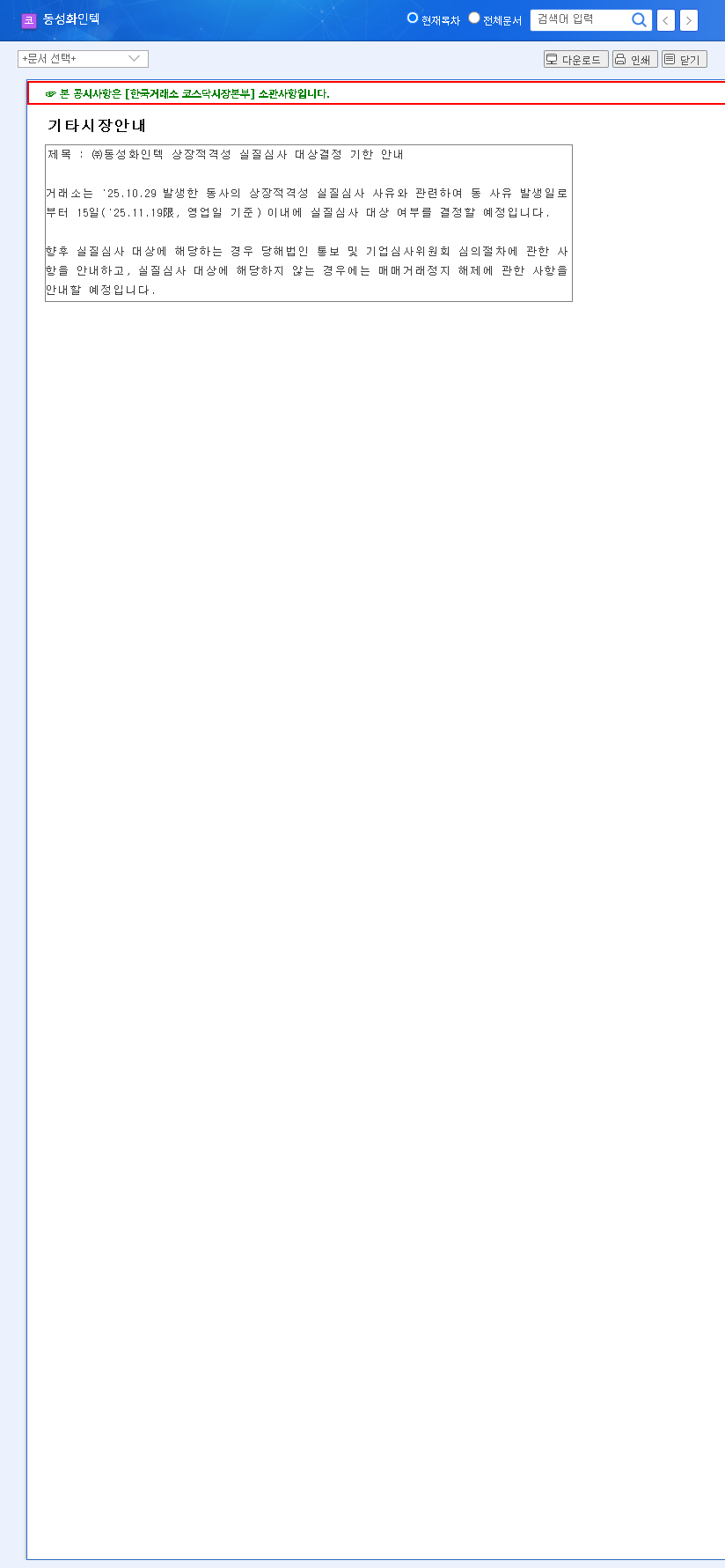

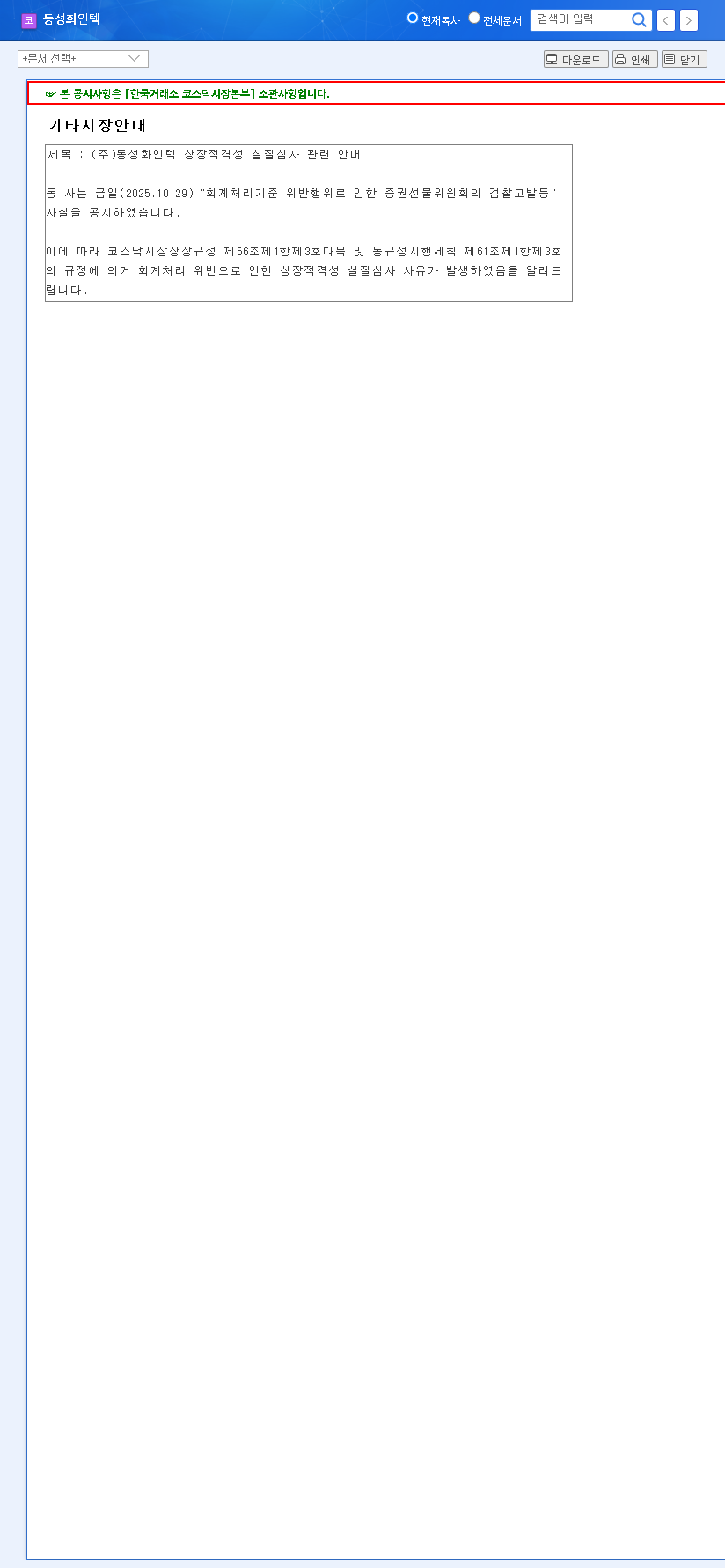

On October 29, 2025, DONGSUNG FINETEC CO., Ltd disclosed that an event had triggered a substantive review of its listing eligibility by the Korea Exchange (KRX). According to the official filing, a decision on whether the company is subject to this formal review will be made by November 19, 2025. The trigger for this review was detailed in an official disclosure filed with the Financial Supervisory Service (Source: DART Report).

A listing eligibility review is a procedural safeguard used by stock exchanges to assess whether a company continues to meet the criteria required to be publicly traded. This process examines factors like financial stability, management transparency, and corporate governance to protect investors and maintain market integrity. The mere initiation of this process introduces significant uncertainty, which almost always results in a negative short-term impact on the stock price as investors react to the potential risks of trading suspension or, in the worst-case scenario, delisting.

Strong Fundamentals Amidst the Storm

Ironically, this regulatory challenge comes at a time when DONGSUNG FINETEC’s underlying business is performing exceptionally well. The discrepancy between the company’s operational health and its market valuation presents a classic dilemma for investors. A detailed DONGSUNG FINETEC analysis of its fundamentals is essential.

Stellar H1 2025 Financial Performance

The company’s financial results for the first half of 2025 were nothing short of impressive, showcasing robust growth across the board:

- •Revenue: Increased by 32.7% year-on-year to KRW 365.68 billion.

- •Operating Profit: Surged by 30.4% to KRW 29.46 billion.

- •Net Income: Grew by an astounding 103.9% to KRW 20.05 billion.

This growth is primarily driven by the strong performance of its core PU (polyurethane) insulation material business, which is a critical component for LNG carriers. Furthermore, the company’s financial health has improved, with its debt-to-equity ratio falling to 70.7% and its cash reserves growing to KRW 93.35 billion, indicating enhanced stability and resilience.

The key challenge for the DONGSUNG FINETEC stock is that market sentiment is currently driven by regulatory risk, not by the company’s strong intrinsic value or positive growth trajectory.

Future Outlook: The November 19th Turning Point

The market is holding its breath for the November 19, 2025 announcement. This date will serve as a major catalyst, and the outcome will likely dictate the direction of the DONGSUNG FINETEC stock for the foreseeable future. There are two primary scenarios:

- •Scenario 1 (Positive): Exclusion from Review. If the KRX determines that a full substantive review is not necessary, the cloud of uncertainty will lift. This would likely trigger a rapid price recovery as investor confidence is restored.

- •Scenario 2 (Negative): Deemed Subject to Review. If the company is formally subjected to the review, it could face a prolonged trading suspension. This would amplify uncertainty and likely lead to further stock price declines.

Long-term, provided the company successfully navigates this regulatory hurdle, its prospects remain bright. The global demand for LNG is expanding, a trend expected to continue for years, as noted by industry authorities like the International Energy Agency (IEA). This directly benefits DONGSUNG FINETEC’s core business. For more on local market rules, see our guide on Korean Stock Market Regulations.

A Prudent Investment Strategy for Investors

In this environment, a cautious and informed DONGSUNG FINETEC investment strategy is paramount. Hasty decisions based on fear or speculation can be costly. Consider the following action plan:

- •Monitor Official Information: Pay close attention to official disclosures from the company and the KRX. Avoid rumors and focus on verified facts leading up to the November 19 decision.

- •Assess Risk Tolerance: Evaluate your personal capacity to handle high volatility. This is not a stock for the risk-averse until the review’s outcome is clear.

- •Focus on Risk Management: Prepare for potential short-term price swings. This may involve setting stop-loss orders or ensuring your portfolio is not overly concentrated in this single stock.

- •Re-evaluate Post-Announcement: Once the results are public, re-evaluate the company’s position. A positive outcome could present a buying opportunity based on its strong fundamentals, while a negative one would require a more defensive strategy.

Frequently Asked Questions (FAQ)

Q1: What exactly is the listing eligibility review for DONGSUNG FINETEC?

A1: It’s a formal process by the Korea Exchange to verify if the company still meets the standards for being publicly listed, focusing on aspects like financial health and corporate governance. The initial decision on whether to proceed with a full review is expected by November 19, 2025.

Q2: How is the company performing financially?

A2: Exceptionally well. For the first half of 2025, DONGSUNG FINETEC reported significant year-on-year growth, with revenue up 32.7% and net income soaring 103.9%, highlighting its strong operational fundamentals.

Q3: How will the review’s outcome affect the DONGSUNG FINETEC stock price?

A3: If the company is excluded from the review, the stock is likely to recover quickly as uncertainty is removed. If it is subjected to a full review, extended trading suspensions and further price declines are highly probable.

Q4: What is the recommended course of action for investors?

A4: A cautious approach is vital. Investors should closely monitor the official announcement on November 19, manage their risk exposure, and be prepared to re-evaluate their investment strategy based on the outcome.