A major development is casting a new light on KOREAN AIR LINES stock as reports surface about its potential involvement in a massive ₩3 trillion national defense initiative. The project in question involves sophisticated airborne control aircraft, a move that could signal a significant strategic shift for the aviation giant. This analysis delves into the official company disclosure, the potential financial upside, and the inherent risks for investors eyeing this new chapter for Korean Air.

We will break down what this airborne control aircraft project entails, evaluate the short and long-term implications for the company’s valuation, and outline a prudent investment strategy based on the available information. Is this a catalyst for sustained growth or a speculative venture still shrouded in uncertainty?

The Disclosure: Unpacking the ₩3 Trillion Opportunity

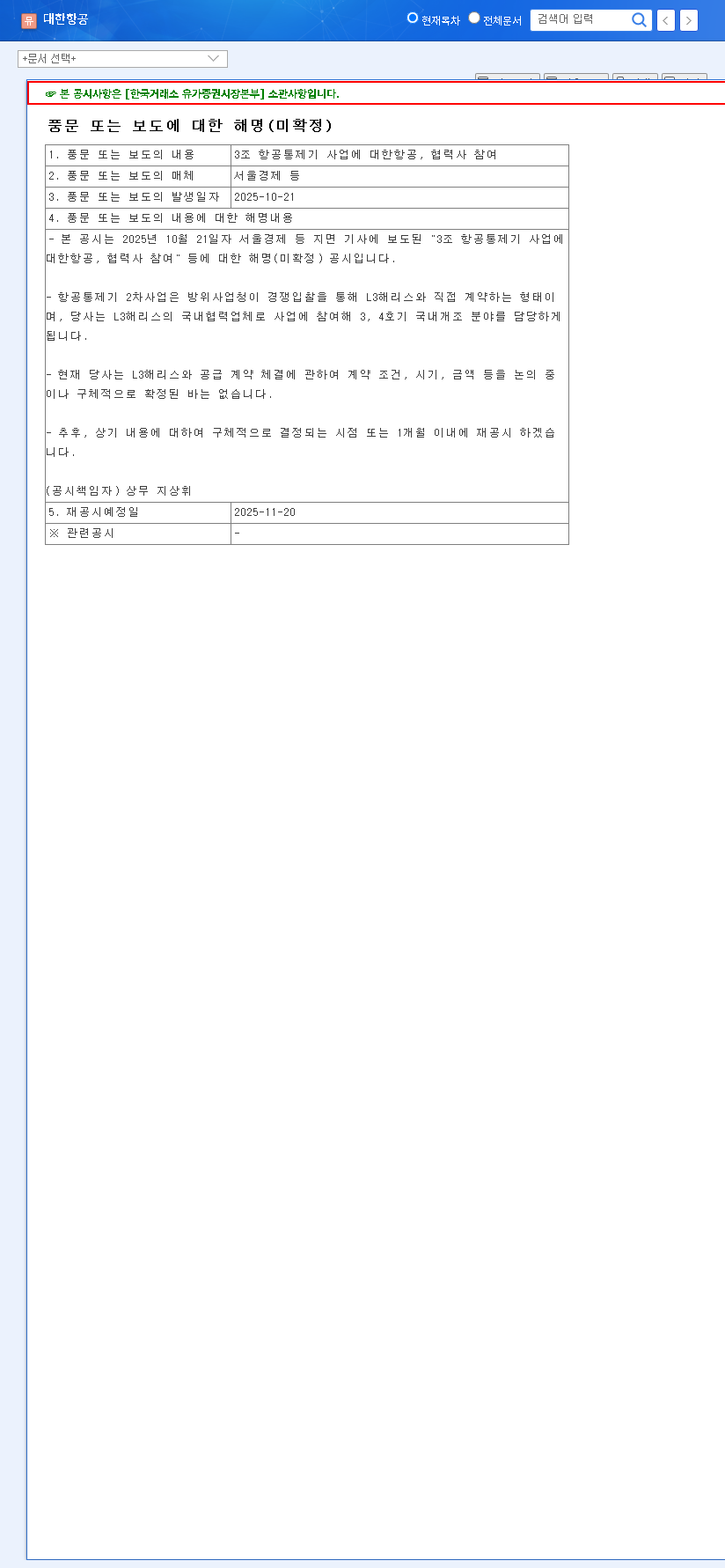

On October 21, 2025, news outlets began reporting that KOREAN AIR LINES was poised to partner in the second phase of a major defense acquisition. In response, the company issued a clarification to address the speculation. The core of the announcement reveals a potential partnership with a global defense technology leader, L3Harris, for the domestic modification of the 3rd and 4th airborne control aircraft for the Defense Acquisition Program Administration (DAPA).

KOREAN AIR LINES has officially stated that while a supply contract with L3Harris is under discussion, crucial details such as contract terms, timing, and financial scope are not yet confirmed. The company has committed to a re-disclosure by November 20, 2025.

This ‘unconfirmed’ status is critical. While the news validates a new business opportunity, it also introduces a layer of uncertainty that investors must navigate carefully. The company’s clarification can be viewed in full via its Official Disclosure (DART).

Analyzing the Impact on KOREAN AIR LINES Stock

Prior to these reports, market expectations for KOREAN AIR LINES’ involvement in a project of this nature were minimal. Therefore, this development should be analyzed as a new, potential catalyst rather than an impact on existing business fundamentals. We can assess the potential effects from both short-term and long-term perspectives.

Short-Term: A Mix of Opportunity and Caution

In the immediate term, the news flow is a net positive for investor sentiment. It highlights the company’s technical capabilities and opens the door to a lucrative new sector. However, the unconfirmed nature of the deal will likely temper any significant, sustained rally in KOREAN AIR LINES stock until concrete details emerge.

- •Positive Catalyst: The prospect of a large-scale, multi-trillion Won KAL defense contract can generate excitement and attract speculative interest.

- •Credibility Boost: Being considered for such a high-tech project validates KOREAN AIR LINES’ aerospace engineering and maintenance (MRO) divisions.

- •Key Risk: The ‘unconfirmed’ status is the primary headwind. A failure to secure the contract or unfavorable terms could lead to investor disappointment.

Mid- to Long-Term: The Path to Business Diversification

The most compelling aspect of this KOREAN AIR LINES investment thesis is the potential for strategic diversification. The commercial airline industry is notoriously cyclical and sensitive to economic shocks, fuel prices, and global events. Securing a significant role in the defense sector would provide a stable, long-term revenue stream insulated from these pressures.

Successful execution of this L3Harris partnership could establish KOREAN AIR LINES as a key player in South Korea’s defense-industrial ecosystem. This opens doors to future projects, from aircraft maintenance to advanced modifications and systems integration. For more context on the industry, see our guide to investing in aerospace and defense stocks.

Investment Strategy: Key Points to Watch

Given the current information, a ‘watchful waiting’ approach is the most prudent strategy. The potential upside is clear, but the risks of premature investment are tangible. Investors should focus on the following key points leading up to the November 20, 2025 re-disclosure date.

- •Contract Confirmation: The binary outcome of whether the contract is signed is the most critical factor.

- •Financial Details: Once confirmed, the contract’s total value for KOREAN AIR LINES, its duration, and expected profit margins will determine the actual financial impact.

- •Scope of Work: Understanding the company’s precise role—whether it involves complex systems integration or more basic airframe modification—will be key to assessing its long-term value creation. Defense contractors like L3Harris Technologies have extensive global supply chains, and KOREAN AIR’s role within it matters.

In conclusion, the potential entry into the airborne control aircraft project is a genuinely exciting development for KOREAN AIR LINES. It represents a tangible step toward becoming a more resilient and diversified aerospace leader. While short-term volatility in KOREAN AIR LINES stock is expected, the long-term strategic merit is undeniable. The upcoming disclosure will be the true determinant, and investors should remain vigilant for the confirmed details.