An in-depth analysis of DAEJIN ADVANCED MATERIALS Inc. stock (393970) has become critical following a major market event. A significant institutional investor, Kolon Investment, has divested a substantial portion of its holdings, sending ripples through the investment community. This move raises urgent questions: Is this a sign of underlying trouble, or simply a strategic portfolio adjustment? For current and potential investors, understanding the context behind this sale is paramount.

This comprehensive article breaks down the event, performs a deep dive into the company’s current financial health and business fundamentals, and provides a clear, actionable investment thesis to help you navigate the uncertainty surrounding DAEJIN ADVANCED MATERIALS Inc. stock.

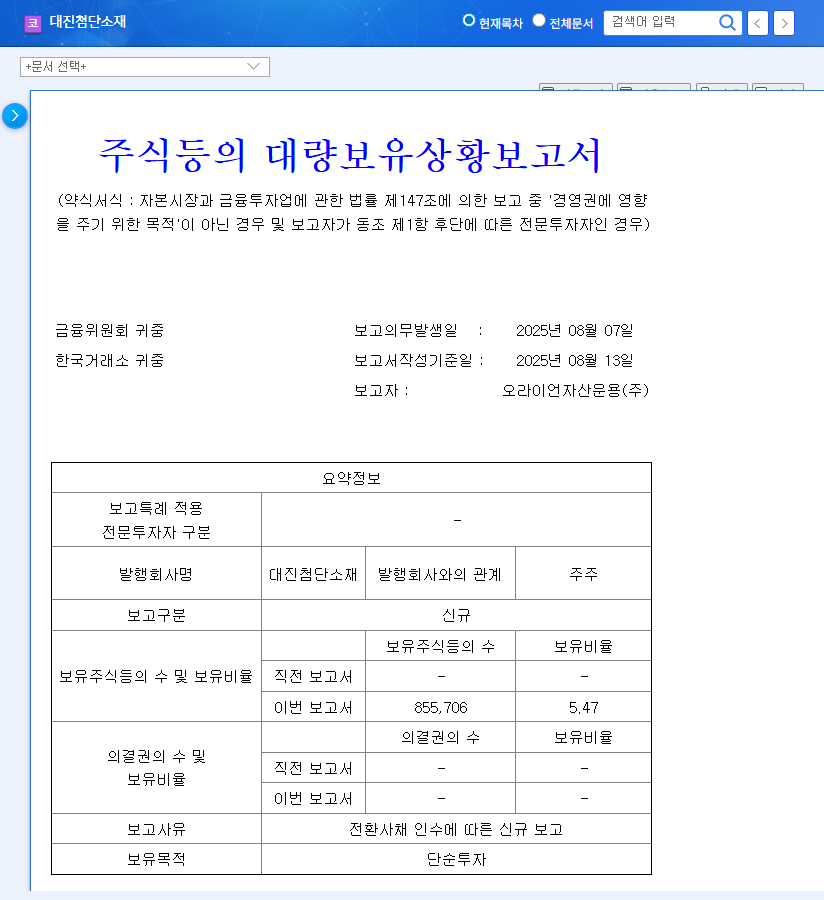

The Catalyst: Kolon Investment’s Major Block Sale

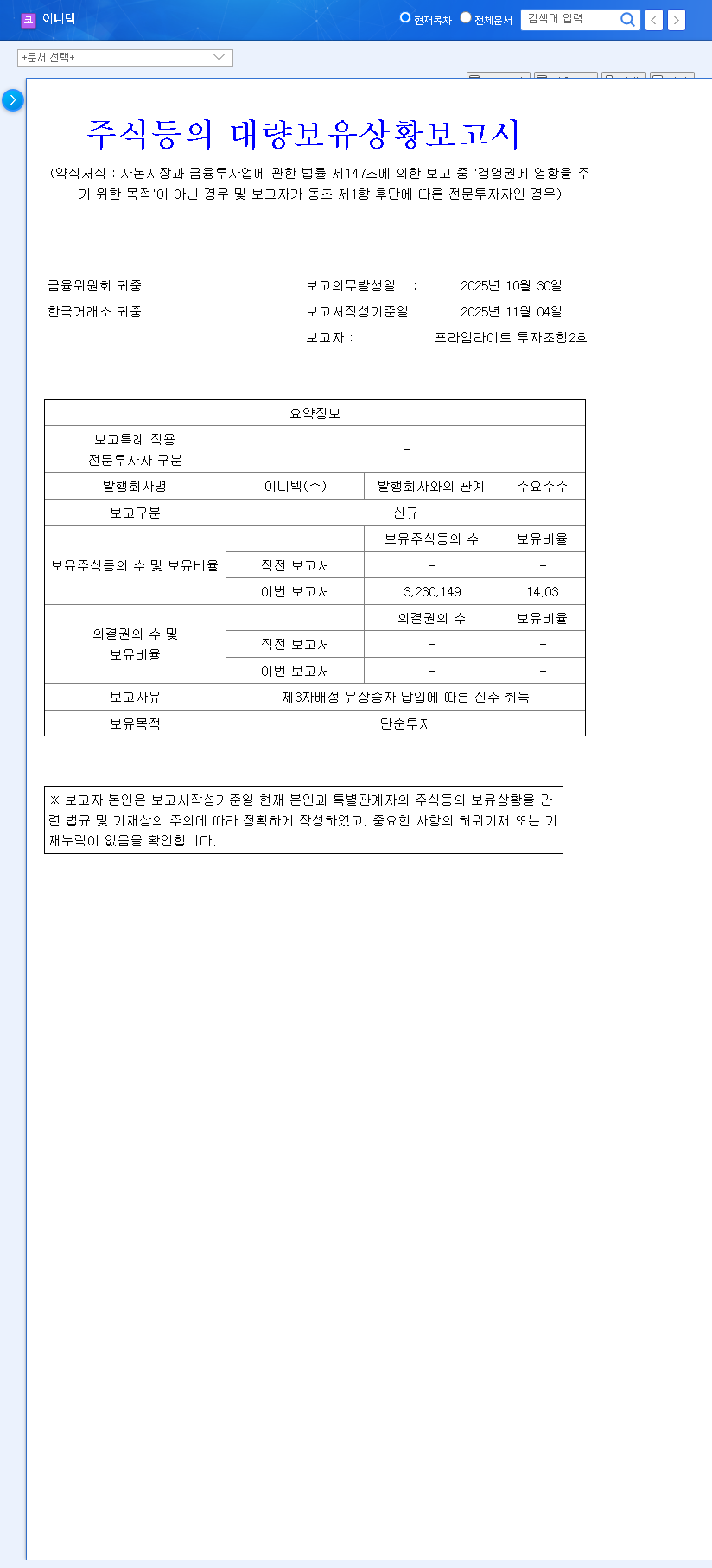

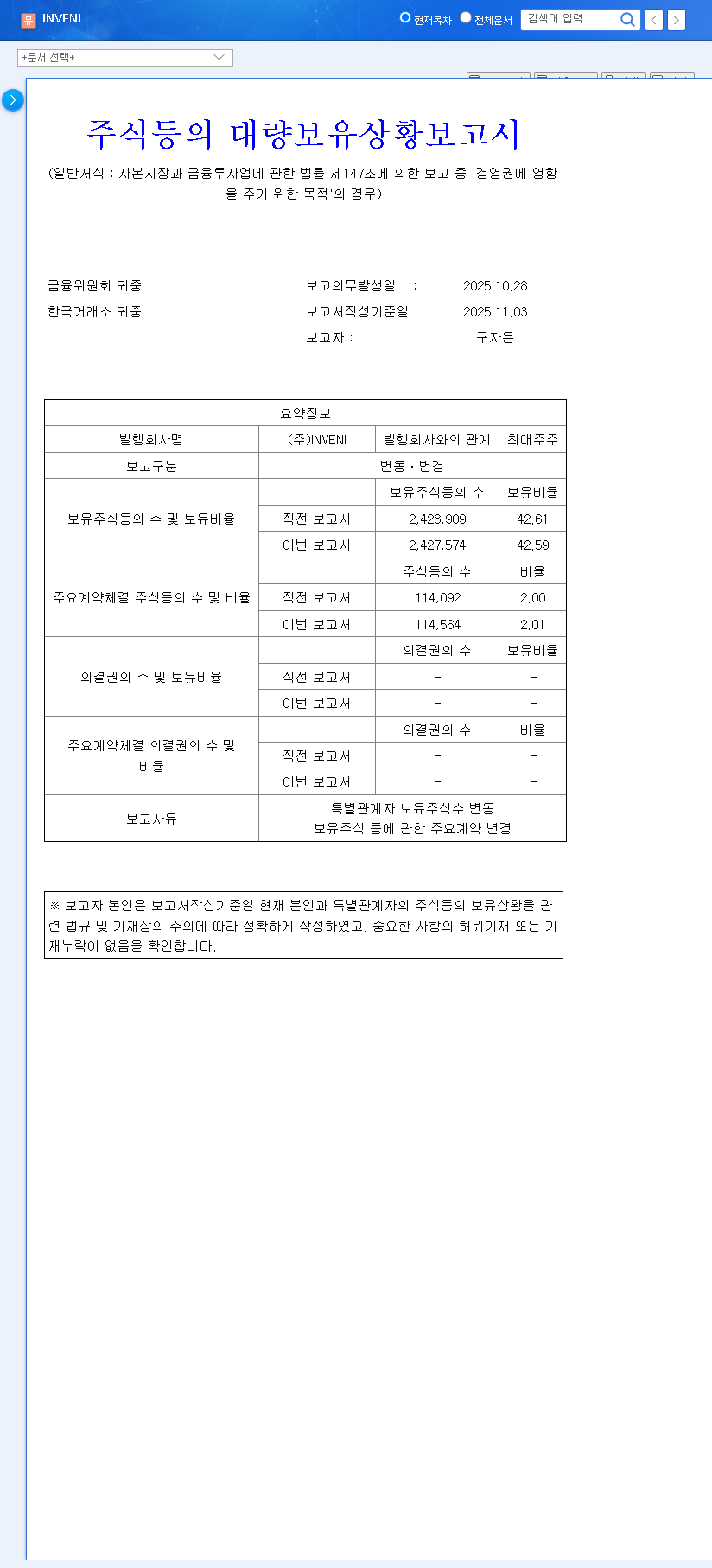

On November 13, 2025, a mandatory disclosure confirmed that Kolon Investment executed a large-scale sale of its shares in DAEJIN ADVANCED MATERIALS Inc. The official filing, known as a ‘Report on the Status of Large Shareholdings,’ detailed a significant reduction in their position. The official disclosure can be reviewed directly on DART (Source).

This wasn’t a minor trim. Kolon Investment offloaded 917,050 shares, slashing their stake from 13.96% down to just 4.53%—a decrease of approximately 9.43 percentage points.

While the stated reason for the sale was a ‘simple investment purpose’—often used to signify profit-taking or portfolio rebalancing—the sheer size of the sale by a major institutional holder is a material event that warrants close scrutiny.

Deep Dive: Analyzing DAEJIN ADVANCED MATERIALS Inc. (393970) Fundamentals

To understand the potential long-term trajectory of the DAEJIN ADVANCED MATERIALS Inc. stock, we must look beyond this single event and assess the health of the underlying business.

Core Business Under Pressure

The company’s primary revenue comes from materials used in secondary battery processes and automotive parts. Unfortunately, this segment has faced severe headwinds. In the first half of 2025, revenue from this division plummeted by a staggering 63.7% year-over-year. This is largely attributed to a market phenomenon known as the ‘chasm’ in the electric vehicle (EV) industry, where growth temporarily slows as the market transitions from early adopters to the more pragmatic mainstream consumer, compounded by a challenging macroeconomic environment.

The Future Bet: Carbon Nanotube (CNT) Technology

DAEJIN is pinning its future growth on its Carbon Nanotube (CNT) business. CNTs are advanced materials with exceptional strength and conductivity, making them highly valuable for next-generation batteries and other high-tech applications. While the company is actively pursuing technology acquisition and global expansion in this area, it’s crucial to note that tangible sales results from the CNT division are still minimal. It remains a promising but currently unproven growth engine.

Financial Red Flags: A Look at the Numbers

The 2025 semi-annual report paints a concerning financial picture:

- •Worsening Profitability: The company posted an operating loss of 3.4 billion KRW and a net loss of 10.5 billion KRW, a sharp reversal into deficit.

- •Rising Debt: Total debt increased by 27.5%, with a notable rise in short-term borrowings and convertible bonds, increasing financial risk.

- •Negative Cash Flow: Operating cash flow was a deeply negative -22.6 billion KRW, indicating the core business is burning through cash rather than generating it.

Investment Outlook and Strategic Plan

Given the block sale and the weak fundamentals, how should investors approach the 393970 stock analysis?

Short-Term Impact: Expect Volatility

The immediate consequence of Kolon’s sale will likely be significant downward pressure on the stock price. The large influx of shares can create an oversupply, and the negative signal sent by a major investor exiting can erode market confidence. Short-term traders should exercise extreme caution, as volatility is expected to be high.

Mid-to-Long-Term Outlook: All Eyes on Recovery

Over the long run, this single sale will become a footnote. The future of DAEJIN ADVANCED MATERIALS Inc. stock will be determined by its ability to execute a turnaround. Key catalysts to watch for are:

- •A recovery in the secondary battery and automotive markets.

- •Meaningful revenue generation from the CNT business.

- •Tangible steps to improve the company’s financial structure and reduce debt.

For context on market cycles, it’s helpful for investors to understand the risks and rewards of evaluating technology growth stocks during downturns.

Conclusion: A ‘Conservative’ Investment Opinion

Taking all factors into account—the major block sale by Kolon Investment, the severe downturn in core business revenue, and the precarious financial situation—our overall investment opinion on DAEJIN ADVANCED MATERIALS Inc. stock is ‘Conservative.’ The combination of external selling pressure and internal fundamental weakness creates a high-risk environment. Investors should wait for clear, sustained signs of a fundamental business recovery before considering a significant position. Monitoring macroeconomic factors is also crucial; for a broader view, resources like Reuters’ global market analysis can provide valuable context.