Our latest analysis of the HD Hyundai Infracore Q3 2025 earnings report reveals a complex picture for investors. The company (KRX: 042670) delivered a surprising revenue beat but fell short on profitability, creating uncertainty in the market. This deep dive unpacks the numbers, explores the underlying fundamentals versus macroeconomic headwinds, and provides a clear investment thesis for both short-term traders and long-term shareholders.

Understanding this dichotomy is crucial for anyone considering an HD Hyundai Infracore investment. Is the profit miss a temporary blip caused by external factors, or does it signal deeper issues? Let’s dissect the results to find out.

Q3 2025 Earnings: A Detailed Breakdown

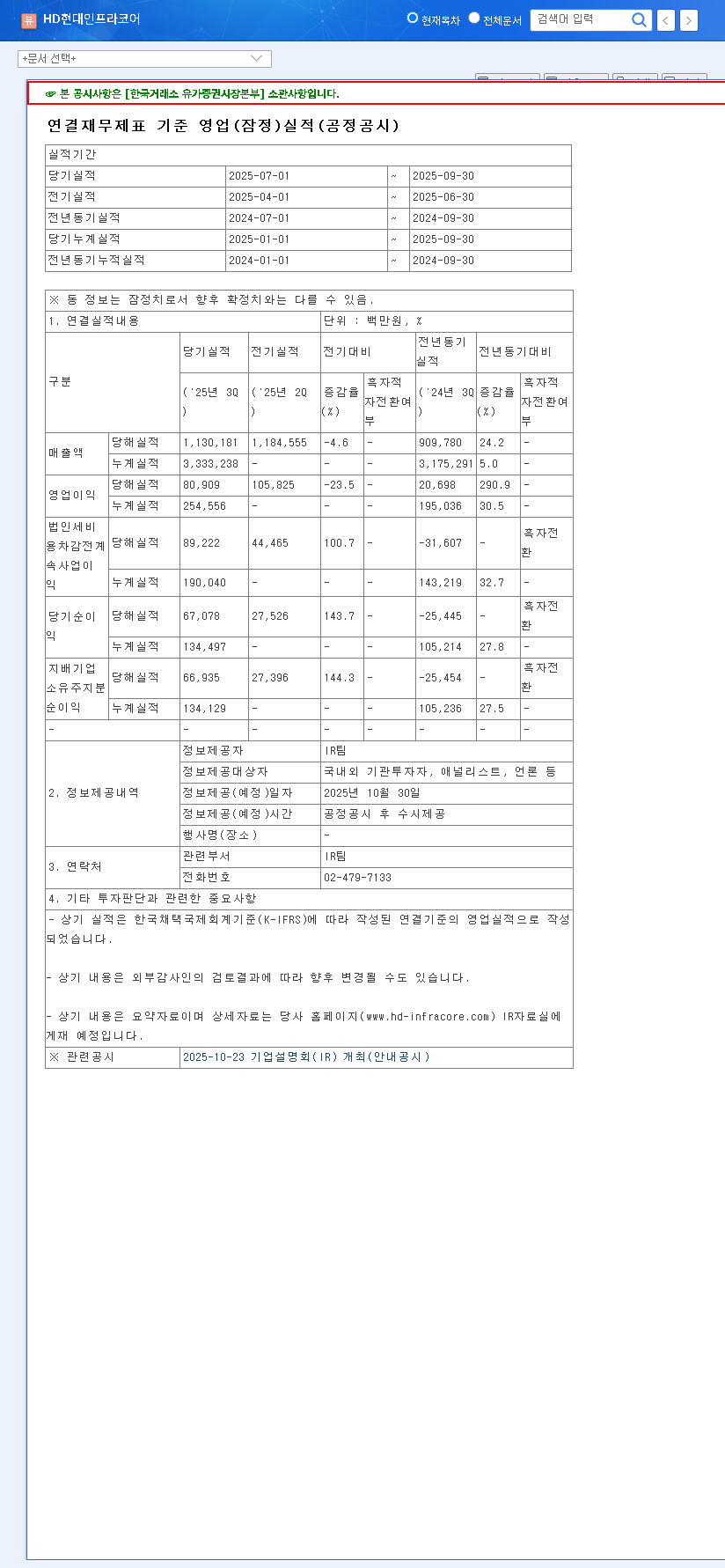

On October 30, 2025, HD Hyundai Infracore released its provisional third-quarter results, which presented a classic case of mixed signals. The official disclosure can be found on the DART (Financial Supervisory Service) portal. Here are the key figures compared to market consensus:

- •Revenue: KRW 1,130.2 billion, which was 1% above the market estimate of KRW 1,120.1 billion.

- •Operating Profit: KRW 80.9 billion, a significant 9% below the market estimate of KRW 88.9 billion.

- •Net Profit: KRW 66.9 billion, coming in 5% below the market estimate of KRW 70.3 billion.

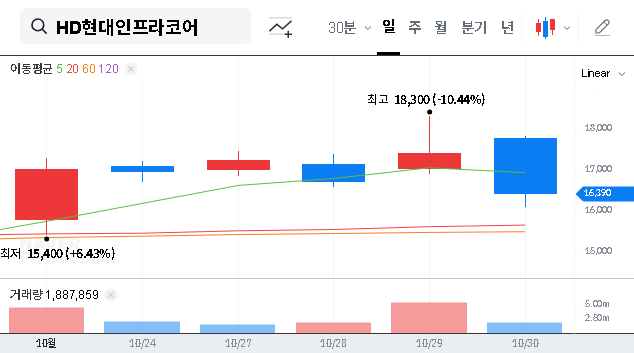

The top-line revenue growth continues a positive trend, suggesting resilient demand for the company’s products. However, the sharp sequential decline in operating profit from Q2’s KRW 105.8 billion is a major point of concern and is likely to weigh heavily on near-term HD Hyundai Infracore stock performance.

Analyzing the Dichotomy: Strong Fundamentals vs. Macro Headwinds

To understand the future trajectory, we must weigh the company’s internal strengths against the challenging external economic environment.

The Bull Case: Enduring Corporate Strengths

Despite the quarterly profit dip, the company’s fundamentals remain robust, signaling long-term potential:

- •Profitability Initiatives: Even with margin pressure, an improved operating profit margin of 7.87% in H1 2025 shows that cost-control measures and a focus on high-margin products are taking effect.

- •Solid Order Backlog: The defense division provides a stable revenue floor, with major contracts for Poland’s K2 tanks and engines for Turkey’s next-gen tanks ensuring future income streams.

- •Financial Fortitude: An improving debt-to-equity ratio and a healthy interest coverage ratio demonstrate a resilient balance sheet capable of weathering economic storms.

- •Future-Focused R&D: Significant investment in automation and unmanned technologies is positioning the company to be a leader in the next generation of industrial equipment. For more on this trend, see our analysis of automation in heavy industry.

- •DEVELON Brand Power: The new ‘DEVELON’ brand is gaining traction, which is expected to boost global market share and brand recognition over the long term.

The Bear Case: Navigating a Turbulent Global Economy

The profitability miss was likely driven by powerful macroeconomic forces that are impacting the entire industrial sector. As documented by sources like Bloomberg’s economic outlook, these challenges are significant:

- •Interest Rate Pressure: A rising global interest rate environment increases borrowing costs for both the company and its customers, potentially delaying large capital expenditures and construction projects.

- •Currency Volatility: While a strong USD/KRW can boost the value of exports, it also inflates the cost of imported raw materials and components, squeezing profit margins.

- •Input Cost Inflation: Fluctuations in the prices of steel, oil, and other key commodities directly impact production costs, making it difficult to maintain stable profitability without passing costs to consumers.

Investment Thesis & Outlook: A Holding Pattern

The core investment thesis for HD Hyundai Infracore is a balance of patience. The market is likely to react negatively to the short-term profitability miss, but the company’s strong fundamentals and long-term growth drivers—from defense contracts to the new DEVELON brand—remain firmly intact.

Our overall investment opinion is a Hold. We anticipate potential short-term volatility and price corrections as the market digests the weaker-than-expected profits. This period calls for careful monitoring rather than immediate action. The long-term outlook, however, remains positive. If the company can demonstrate a recovery in profit margins in the coming quarters, the current price levels could represent an attractive entry point for patient investors.

Actionable Plan for Investors

- •For Short-Term Investors: Exercise caution. Wait for the market’s initial reaction to settle. A break below key technical support levels could signal further downside. Monitor the Q4 earnings call for explicit commentary on margin recovery.

- •For Long-Term Investors: View any significant dips as potential opportunities for staggered accumulation. Focus on the execution of the defense backlog, DEVELON’s market penetration in North America and Europe, and progress in R&D initiatives.

- •Key Metrics to Watch: Keep a close eye on operating profit margins, raw material price trends, and global construction PMI data. The company’s ability to manage costs in this inflationary environment will be the ultimate determinant of future stock performance.

Disclaimer: This article provides an analysis based on publicly available information. Investment decisions carry risk, and the final responsibility rests solely with the investor.