The latest LOTTE SHOPPING Q2 2025 earnings report has sent a significant chill through the investment community. Preliminary results reveal not just a minor miss, but a profound underperformance, culminating in a staggering net loss that has amplified concerns about the company’s fundamental health and strategic direction. This is more than a temporary setback; it’s a clear crisis signal that demands a thorough review.

For investors holding or considering a position in LOTTE SHOPPING, this detailed analysis will dissect the disappointing figures, explore the deep-seated structural issues and macroeconomic headwinds at play, and provide a clear-eyed view of the future outlook. We’ll examine why these results justify a cautious, if not outright bearish, stance on the stock.

The Unvarnished Truth of the Q2 2025 ‘Earnings Shock’

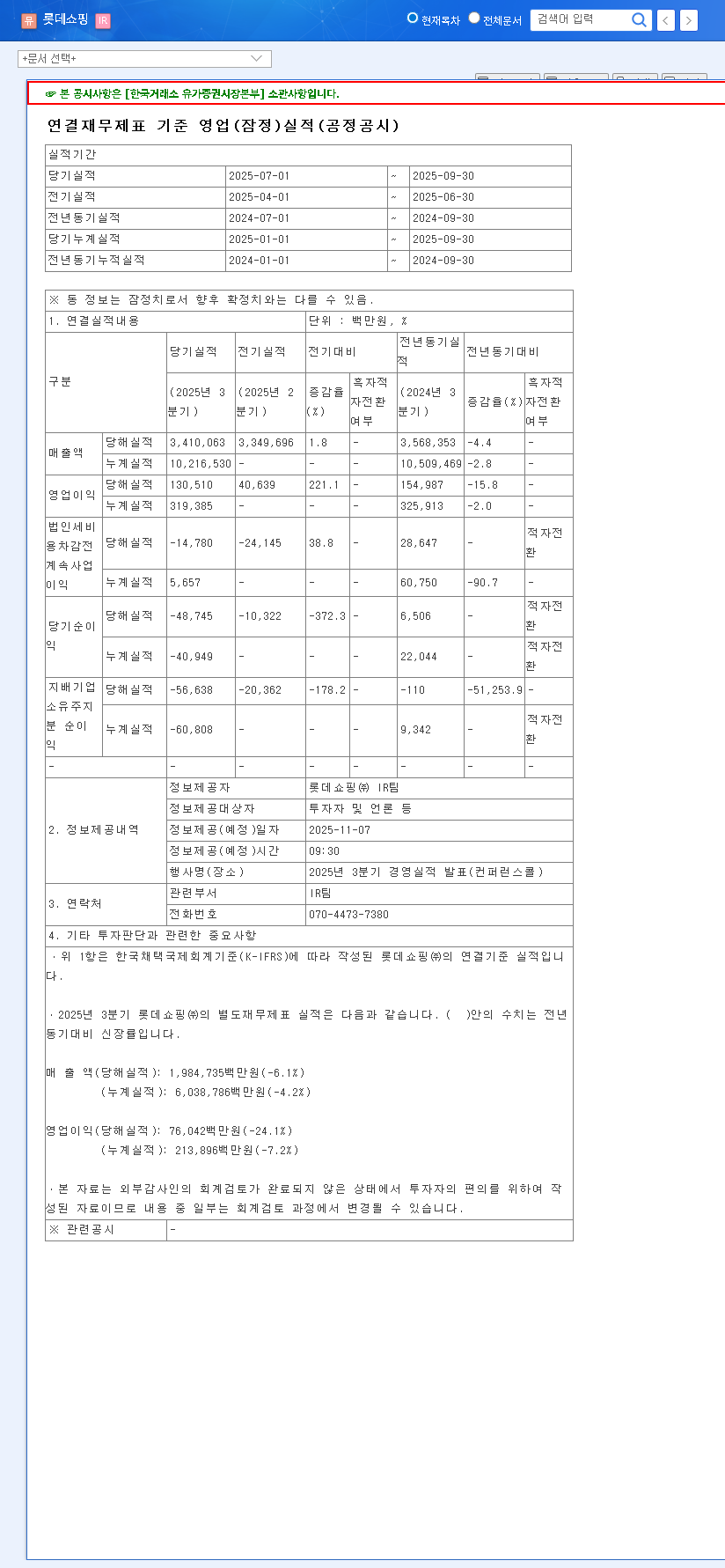

LOTTE SHOPPING CO.,LTD. released preliminary Q2 2025 earnings that fell dramatically short of consensus estimates across all key metrics. This significant miss suggests that the challenges facing the company are more severe than previously anticipated. The official disclosure, available on DART (Source), confirms the grim reality.

Key Performance Indicators vs. Market Expectations

- •Revenue: Reported at KRW 3.4101 trillion, a 2.85% miss compared to the market expectation of KRW 3.5104 trillion. This signals weakening top-line growth and potential market share erosion.

- •Operating Profit: Came in at KRW 130.5 billion, a substantial 7.71% below the expected KRW 141.4 billion, pointing to deteriorating operational efficiency and margin pressure.

- •Net Income: The most alarming figure was a net loss of KRW 56.6 billion. This starkly contrasts with market projections of a KRW 42.3 billion profit, highlighting severe financial strain from non-operating factors.

Root Causes: A Perfect Storm of Internal and External Pressures

This poor LOTTE SHOPPING performance isn’t an isolated event. It is the culmination of long-standing internal weaknesses being mercilessly exposed by a harsh macroeconomic environment. A comprehensive LOTTE SHOPPING stock analysis must consider these intertwined factors.

Persistent Underperformance in Core Business Segments

- •Discount Store Division: This segment continues to be a major drag, bleeding losses without a clear turnaround strategy. The inability to compete with agile online players and more efficient physical retailers remains a core structural problem.

- •E-commerce Division: Despite significant investment and efforts to stem the bleeding, the e-commerce arm remains unprofitable. Securing a viable growth engine in a hyper-competitive market has proven elusive, raising questions about investment efficiency and long-term strategy.

- •Department Store Division: Traditionally the crown jewel, this division’s solid performance is no longer enough to offset the heavy losses elsewhere. The overall negative results suggest even this reliable pillar may be facing headwinds amidst weakening consumer sentiment.

Vulnerable Financials Meeting Macroeconomic Headwinds

With a high debt-to-equity ratio of 129%, LOTTE SHOPPING entered this period of economic turmoil on shaky ground. The current global financial climate, as reported by sources like Reuters, is exacerbating this fragility.

- •Currency & Interest Rate Pain: A weak Korean Won (exceeding KRW 1,400/USD) and persistently high benchmark interest rates are inflating the cost of servicing foreign currency debt. This is a primary driver of the massive LOTTE SHOPPING net loss.

- •Soaring Operational Costs: Rising international oil prices and volatile shipping costs directly translate to higher logistics expenses, further squeezing already thin margins.

The Q2 2025 results are a clear verdict: LOTTE SHOPPING’s chronic internal issues are now colliding with an unforgiving external environment, creating a perilous situation for investors.

Investment Thesis: A ‘Sell’ Recommendation and Outlook

Given the severity of the LOTTE SHOPPING Q2 2025 earnings, the path forward appears fraught with risk. The company stands at a critical juncture where deep, decisive action is required to avoid further deterioration. However, the short-term outlook is overwhelmingly negative. Learn more about market trends in our comprehensive guide to the Korean retail sector.

Rationale for the ‘Sell’ Recommendation

- •Deepening Structural Flaws: The lack of a turnaround in key loss-making divisions indicates chronic problems that are far from being solved.

- •Hostile Macro Environment: High interest rates and currency volatility will continue to weigh heavily on the company’s fragile balance sheet.

- •Eroding Investor Confidence: This earnings shock will likely lead to analyst downgrades and a significant decline in investor sentiment, putting sustained downward pressure on the stock price.

For current shareholders, this is a moment to seriously reconsider your position. For those considering a new LOTTE SHOPPING investment, the risk-reward profile is highly unfavorable at this time. Caution is strongly advised.

Frequently Asked Questions

Q1: How did LOTTE SHOPPING’s Q2 2025 preliminary results fare?

A1: The results were extremely poor. LOTTE SHOPPING reported revenue of KRW 3.4101 trillion and operating profit of KRW 130.5 billion, both significantly missing market expectations. Most critically, it posted a large net loss of KRW 56.6 billion.

Q2: What are the main reasons for this poor performance?

A2: The underperformance stems from a combination of persistent losses in its discount store and e-commerce divisions, a high debt-to-equity ratio (129%), and adverse macroeconomic factors like high interest rates and a weak currency.

Q3: What is the current investment opinion on LOTTE SHOPPING?

A3: Due to the company’s deepening structural weaknesses, macroeconomic vulnerability, and cratering investor sentiment, a ‘Sell’ recommendation is advised. New investments are considered highly risky.

Disclaimer: This analysis is based on preliminary earnings data and public information. It is not an official investment recommendation. All investment decisions are the sole responsibility of the investor.