In a world of escalating geopolitical tensions, the defense sector is under an intense spotlight. This comprehensive LIG Nex1 stock analysis delves into the prospects of South Korea’s leading defense contractor, LIG Nex1 Co., Ltd. (079550), as it approaches a pivotal Investor Relations (IR) event on November 18, 2025. Following a surprising revenue decline in the first half of the year, all eyes are on the upcoming Q3 earnings report and the company’s strategic vision for the future.

This article provides an expert breakdown of LIG Nex1’s current financial standing, its promising growth catalysts, and the critical factors investors must monitor during the IR event. We will dissect the numbers, evaluate the strategies, and offer a clear framework for making informed investment decisions.

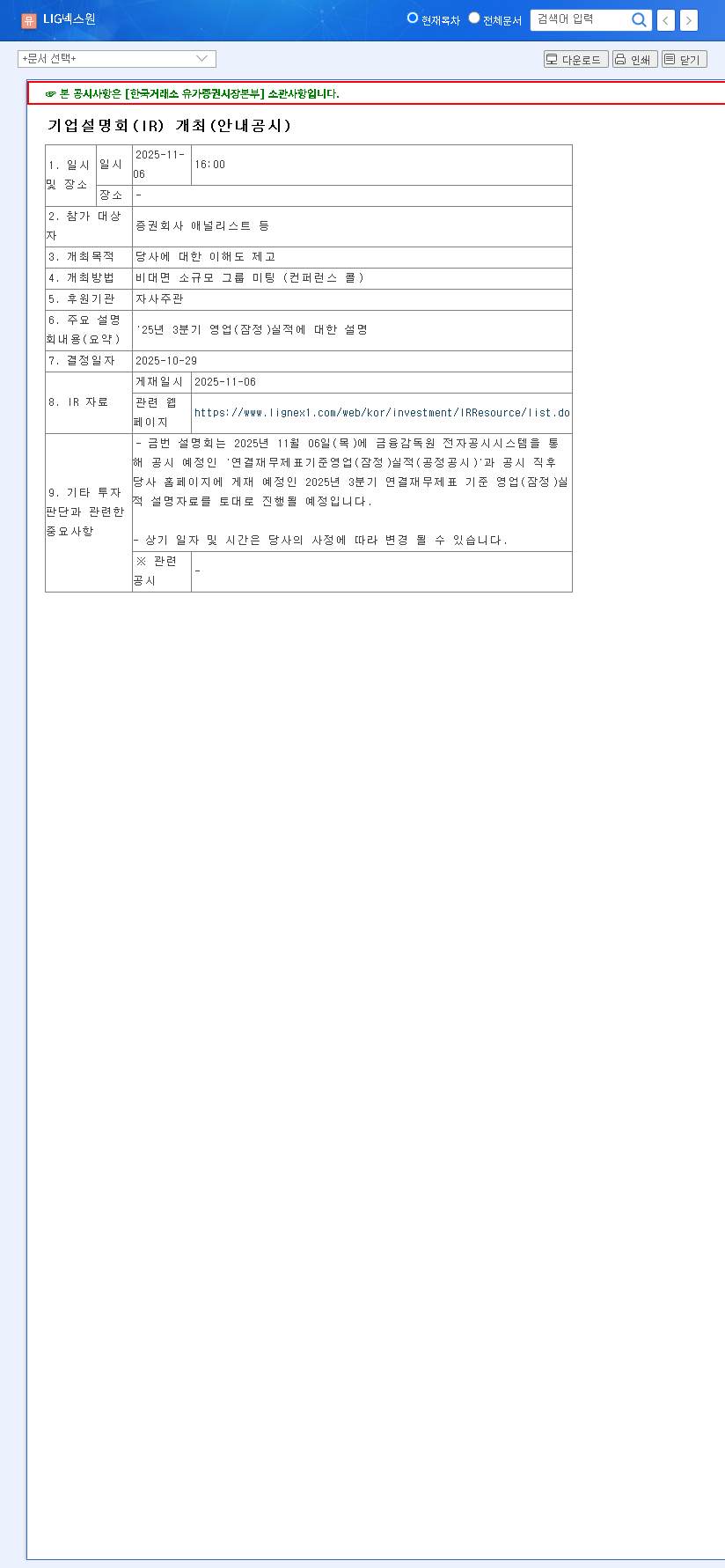

The Q3 2025 IR Event: A Moment of Truth

LIG Nex1’s scheduled IR event is more than a routine update; it’s a critical platform to address investor concerns and chart a course for future growth. The primary agenda includes the announcement of preliminary LIG Nex1 earnings for Q3 2025 and a detailed presentation on the company’s operational status. The market is eager for clarity on the H1 revenue dip and reassurance about the company’s long-term trajectory.

In-Depth LIG Nex1 Stock Analysis: Financial Health & Performance

The Paradox: Declining Revenue vs. a Massive Order Backlog

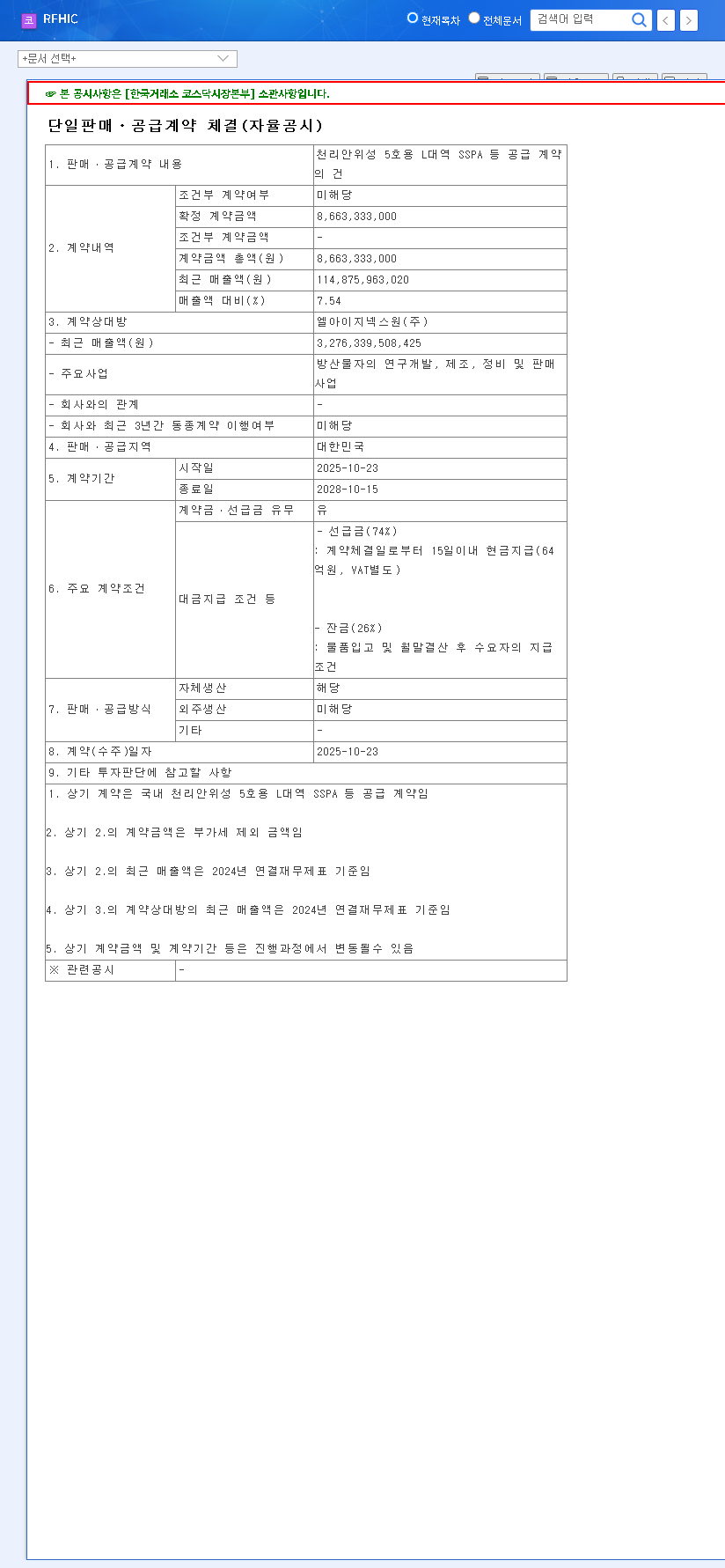

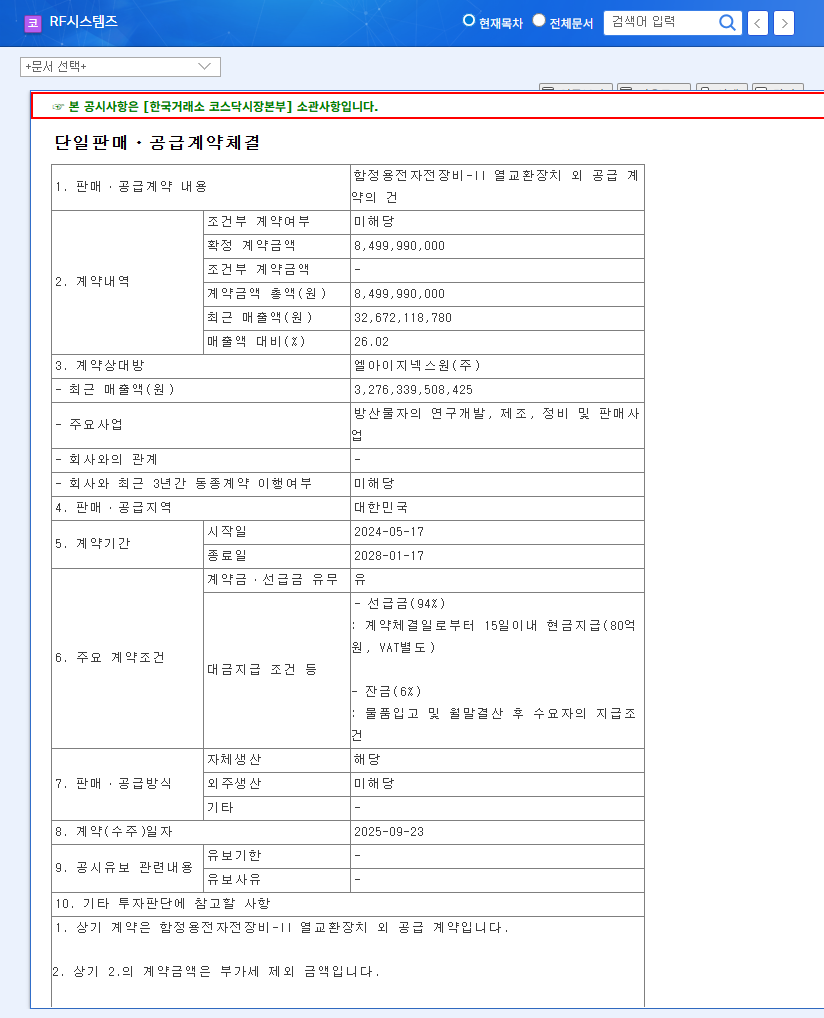

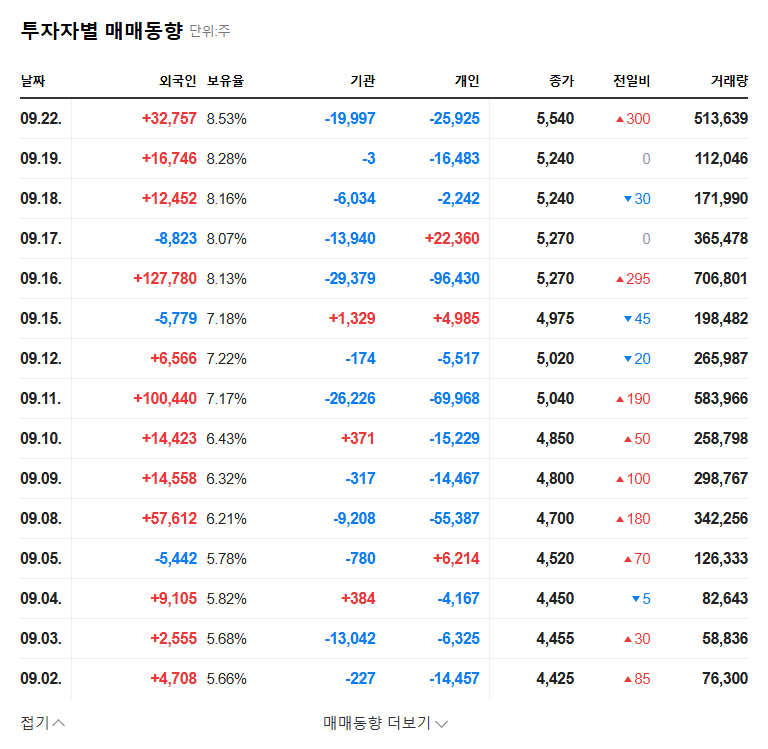

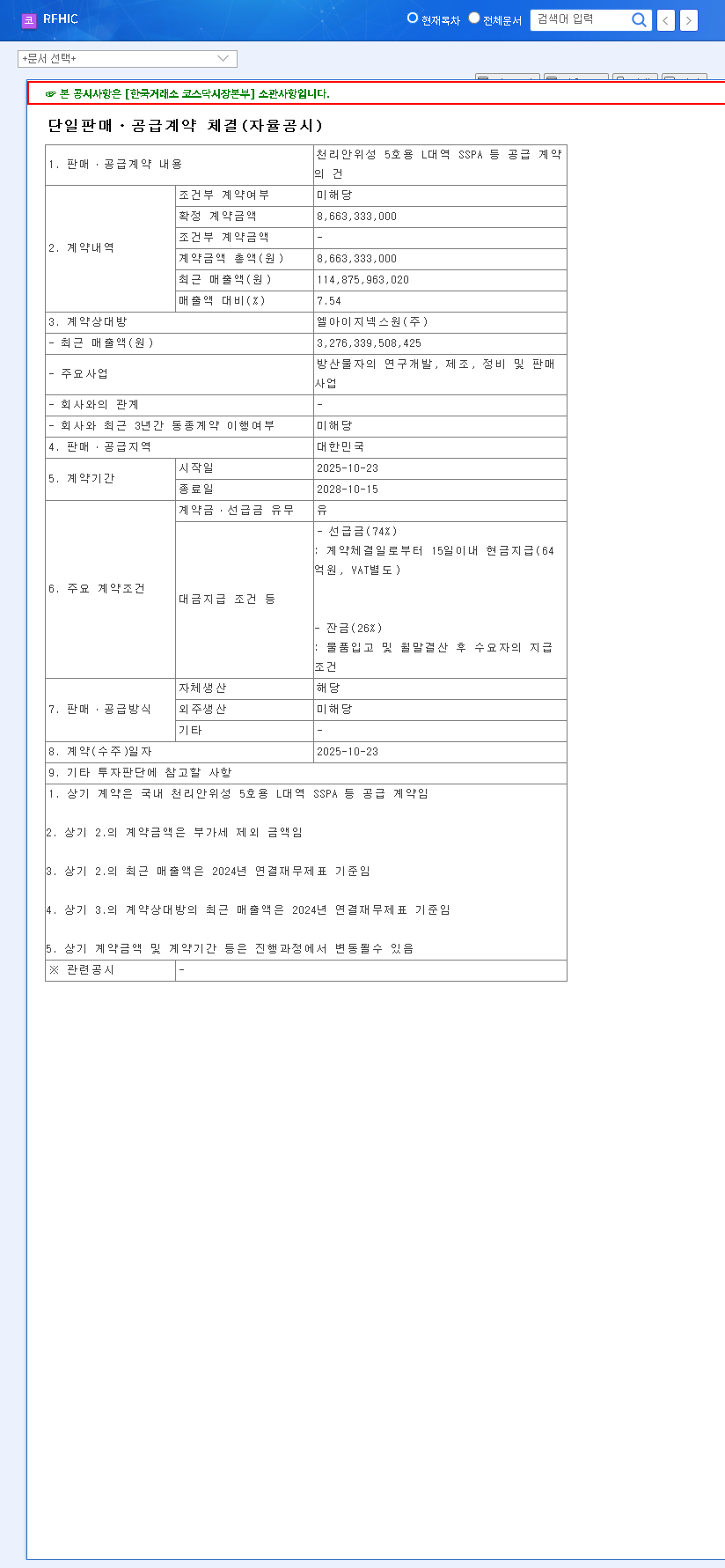

According to its H1 2025 report, LIG Nex1 posted revenue of KRW 1,852.97 billion, marking a 35.6% decrease year-on-year. This naturally raised concerns. However, the headline number doesn’t tell the whole story. The company boasts an incredibly robust order backlog of KRW 23,466.5 billion. This massive backlog provides a stable and predictable foundation for revenue streams for years to come, suggesting the H1 decline may be a matter of project timing rather than a fundamental business weakness. You can review the Official Disclosure (Source: DART) for more details.

An order backlog of over KRW 23 trillion acts as a powerful buffer against short-term revenue fluctuations, securing the company’s financial stability and offering significant long-term visibility for investors.

Core Business Segments and Export Outlook

The PGM (Precision Guided Munitions) segment remains the company’s revenue cornerstone, accounting for 47.8% of the total. The observed decline in other areas like ISR (Intelligence, Surveillance, Reconnaissance) and C4I (Command, Control, Communications, Computers, and Intelligence) is largely attributed to the cyclical nature of large-scale government contracts. The export share, which stood at 17.3%, also saw a temporary decrease. A key focus of the upcoming LIG Nex1 IR event will be the strategy to re-accelerate international sales and secure new overseas contracts.

Future Growth Engines: Robotics and Geopolitical Tailwinds

The Strategic Acquisition of Ghost Robotics

LIG Nex1’s forward-looking strategy is highlighted by its significant acquisition of Ghost Robotics Corporation. This move is not merely a diversification play; it’s a strategic pivot to secure a foothold in the future of defense technology. This acquisition establishes a powerful robotics platform, opens a direct channel into the lucrative U.S. defense market, and positions LIG Nex1 at the forefront of autonomous warfare systems. This investment signals a strong commitment to becoming a global, tech-driven defense powerhouse.

Macroeconomic and Geopolitical Opportunities

The global landscape presents significant opportunities for the Korean defense industry. Rising global defense budgets, driven by heightened security concerns, create a fertile ground for companies like LIG Nex1. According to reports from leading defense analysts, global military expenditure continues to climb. Additionally, the weaker Korean Won against the US Dollar provides a competitive pricing advantage for LIG Nex1’s exports, potentially boosting profitability on international contracts.

Investor Action Plan: What to Watch in the IR Briefing

For investors conducting a thorough LIG Nex1 stock analysis, the IR event will provide crucial data points. Pay close attention to the management’s commentary on the following key areas:

- •Q3 Performance: Is there a clear reversal or stabilization of the revenue decline? Listen for a detailed analysis of the causes and the outlook for Q4 and beyond.

- •Robotics Synergy: Demand concrete plans on how Ghost Robotics will be integrated and the timeline for realizing synergies and penetrating the U.S. market.

- •Export Strategy: What is the specific plan to regain momentum in overseas markets? Look for announcements of new contracts or progress in key international negotiations.

- •Financial Management: How is the company managing its balance sheet and cash flow amidst large R&D investments and acquisitions?

For more insights, you can compare this with our Deep Dive into the Korean Defense Sector.

Frequently Asked Questions (FAQ)

Q1: When is the LIG Nex1 IR event?

A1: The Investor Relations (IR) event is scheduled for November 18, 2025. It will feature the announcement of preliminary Q3 2025 operating results and a detailed corporate briefing.

Q2: What is the significance of LIG Nex1’s order backlog?

A2: Despite an H1 2025 revenue dip, the company holds a massive order backlog of over KRW 23 trillion. This provides a very stable and predictable foundation for future revenues, mitigating short-term performance concerns.

Q3: What are LIG Nex1’s key future growth drivers?

A3: Key growth drivers include strengthening its core domestic business and expanding into future technologies through strategic moves like the acquisition of Ghost Robotics, which is aimed at securing a leading position in defense robotics and entering the U.S. market.

Q4: What are the primary risks for the 079550 stock?

A4: Key risks include potential delays in converting the order backlog to revenue, increased competition in the global defense market, the efficiency of R&D spending, and the impact of currency fluctuations on profitability.