The latest ktcs corporation earnings report for Q3 2025 has landed, leaving investors at a critical crossroads. After a spectacular turnaround in the first half of the year that fueled significant optimism, the key question now is whether the company can sustain its upward trajectory. The preliminary figures present a complex narrative of continued growth tempered by emerging challenges.

This comprehensive ktcs Q3 2025 analysis delves into the official financial disclosure, breaking down performance metrics, business segment dynamics, and the broader market environment. Our goal is to equip you with the crucial insights needed to evaluate the true value of ktcs stock and formulate a well-informed investment strategy.

Q3 2025 Earnings: A Story of Diverging Trends

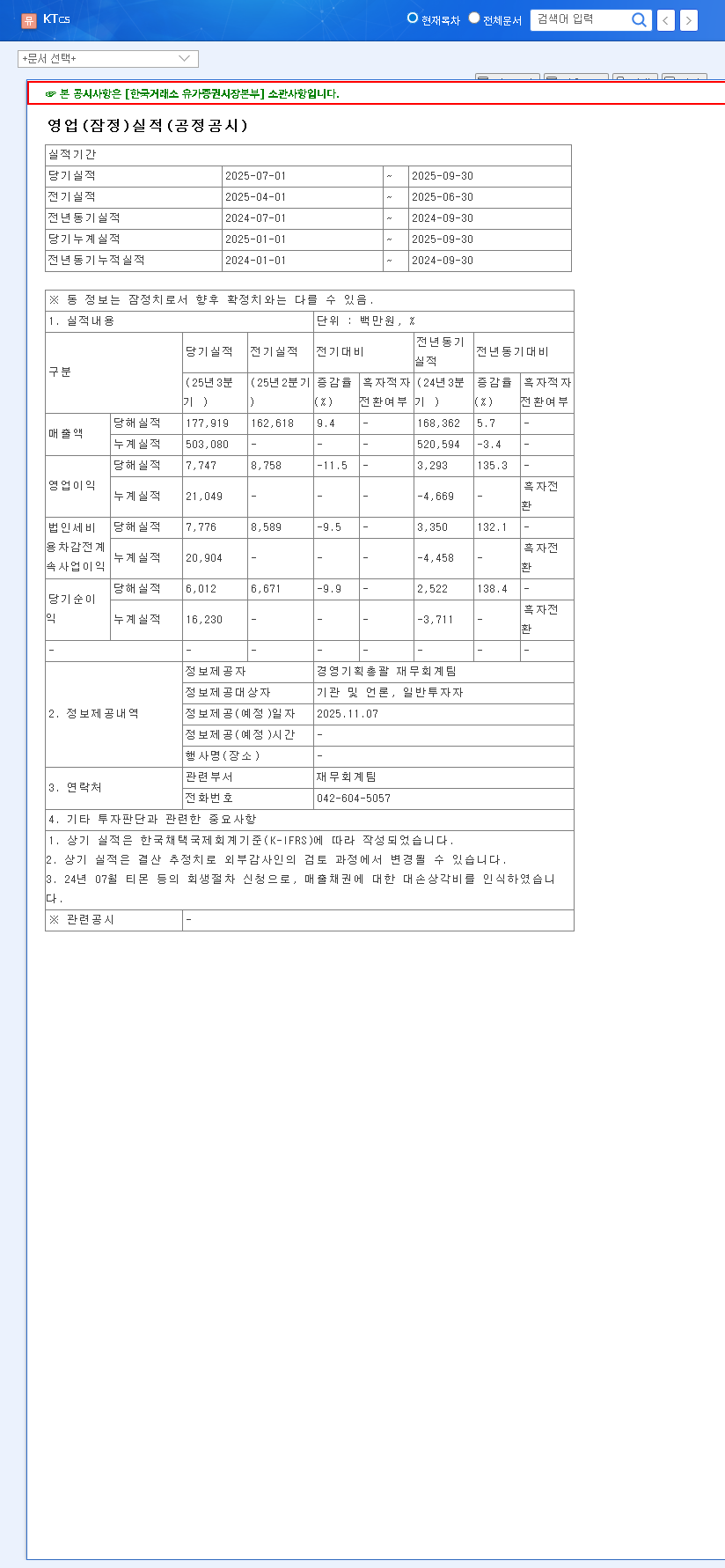

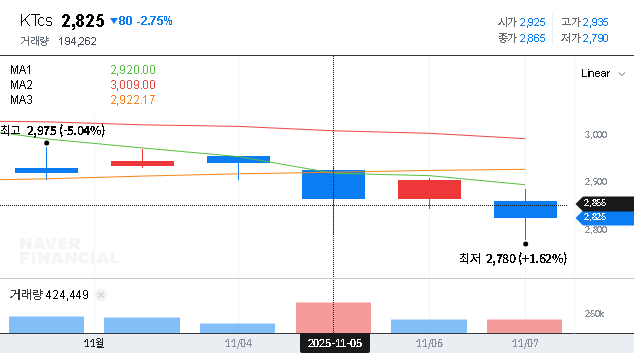

On November 7, 2025, ktcs corporation released its preliminary Q3 earnings, which painted a mixed picture. The top-line revenue showed healthy growth, but profitability metrics took a step back from the previous quarter’s highs. You can view the complete filing here: Official Disclosure.

While revenue climbed 8.4% quarter-over-quarter to KRW 268.9 billion, operating profit saw a significant 28.1% decrease to KRW 9.2 billion. This signals a potential pause in the powerful profitability momentum built during the first half of 2025.

Quarterly Performance at a Glance

- •Q3 2025: Revenue KRW 268.9B, Operating Profit KRW 9.2B

- •Q2 2025: Revenue KRW 248.0B, Operating Profit KRW 12.8B

- •Q1 2025: Revenue KRW 235.2B, Operating Profit KRW 6.6B

This data highlights that while year-over-year performance remains strong, the sequential decline in profitability warrants a closer look into the company’s operational drivers and cost structures.

Dissecting the Business: The AI Engine vs. Legacy Drag

The first half of 2025 was a testament to ktcs corporation’s strategic pivot. Despite lower overall revenue, operating profit surged an incredible 177.5% year-over-year. This success was driven by a deliberate shift away from lower-margin businesses towards high-profit services, particularly in the tech space.

The Rise of the AI Contact Center

The star of the show is the company’s transformation into an AI Contact Center (AICC) powerhouse. The commercialization of its proprietary ‘HiQri’ AICC solution is proving to be a powerful growth engine. This focus on AI-driven customer service is not just a trend; it’s a fundamental shift that enhances efficiency and scalability, directly boosting the bottom line. This aligns with broader market trends where automation is key, as noted in reports by major consulting firms like Gartner on customer service AI.

Persistent Challenges in Distribution

In stark contrast, the legacy distribution business continues to face significant headwinds. Market saturation and intense competition have led to a persistent slump in this segment. The Q3 results do not show any signs of a meaningful turnaround, and this continues to be a drag on the company’s overall performance. Investors should monitor whether ktcs decides to divest or further restructure this part of the business.

Investment Outlook: Balancing Positives with Caution

Considering the full picture of the ktcs corporation earnings, our investment opinion remains a cautious ‘Neutral’. The company’s future hinges on its ability to scale its high-growth AI business faster than its legacy segments decline.

Key Factors to Watch

- •Bull Case: The AI Contact Center business continues its rapid expansion, securing major new clients and driving margin improvement. The company successfully manages costs, returning to a path of quarter-over-quarter profit growth.

- •Bear Case: Competition in the AI market intensifies, slowing growth and compressing margins. The distribution business continues to decline, offsetting gains elsewhere. Macroeconomic pressures impact client spending on contact center services.

Strategic Considerations

For short-term investors, it is prudent to monitor the stock’s reaction to these earnings and await the Q4 results for a clearer trend. For long-term investors, the focus should be on the tangible growth of the AICC business and any strategic moves to address the underperforming distribution segment. Our internal analysis suggests keeping an eye on their long-term corporate strategy updates.

Frequently Asked Questions (FAQ)

Q1: What were the main takeaways from ktcs corporation’s Q3 2025 earnings?

The key takeaway is mixed performance. Revenue grew to KRW 268.9 billion, but operating profit and net income declined compared to the previous quarter, indicating a slowdown in the strong profitability trend seen in H1.

Q2: What is driving ktcs corporation’s business transformation?

The core of the transformation is a strategic shift towards its high-margin AI Contact Center (AICC) business. By focusing on technology and efficiency, the company is securing new growth engines to offset declines in its traditional distribution segment.

Q3: What are the primary risks for investors considering ktcs stock?

Major risks include fierce competition in the AI market, a potential slowdown in client demand due to macroeconomic factors, and the ongoing slump in the company’s distribution business acting as a drag on overall financial health.