The recent announcement of the DAEHO AL Co.,Ltd. stake sale in its subsidiary, Opticore, represents a pivotal strategic move for the company. While the transaction size of KRW 2 billion may seem modest, it signals a deliberate effort towards financial fortification and business realignment. This decision to divest is more than a simple line item on a balance sheet; it’s a calculated strategy aimed at securing vital operating funds and streamlining the corporate structure for future growth. For investors and market analysts, understanding the nuances of this divestment is key to forecasting the future trajectory of DAEHO AL (069460).

This comprehensive analysis will explore the details of the Opticore stake disposal, delve into the company’s current financial health, and evaluate the short-term and long-term implications of this strategic restructuring.

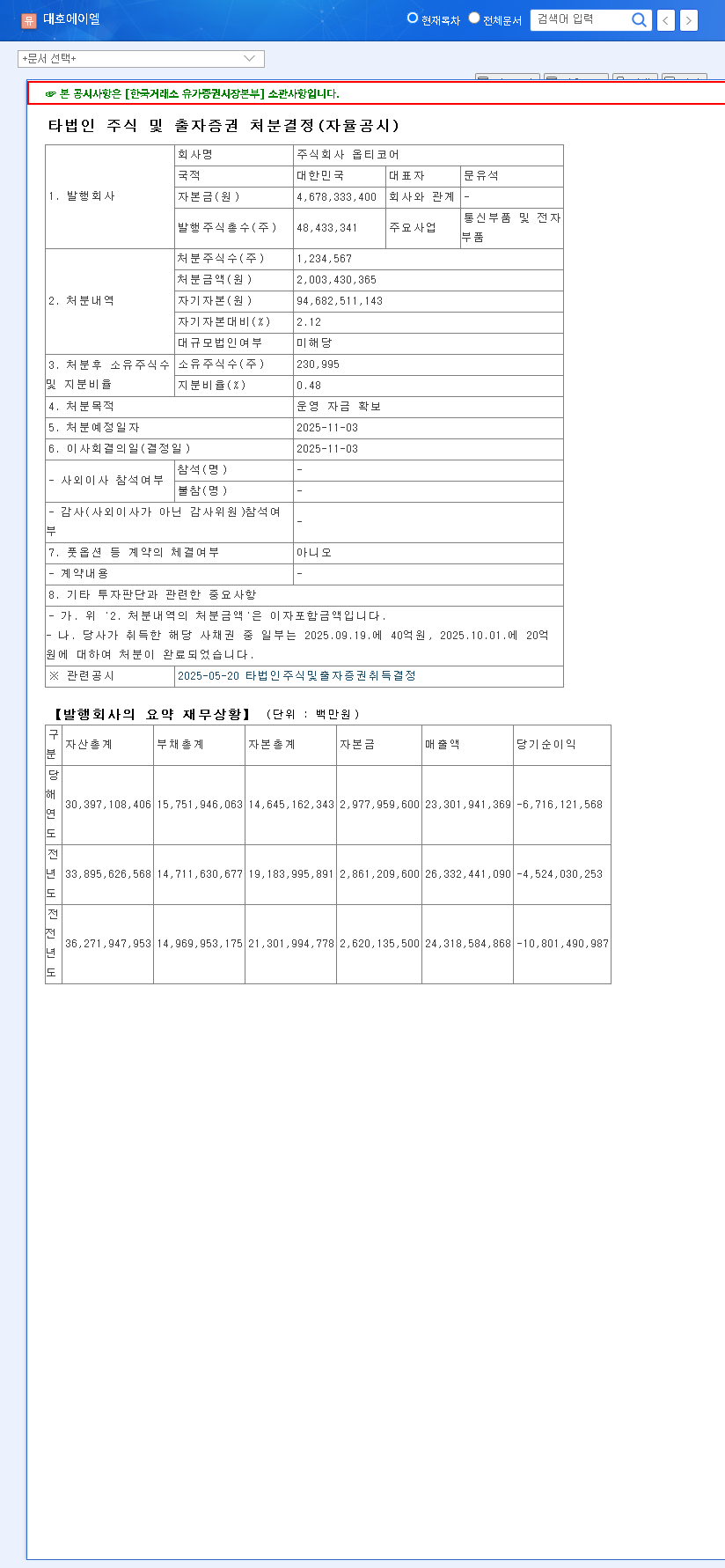

Transaction Overview: The Opticore Stake Disposal

On November 3, 2025, DAEHO AL Co.,Ltd. formally announced its decision to sell a portion of its shares and equity in Opticore. According to the Official Disclosure on DART, the transaction is valued at KRW 2 billion. This figure represents 2.12% of DAEHO AL’s total capital. Following the sale, DAEHO AL’s remaining stake in Opticore will be reduced to a minimal 0.48%, effectively marking a significant divestment from the subsidiary. The explicitly stated purpose is twofold: securing immediate operating funds and optimizing its business portfolio.

The Strategic Rationale Behind the DAEHO AL Co.,Ltd. Stake Sale

This decision is not merely a reactive measure for cash acquisition but a proactive step in a broader corporate strategy. Understanding the underlying motivations provides critical context for evaluating its potential success.

Immediate Need: Securing Operating Funds

The KRW 2 billion infusion provides DAEHO AL with immediate liquidity. This cash can be used to navigate short-term operational challenges, manage financial costs more efficiently, and weather periods of negative operating cash flow, which has been impacted by increases in inventory and accounts receivable. This financial buffer is crucial in a market facing rising interest rates and economic uncertainty.

Long-Term Vision: Business Restructuring

Beyond liquidity, the sale is a clear move towards DAEHO AL business restructuring. By divesting from what may be considered a non-core or underperforming asset, the management can redirect capital and focus towards more promising ventures. The company has already signaled its intent to pursue new growth drivers, including clean ventilation systems and the burgeoning battery business. This disposal frees up resources and management bandwidth to accelerate these new initiatives.

Strategic divestment allows a company to prune its portfolio, shedding assets that no longer align with its core mission to reallocate resources toward areas with higher growth potential.

A Snapshot of DAEHO AL’s Financial Health

A detailed financial analysis of DAEHO AL reveals a mixed but improving picture, providing context for the stake sale. While half-year 2025 revenue saw a 39% decrease year-over-year to KRW 102.2 billion, the company’s profitability has shown remarkable improvement. An operating profit of KRW 8.58 billion and a net profit of KRW 7.58 billion suggest successful cost management and financial optimization strategies, likely aided by recent fundraising activities. However, the company faces several key risks:

- •Cash Flow Concerns: Despite profitability, operating cash flow remains negative, putting pressure on liquidity.

- •New Business Uncertainty: The success of new ventures in clean ventilation and batteries is not yet guaranteed and requires significant investment.

- •Macroeconomic Headwinds: The company is exposed to external risks like interest rate hikes, raw material price fluctuations, and currency volatility. For more on this, investors can track global economic trends on platforms like Reuters.

Impact Analysis: What This Means for Investors

The stake sale’s impact can be viewed through both a short-term and long-term lens.

Short-Term Effects: Liquidity and Limited Stock Impact

The most immediate effect is a positive boost to financial liquidity. Furthermore, by reducing its stake in Opticore, DAEHO AL insulates its consolidated financial statements from the subsidiary’s performance volatility. However, the direct impact on the stock price is expected to be limited. The transaction size is not substantial relative to DAEHO AL’s overall market capitalization, and the market may view it as a necessary operational move rather than a transformative event.

Long-Term Outlook: A Foundation for Growth

The long-term implications are potentially more significant. This move is a textbook example of corporate restructuring, a topic you can learn more about in our guide to evaluating corporate strategy. If the proceeds are used wisely to pay down debt or invest in high-growth areas, it can strengthen the company’s financial health and enhance its competitive position. The market will be watching closely to see if this divestment marks the beginning of a successful turnaround and a pivot towards sustainable growth engines.

Investor Takeaways & Key Questions

Q: Why did DAEHO AL Co.,Ltd. sell its Opticore stake?

A: The primary stated reasons are to secure KRW 2 billion in operating funds to improve short-term liquidity and to advance its business restructuring strategy by divesting from non-core assets to focus on new growth drivers.

Q: How will this stake sale impact DAEHO AL’s stock price?

A: The short-term impact on the stock price is likely to be minimal due to the relatively small scale of the transaction. The long-term impact will depend on how effectively the company utilizes the funds and executes its pivot to new business areas. A positive market reaction will hinge on tangible results from these new ventures.

Q: What should investors monitor going forward?

A: Investors should maintain a neutral but watchful stance. Key areas to monitor include: the specific use of the KRW 2 billion proceeds, tangible progress and revenue generation from the clean ventilation and battery businesses, and the company’s ability to manage macroeconomic risks like interest rates and raw material costs.