Investors are taking a closer look at Misto Holdings Corporation (081660) following the announcement of a new quarterly dividend. This move signals a commitment to shareholder returns, but it arrives amidst a complex financial landscape for the company. While its Acushnet segment shows impressive growth, the struggling Misto segment raises critical questions about long-term sustainability. This comprehensive analysis will break down the latest Misto Holdings dividend news, dissect the company’s fundamentals, and provide a strategic outlook to help inform your investment decisions.

Is this dividend a sign of robust financial health, or a strategic move to placate investors while navigating internal challenges? Let’s delve into the data.

The Dividend Announcement: A Signal of Confidence?

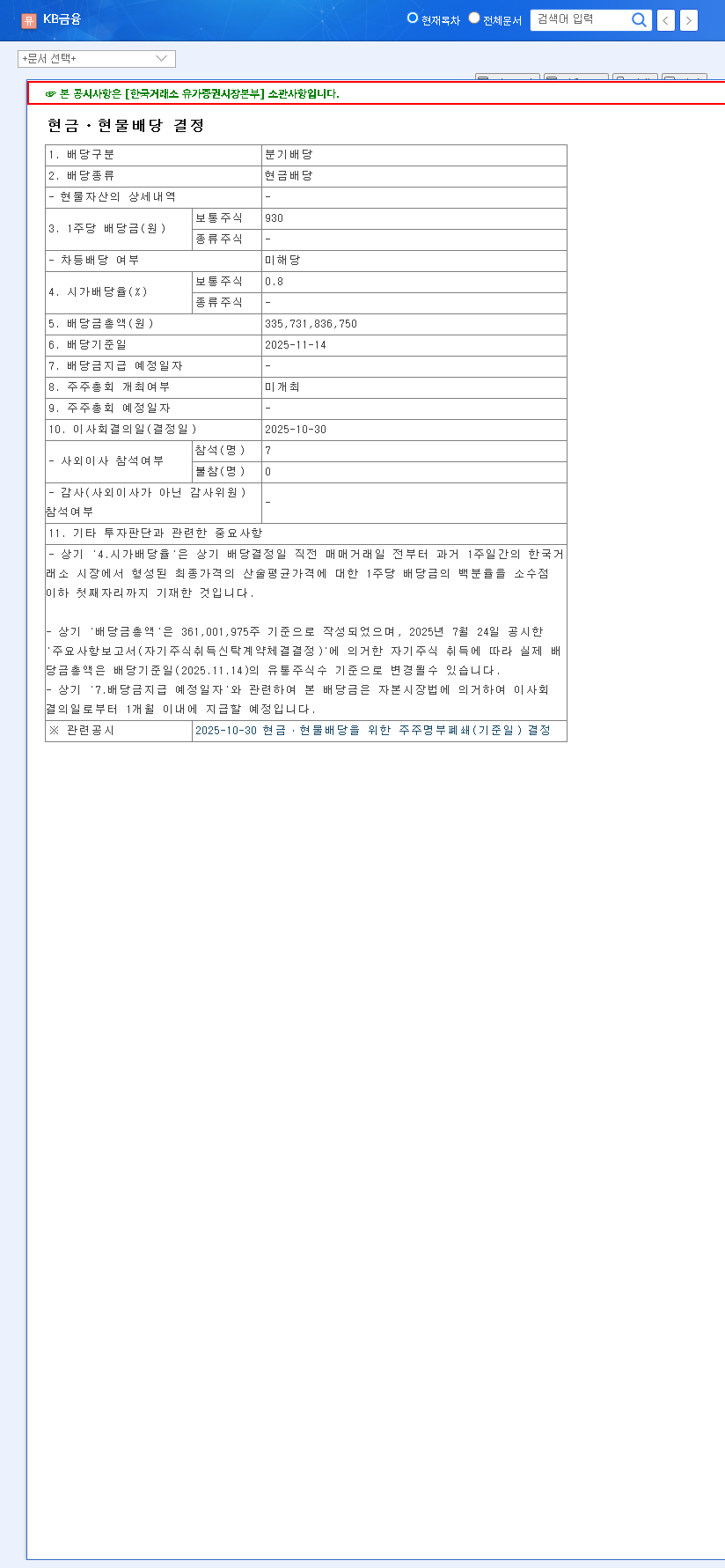

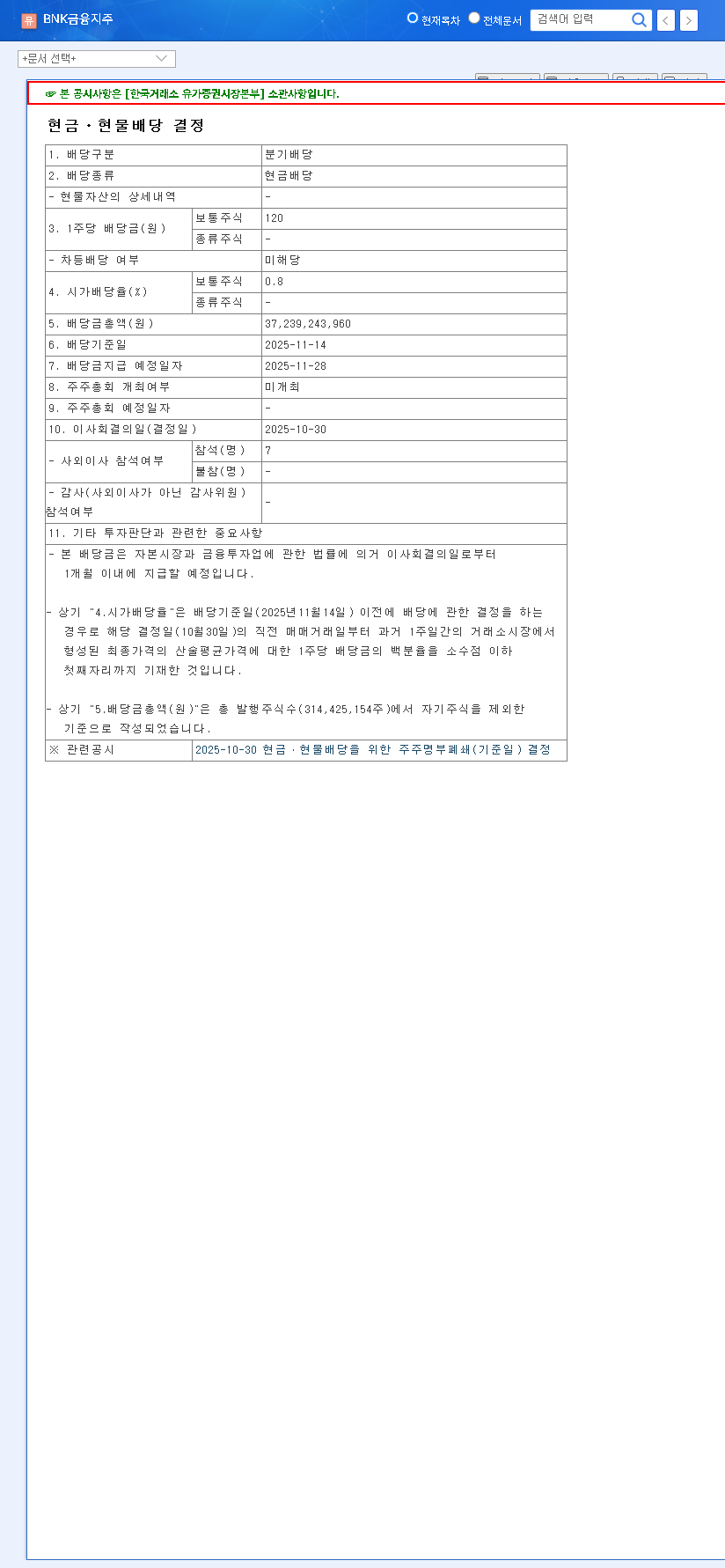

On November 12, 2025, Misto Holdings Corporation confirmed its decision to issue a cash quarterly dividend of 940 KRW per common share for the period ending September 30, 2025. This action is a key part of the company’s multi-year shareholder return policy, aiming to distribute 500 billion KRW between 2025 and 2027. This decision, detailed in the company’s Official Disclosure (Source: DART), suggests management’s confidence in its cash flow, but a deeper look at the fundamentals is essential.

Deep Dive: Misto Holdings’ H1 2025 Financial Health

A company’s ability to sustain dividends is directly tied to its financial performance. The H1 2025 report for Misto Holdings Corporation reveals a story of divergence and resilience.

The Tale of Two Segments: Acushnet vs. Misto

The company’s performance is sharply divided between its two primary business units. The Acushnet segment, the powerhouse behind the globally recognized Titleist golf brand, is thriving. It posted an 8.5% increase in revenue, driving the company’s consolidated revenue up by 4.5% year-over-year to 2.4652 trillion KRW. This segment is the engine of growth and profitability.

Conversely, the Misto segment has faced significant headwinds, largely due to weakening global consumer sentiment. This resulted in a stark 18.6% decline in revenue. While it’s a positive note that the Misto segment managed to turn a small profit compared to a major loss in the previous year, its underperformance remains the primary risk factor for the entire corporation.

Analyzing the Balance Sheet and Cash Flow

Misto Holdings maintains a stable financial position with a debt-to-equity ratio of 106.7%. However, operating cash flow saw a significant 49.6% decrease YoY to 99.4 billion KRW. This dip is directly attributable to the revenue decline and working capital challenges within the struggling Misto segment. While the dividend payment is currently manageable, a continued decline in cash flow could jeopardize future shareholder returns. For more on how to interpret these figures, see our Guide to Analyzing Corporate Financial Reports.

Investor Implications: Weighing the Pros and Cons

For current and prospective investors in 081660 stock, the dividend decision presents both opportunities and risks.

Key Positives for Misto Holdings Corporation

- •Attractive Dividend Yield: The dividend offers an approximate yield of 2.38% (based on recent prices), which is appealing to income-focused investors. Learn more about calculating dividend yield at Investopedia.

- •Robust Acushnet Performance: The continued strength of the Acushnet segment provides a stable foundation for revenue and profit, currently funding the dividend.

- •Strong Shareholder Return Policy: The dividend is part of a clear, long-term commitment to return value to shareholders, which can support the stock price.

- •Positive ESG Ratings: The company’s inclusion in indices like the FTSE4Good highlights a commitment to sustainability, which is increasingly important to institutional investors.

Significant Risks and Headwinds to Consider

- •Misto Segment Drag: The persistent underperformance of the Misto segment is the single largest threat. If it doesn’t recover, it could drain resources and threaten the sustainability of the dividend policy.

- •Macroeconomic Volatility: Global economic slowdowns, rising interest rates, and foreign exchange fluctuations pose a risk to both business segments.

- •Decreased Operating Cash Flow: The sharp drop in cash from operations is a red flag that needs to be monitored closely in upcoming quarters.

Strategic Outlook: Crafting Your Investment Thesis

Misto Holdings Corporation is a tale of two companies under one roof. The dividend is a vote of confidence, but its long-term viability hinges on a single question: can the Misto segment be fixed? Investors should build their strategy around monitoring key performance indicators.

Keep a close watch on the revenue and profit margin trends for the Misto segment in subsequent quarterly reports. Any sign of a sustained turnaround could be a powerful catalyst for the stock. In contrast, further deterioration may force management to reconsider its capital allocation, potentially impacting future dividends and buybacks. For now, the strength of the Acushnet segment provides a valuable cushion, but it cannot carry the entire company indefinitely.

Disclaimer: This article is for informational purposes only and does not constitute investment advice. All investment decisions should be made based on your own research and judgment.