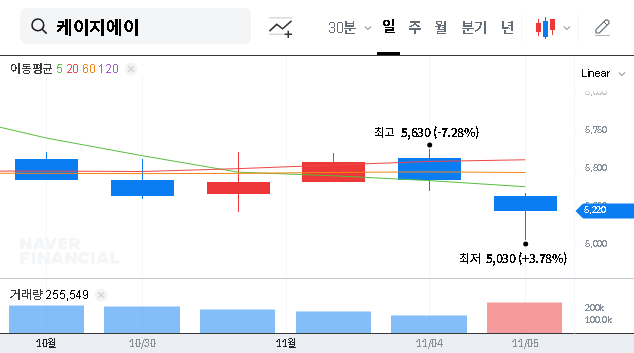

The recent news surrounding the KGA delisting review has sent shockwaves through the investment community, leaving shareholders concerned and potential investors wary. On November 14, 2025, KGA CO., LTD announced that its Q3 revenue had fallen below the critical threshold of KRW 300 million, automatically triggering a substantive eligibility review for delisting from the KOSDAQ market. This guide provides a comprehensive analysis of the situation, breaking down the financial crisis, market implications, and strategic actions for investors facing this high-stakes scenario.

Anatomy of a Crisis: The KGA Delisting Trigger

The catalyst for this crisis was a formal disclosure in KGA’s Q3 2025 quarterly report. The company confirmed its revenue fell short of the minimum requirement, placing it under the ‘cessation of major business operations’ clause as defined by KOSDAQ Market Listing Regulations (Article 56, Paragraph 1, Subparagraph 6). This is not a minor infraction; it is a severe event that questions the company’s operational viability and very existence. The official confirmation can be found in the company’s Official Disclosure on the DART system.

Dissecting the Financial Collapse: A Look at the Numbers

This delisting review was not a sudden event but the culmination of continuously deteriorating financial fundamentals. A closer look reveals a company in significant distress.

Key Financial Red Flags (Q3 2025 Cumulative)

- •Massive Revenue Decline: Cumulative revenue plunged to KRW 16.83 billion, a staggering 56% decrease year-over-year. The Q3-specific revenue of less than KRW 300 million signifies a near-total halt in core operations.

- •Deepening Losses: The company swung to an operating deficit of KRW 700 million and posted a substantial net loss of KRW 7.07 billion, exacerbated by IPO-related merger costs.

- •Precarious Financial Health: Despite an IPO-driven capital increase, accumulated losses have wiped out retained earnings. A high debt-to-equity ratio of 134% and significant cash outflow from investments raise serious doubts about its ability to fund ongoing operations.

Core Business Under Siege

The company’s primary business segments face immense challenges. The slowdown in the global electric vehicle (EV) market has directly impacted its secondary battery electrode process equipment division, as major Korean battery manufacturers have slashed investments. While stable, its duct automation and engineering businesses are too small to offset this catastrophic decline, highlighting a critical failure in business diversification and risk management.

The trigger of a ‘cessation of major business operations’ review is one of the most severe flags for an investor, as it directly challenges the company’s ability to continue as a going concern.

The Ripple Effect: Widespread Consequences

The KOSDAQ delisting review process initiates a cascade of negative impacts that will be felt by the company and its investors for a long time.

- •Trading Suspension & Stock Collapse: An immediate trading halt is highly probable, trapping existing shareholders. If and when trading resumes, a catastrophic price drop is expected.

- •Erosion of Trust: Corporate image and trust among investors, partners, and financial institutions will be severely damaged, making any recovery effort incredibly difficult.

- •Funding Freeze: Raising new capital through debt or equity will become virtually impossible, strangling the company of the funds needed for operations and debt repayment. For more on this, you can read about how market confidence affects corporate financing.

- •Brain Drain: The uncertainty will likely lead to an exodus of skilled employees, further weakening the company’s ability to innovate and execute a turnaround plan. Understanding the basics of stock market delisting is crucial for investors, as explained by authoritative sources like Investopedia.

Investor Guide: A Strategic Action Plan for KGA Stock

Given the high probability of a negative outcome from the delisting review, a prudent and cautious approach is paramount.

For New Investors

Avoid New Positions. Until all uncertainties surrounding the KGA delisting risk are fully resolved, initiating a new investment is an extremely high-risk gamble. The potential for total loss of capital is significant.

For Existing Shareholders

Evaluate Your Risk Tolerance. Investors should seriously consider reducing their position or setting a firm stop-loss for when trading resumes. While a speculative rebound is always possible, the fundamental case points towards further downside. During the trading suspension, closely monitor all company communications, press releases, and regulatory filings regarding its improvement plan and the status of the review.

Conclusion: A Time for Extreme Prudence

KGA CO., LTD is at a critical juncture, facing a crisis that threatens its survival. The delisting review is a direct result of a severe operational and financial breakdown. At this moment, the KGA delisting risk is exceptionally high. Unless the company can present a rapid, transparent, and highly credible turnaround plan, the outlook remains bleak. Investors must prioritize capital preservation and make decisions based on the stark reality of the company’s current situation. All investment decisions are the sole responsibility of the investor.