The latest KTnasmedia Q3 2025 earnings report (KRX: 089600) presents a complex picture for investors. While the company celebrated a significant revenue beat that surpassed market expectations, a surprising shortfall in operating profit and net income has cast a shadow on the results. This classic top-line strength versus bottom-line weakness scenario demands a closer look. In this in-depth analysis, we will dissect the numbers, explore the underlying factors driving this performance, and outline a strategic approach for investors considering their position in KTnasmedia stock.

Dissecting the KTnasmedia Q3 2025 Earnings Report

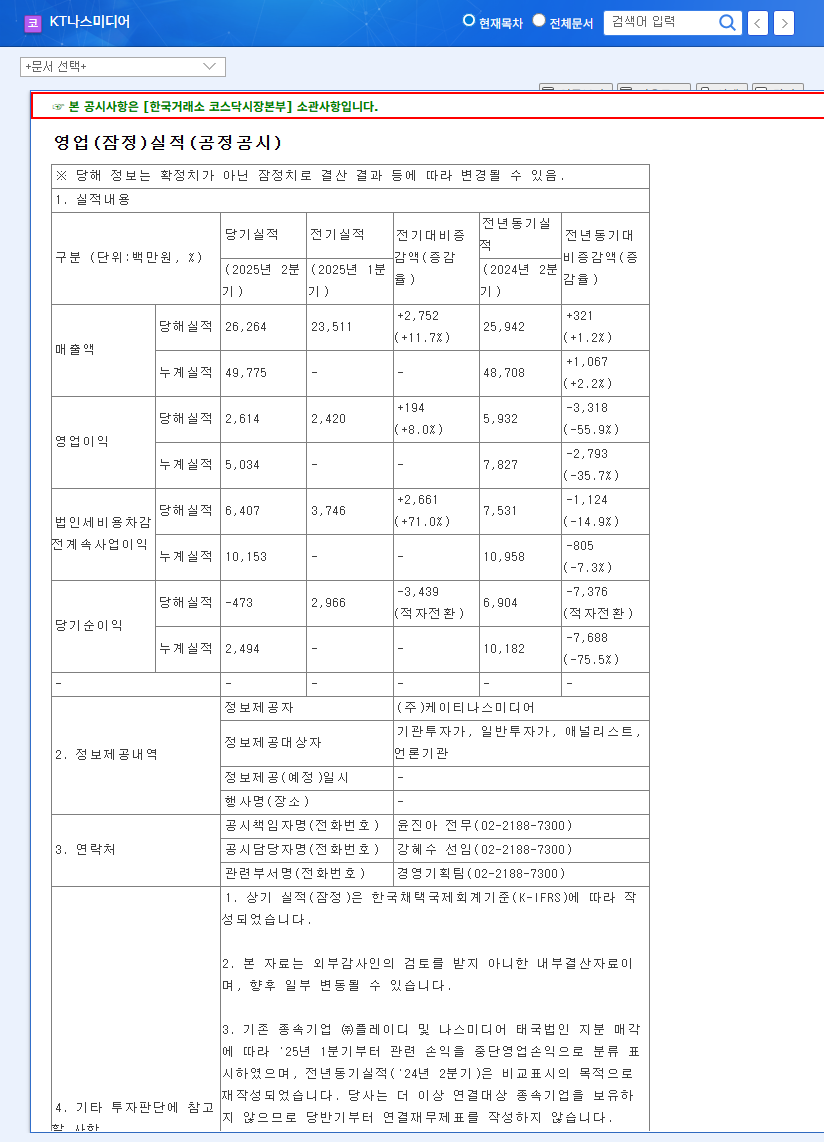

KTnasmedia Co., Ltd. released its preliminary financial results for the third quarter of 2025, revealing a significant divergence between sales and profitability. The official figures, as per the company’s disclosure, are as follows:

- •Revenue: KRW 31.2 billion, a 13% beat compared to the market consensus of KRW 27.5 billion.

- •Operating Profit: KRW 3.8 billion, a 19% miss against the market expectation of KRW 4.7 billion.

- •Net Income: KRW 4.9 billion, falling 11% short of the forecasted KRW 5.5 billion.

This data highlights robust growth in business operations and market demand. However, the inability to translate this top-line success into expected profits raises critical questions about cost management and investment cycles. The full details can be reviewed in the Official Disclosure (Source) on DART.

Fundamental Analysis: Strengths and Headwinds

To form a comprehensive KTnasmedia stock analysis, we must weigh the company’s strategic initiatives against the potential market and internal risks.

Positive Catalysts for Growth

- •Strategic Refocus & Financial Health: The recent divestiture of subsidiaries has streamlined operations, allowing KTnasmedia to concentrate on its high-margin core advertising business. This move also bolstered its balance sheet, reducing the debt-to-equity ratio to a healthier 102.93% and improving cash liquidity.

- •Investment in AI-Powered Ad Tech: The company is making significant R&D investments in next-generation advertising solutions, including AI-driven contextual advertising and its proprietary N.DMP (Data Management Platform). These technologies are crucial for maintaining a competitive edge in the evolving digital advertising market.

- •Favorable Market Tailwinds: The broader digital advertising sector continues to show resilient growth. According to industry reports from high-authority sites like major market analysts, the shift from traditional to digital media is ongoing, providing a supportive external environment for KTnasmedia’s services.

Potential Risk Factors to Monitor

- •Profitability Compression: The sharp drop in the operating profit margin from 18.03% (Q3 2024) to 12.18% (Q3 2025) is the most immediate concern. This may be a result of increased R&D spending or rising operational costs.

- •Macroeconomic Volatility: The company’s financials are exposed to currency fluctuations. A 10% change in the USD/KRW exchange rate can materially impact pre-tax income. A broader economic slowdown could also lead to reduced ad budgets from clients.

- •Post-Divestiture Revenue Dip: While strategic, the sale of subsidiaries will cause a temporary year-over-year revenue decrease in consolidated financials. The market will be watching to see if organic growth can quickly compensate for this.

The key question from the 089600 earnings report is whether the profit slump is a strategic investment in future growth or a sign of underlying operational weakness.

Strategic Outlook and Investment Thesis

Given the mixed signals from the KTnasmedia Q3 2025 earnings, investors should adopt a cautious but forward-looking approach. The short-term market reaction may be negative due to the profit miss, potentially creating a buying opportunity for those with a long-term KTnasmedia investment horizon.

Actionable Steps for Investors

- •Analyze the Next Earnings Call: Listen closely to management’s explanation for the profitability decline. Are the costs related to one-time investments or are they recurring? This will be the most critical piece of information.

- •Monitor AI Tech Monetization: Track announcements related to the new AI-powered advertising platforms. The key catalyst for a re-rating of the stock will be evidence that R&D is translating into new revenue streams and higher margins.

- •Review Valuation Metrics: Following a potential price dip, it’s essential to re-evaluate the company’s valuation. For more context, you can explore our guide on understanding key financial ratios.

In conclusion, KTnasmedia’s Q3 results are a pivotal moment. While short-term volatility is likely, the company’s strategic pivot towards its core ad-tech business, combined with investments in future-proof technologies, lays the groundwork for potential long-term value creation. Prudent investors should watch for signs of margin recovery in the coming quarters before making significant decisions.