The recent Korean Air Lines L3Harris contract marks a pivotal moment for the airline’s burgeoning aerospace division. In a landmark deal, Korean Air secured a long-term supply agreement worth ₩631.9 billion (approximately $460 million USD) with L3Harris Technologies, a global aerospace and defense titan. This agreement, centered on crucial Korean Airborne Early Warning & Control (AEW&C) components, is far more than a simple revenue entry; it signals a strategic deepening of Korean Air’s role in the high-stakes global defense supply chain. This analysis will dissect the contract’s details, explore its profound impact on Korean Air’s fundamentals, and provide a clear-eyed outlook for investors.

Deconstructing the Landmark Agreement

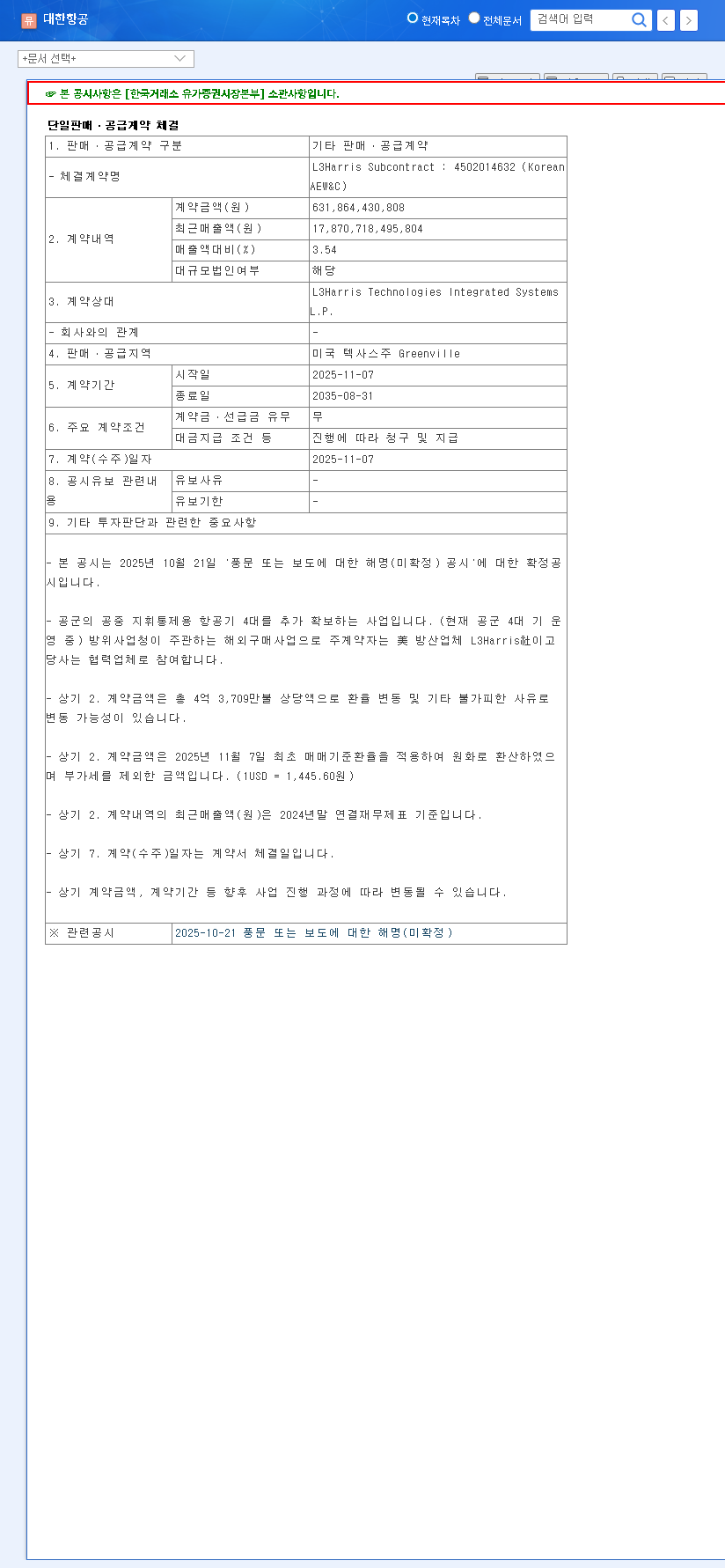

Announced on November 7, 2025, this significant supply contract formalizes a long-term partnership with L3Harris Technologies Integrated Systems L.P., a key player in the U.S. defense sector. The scale and duration of this deal underscore its strategic importance for the Korean Air aerospace division.

Key Contract Specifics

- •Total Value: ₩631.9 billion, representing 3.54% of Korean Air’s recent total revenue.

- •Contract Duration: A nearly decade-long term from November 7, 2025, to August 31, 2035.

- •Scope of Work: Supply of critical components for Korea’s advanced AEW&C aircraft, a vital national security asset.

- •Counterparty: L3Harris Technologies, a top-tier U.S. defense contractor known for its advanced technology solutions.

Strategic Impact on Korean Air’s Aerospace Ambitions

This long-term agreement is a powerful catalyst, expected to deliver several fundamental benefits that extend well beyond the balance sheet. It solidifies the aerospace division’s position as a core pillar of future growth for the company.

This contract is not just about revenue; it’s a vote of confidence in our technological prowess and a gateway to deeper integration within the global aerospace and defense market.

Securing Predictable, Long-Term Revenue

In an industry often marked by cyclicality, a ten-year contract provides an invaluable stream of predictable revenue. This stability enhances financial planning, de-risks future investments in the aerospace division, and provides a buffer against volatility in the passenger airline market.

Expanding Presence in the U.S. Defense Market

The deal, centered in Greenville, Texas, provides Korean Air with a crucial foothold in the highly competitive U.S. market. Successfully executing this AEW&C components supply contract will bolster the company’s reputation and strengthen its relationships with the U.S. government and other defense contractors, potentially unlocking future large-scale opportunities.

Market Outlook and Investor Considerations

While the long-term strategic benefits are clear, investors should analyze the Korean Air Lines L3Harris contract within a broader market context. Large-scale agreements like this typically boost investor sentiment, which can positively influence Korean Air stock performance. However, macroeconomic variables will play a significant role over the contract’s lifespan.

- •Exchange Rate Fluctuations: As a USD-denominated contract, swings in the KRW/USD exchange rate will directly affect the revenue and profitability when converted back to Korean Won.

- •Profitability Margins: While defense contracts are often stable, the specific profit margins are not public. Investors must monitor company reports for insights into the project’s overall profitability.

- •External Factors: The ongoing progress of the Asiana Airlines merger, geopolitical stability, and global economic trends will continue to influence Korean Air’s overall business environment.

Final Analysis & Investor Takeaway

The ₩631.9 billion agreement with L3Harris Technologies is an undeniable strategic win for Korean Air. It validates the capabilities of its aerospace division, ensures a decade of stable revenue, and opens doors for future growth. This development provides a strong tailwind for the company’s long-term fundamental health.

For investors, this news supports a positive, long-term outlook. However, a cautious ‘Neutral’ stance is advisable in the short term. Key variables, including undisclosed contract profitability and macroeconomic volatility, require continuous monitoring. Investment decisions should be made after considering these factors alongside the broader aviation industry landscape. For complete transparency, the original filing can be reviewed in the Official Disclosure.

Frequently Asked Questions

What is the core of the Korean Air Lines L3Harris contract?

It is a long-term supply contract valued at ₩631.9 billion, where Korean Air will provide key components for Korean AEW&C (Airborne Early Warning & Control) aircraft to U.S. defense company L3Harris Technologies over nearly 10 years.

How does this contract affect Korean Air’s revenue?

While representing 3.54% of total revenue, its primary benefit is not a massive short-term boost but rather the establishment of a stable, predictable revenue stream for the aerospace division over the next decade, which enhances financial stability.

What does this mean for the future of Korean Air’s aerospace business?

This deal significantly elevates the profile of Korean Air aerospace, confirming its technical expertise. It acts as a springboard for securing more high-value contracts and expanding its footprint in the lucrative U.S. defense market.