The latest Daewoong Pharma earnings report for Q3 2025 has presented a fascinating puzzle for investors and market analysts. While top-line revenue slightly missed expectations, the company delivered a significant ‘earnings surprise’ in its operating profit, signaling robust underlying profitability and operational efficiency. This in-depth analysis will dissect the provisional financial results, explore the core drivers behind this mixed performance, and provide a strategic outlook for investors evaluating Daewoong Pharma stock.

How did Daewoong Pharma orchestrate such a strong profit performance amidst revenue headwinds? We will explore the fundamental metrics, macroeconomic influences, and future catalysts that will shape the company’s trajectory.

Deconstructing the Q3 2025 Earnings Report

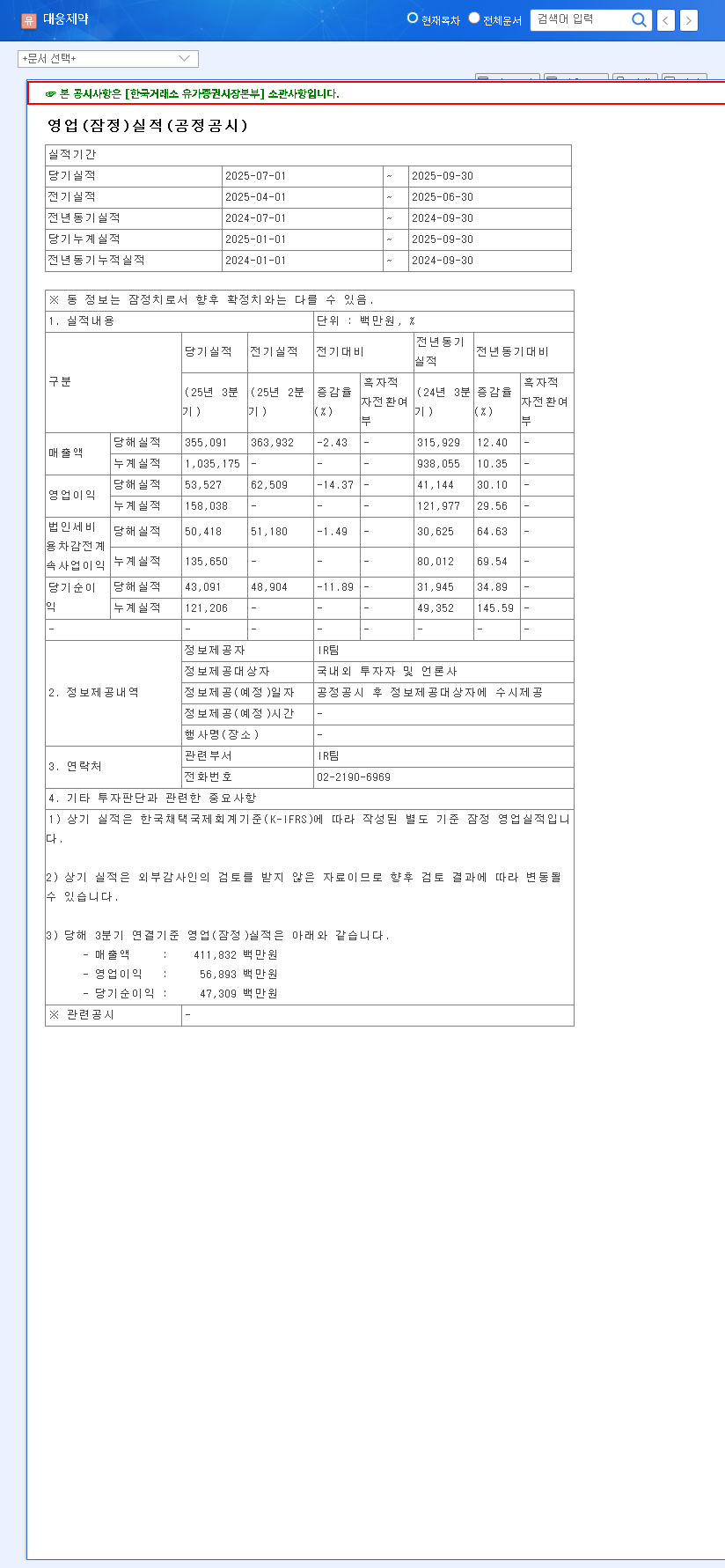

On November 7, 2025, Daewoong Pharma released its provisional Q3 earnings, with the market immediately focusing on two key conflicting data points. The provisional figures, released in the company’s Official Disclosure, paint a complex but ultimately promising picture. Here are the headline numbers:

- •Revenue: KRW 355.1 billion, which was 5% below the market consensus of KRW 372.2 billion.

- •Operating Profit: KRW 53.5 billion, a remarkable 11% above the market estimate of KRW 48.1 billion, creating the ‘earnings surprise’.

- •Net Profit: KRW 43.1 billion, showcasing a significant recovery and improvement from weaker performance in the prior year.

Despite a revenue shortfall, Daewoong Pharma’s ability to significantly boost operating profit by 43.4% year-over-year showcases remarkable operational efficiency and a strengthening core business.

Fundamental Analysis: The ‘Why’ Behind the Numbers

The Profit Powerhouse: Drivers of the Earnings Surprise

The surge in operating profit, up 43.4% year-over-year, is the central story of this earnings report. This impressive margin expansion, despite a 1.0% YoY revenue dip, points to several positive internal developments. The most likely drivers include a strategic shift towards a higher-margin product mix, successful implementation of stringent cost-control measures, and tangible gains in manufacturing and operational productivity. This demonstrates a sophisticated management approach focused on profitability over sheer volume, a key metric in any pharmaceutical stock analysis.

Revenue Growth and Financial Stability

While the revenue miss raises questions about near-term growth momentum, the company’s full-year 2025 projections remain positive, with revenue expected to reach KRW 8.048 trillion (+2.2% YoY). The more critical forecast is the projected 39.6% YoY increase in full-year operating profit. The company’s financial health appears solid; as of 2024, its debt-to-equity ratio was a manageable 84.85%, and a current ratio of 109.81% indicates sufficient liquidity to cover short-term liabilities, providing a stable foundation for future growth.

Navigating Macroeconomic Crosswinds

No company operates in a vacuum, and Daewoong Pharma is subject to several external economic forces. Persistent volatility in the USD/KRW and EUR/KRW exchange rates can directly impact the profitability of its international sales and the performance of overseas subsidiaries. Furthermore, rising international oil prices could exert upward pressure on production and logistics costs. On the other hand, declining global shipping indices may offer some relief. Investors must monitor how effectively the company hedges against these risks to protect its impressive margins.

A Strategic Action Plan for Investors

Given the nuances of the Q3 2025 Daewoong Pharma earnings, a prudent investment strategy requires a forward-looking and multifaceted approach. Before making any decisions, investors should consider the following action points:

- •Analyze the Final Report: Go beyond the provisional numbers. When the detailed report is released, scrutinize the segment-by-segment performance to identify precisely which products drove the margin improvements.

- •Monitor Key Pipelines: Future revenue growth hinges on the global market penetration of key drugs like ‘Fexuclue’ (GERD) and ‘Enavlo’ (diabetes). It’s also crucial to monitor R&D progress, a topic we cover in our deep dive into Daewoong Pharma’s R&D pipeline.

- •Assess Macro Resilience: Evaluate the company’s strategies for managing external risks, such as its currency hedging policies and supply chain diversification, to ensure profitability is protected from market volatility.

- •Re-evaluate Valuation: Observe how the market digests this earnings surprise. Analyze whether the improved profitability is being fairly priced into the Daewoong Pharma stock valuation. For a broader view, consult high-authority sources like Bloomberg’s pharmaceutical sector analysis.

In conclusion, Daewoong Pharma’s Q3 2025 results signal a company successfully optimizing its business structure for profitability. The key challenge ahead will be reigniting top-line revenue growth while defending these hard-won margins against a complex global backdrop. Meticulous analysis and ongoing vigilance are essential for any investor considering this promising but evolving opportunity.