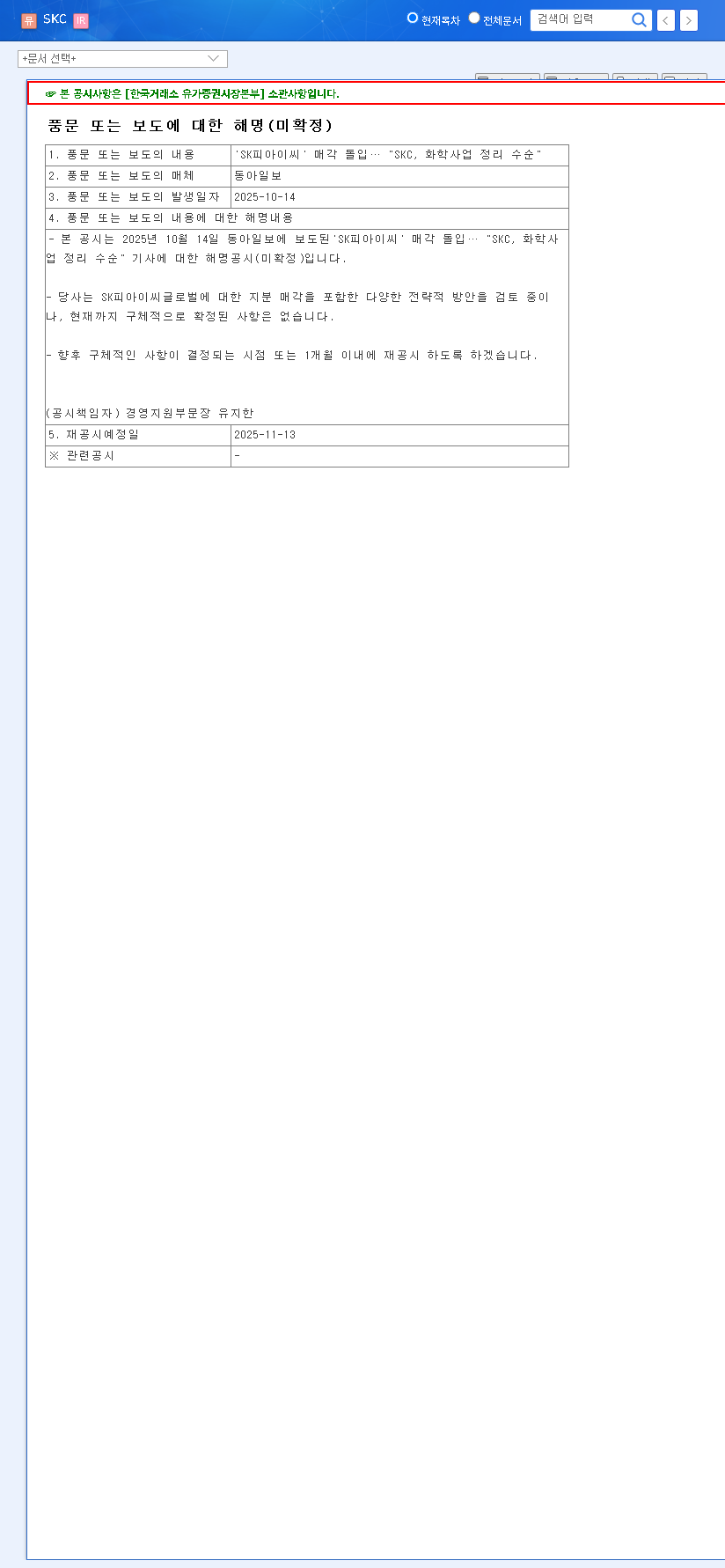

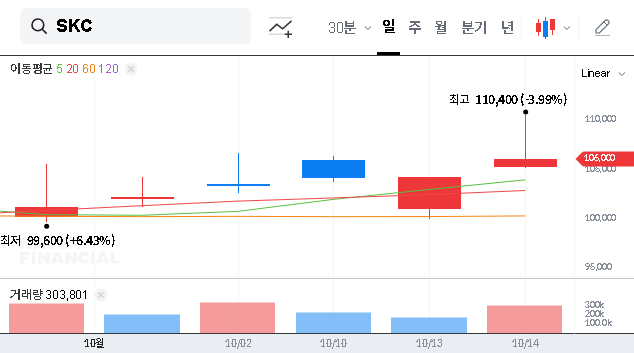

Recent market reports surrounding the potential SKC LTD SK PIC Global divestment have sparked significant discussion among investors. This strategic move, first highlighted by Dong-A Ilbo on October 14, 2025, is widely seen as a pivotal step in SKC LTD’s overarching plan to streamline its chemical business and double down on high-growth sectors. This comprehensive analysis breaks down the rumors, examines the company’s fundamentals, and provides a clear, actionable perspective for anyone considering an SKC LTD investment.

Understanding this potential SKC LTD divestment is crucial, as it offers a window into the company’s future trajectory. We will explore both the promising opportunities and the inherent risks to help you make well-informed financial decisions.

The SK PIC Global Divestment Rumors: What We Know

The initial report claimed that the SKC LTD SK PIC Global sale was actively underway as part of a broader consolidation of the SKC LTD chemical business. In response, SKC LTD issued a clarification, stating it is reviewing various strategic options for its stake in SK PIC Global, but no final decision has been made. The company has committed to providing a further update once details are confirmed or within one month. (Source: Official Disclosure).

SKC LTD Fundamental Analysis (Based on H1 2025 Report)

To grasp the full context of this move, a deep dive into SKC LTD’s current financial and strategic state is essential. The company is in the midst of a significant transformation, pivoting away from legacy operations to secure its position in next-generation industries.

Business Restructuring and Core Focus

SKC LTD has been methodically divesting non-core assets to sharpen its focus on three key pillars: secondary battery materials (copper foil, silicon anode), advanced semiconductor materials, and eco-friendly solutions. This strategic realignment is designed to enhance competitiveness and unlock long-term value in high-growth markets.

Financial Health and Capital Allocation

To fuel this expansion, SKC has been actively raising capital. As of June 30, 2025, its debt-to-equity ratio improved to a healthy 76.93%. However, this aggressive investment has come at a cost. The company reported a significant consolidated net loss in the first half of the year, driven by large-scale capital expenditures and weakening profitability in its traditional chemical segments. This financial pressure likely adds urgency to the SKC LTD SK PIC Global divestment considerations.

Market Environment and Risk Management

Each of SKC’s core businesses operates in a dynamic environment:

- •Secondary Battery Materials: The electric vehicle market underpins gradual but steady demand for copper foil. However, SKC must navigate increasing competition from global players. For more on this sector, read our complete guide to battery material stocks.

- •Semiconductor Materials: With the boom in AI, the long-term outlook is robust. Yet, the industry is famously cyclical, exposing SKC to economic volatility, as noted by analysts at high-authority sites like Reuters Business.

- •Chemical Business: The markets for Propylene Oxide (PO) and Propylene Glycol (PG) remain steady but are highly susceptible to downturns in manufacturing and industrial demand.

Impact Analysis: How the Sale Could Reshape SKC LTD

The rumored SKC LTD divestment carries significant potential consequences, both positive and negative, that require careful consideration in any SKC LTD stock analysis.

Potential Upsides: A Leaner, More Focused Company

- •Accelerated Core Business Focus: Selling SK PIC Global would free up capital and management bandwidth to pour into the high-growth battery and semiconductor divisions.

- •Improved Financial Structure: Proceeds could be used to pay down debt or fund critical R&D, directly addressing the recent net loss and improving the balance sheet.

- •Corporate Re-evaluation: Shifting away from the legacy chemical business could help the market re-evaluate SKC LTD as a forward-looking technology materials company, potentially unlocking a higher valuation multiple.

Potential Downsides and Inherent Risks

- •Market Uncertainty: As the deal is unconfirmed, the ensuing speculation can lead to short-term stock price volatility.

- •Loss of Profit Contribution: If SK PIC Global is a significant contributor to revenue, its sale could create a short-term earnings gap that the growth businesses may not immediately fill.

- •Execution Risk: A poorly executed sale or a lower-than-expected price could limit the financial benefits and disappoint the market.

Investment Opinion: Neutral. While SKC LTD’s long-term pivot towards future-proof industries is strategically sound, the short-term uncertainties tied to the SKC LTD SK PIC Global divestment and current financial performance warrant a cautious, observant approach.

Conclusion and Investor Recommendations

The potential sale of SK PIC Global is a defining moment for SKC LTD. It represents a trade-off: sacrificing a stable, cash-generating asset for a more aggressive, focused push into higher-growth markets. Long-term, this strategy is commendable. Short-term, investors must remain vigilant.

Key Recommendations:

- •Monitor Official Disclosures: Pay close attention to SKC LTD’s follow-up announcements regarding the sale’s progress and terms.

- •Analyze Core Business Performance: Track the profitability and market share gains in the secondary battery and semiconductor segments to see if the investment is paying off.

- •Assess Macroeconomic Factors: Keep an eye on exchange rates, interest rates, and commodity prices, as they directly impact SKC’s global operations and profitability.