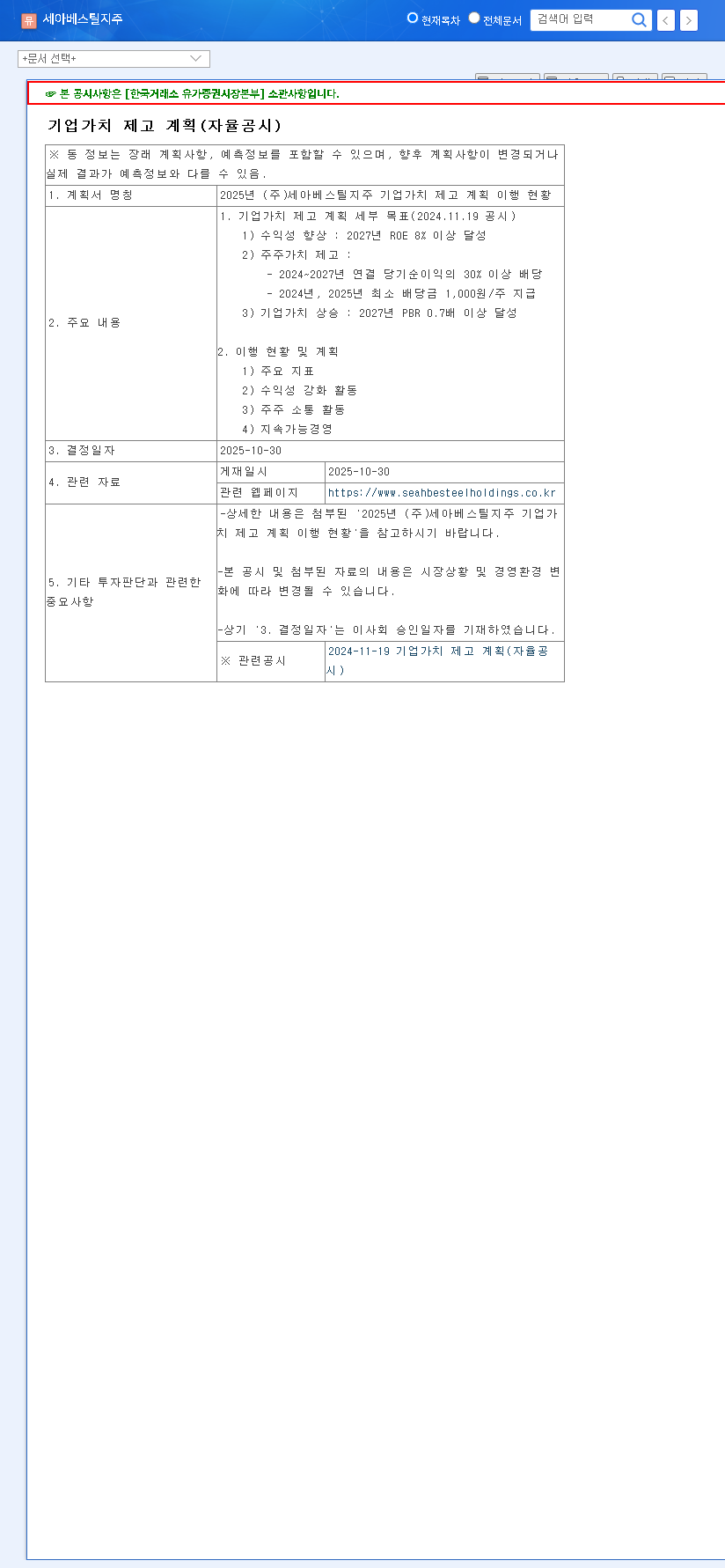

SeAH Besteel Holdings Corporation has captured the market’s attention with the recent progress report on its ambitious 2025 Corporate Value Enhancement Plan. This isn’t just a routine corporate update; it’s a strategic roadmap designed to bolster profitability, significantly increase shareholder returns, and elevate the company’s overall market valuation. For investors, this plan presents both a compelling opportunity and a series of critical questions.

This comprehensive investor analysis will dissect the core components of the plan, evaluate the fundamental strengths and weaknesses of SeAH Besteel Holdings, and provide a clear, strategic outlook. We will explore whether this roadmap is a guaranteed path to growth or if a more cautious approach is warranted in the current economic climate.

Core Pillars of the Value Enhancement Plan

The 2025 Corporate Value Enhancement Plan is built on three specific, measurable objectives that signal a profound commitment to sustainable growth and shareholder-friendly policies. Understanding these goals is the first step in a thorough investor analysis.

- •Enhanced Profitability: The primary financial target is to achieve a Return on Equity (ROE) of 8% or higher by the year 2027. This represents a significant leap from current levels, indicating a focus on operational efficiency and margin improvement.

- •Superior Shareholder Value: A commitment to distribute over 30% of consolidated net profit as dividends between 2024 and 2027. Crucially, the plan guarantees a minimum dividend of KRW 1,000 per share for 2024-2025, providing a reliable income floor for investors.

- •Corporate Value Growth: The goal is to reach a Price-to-Book Ratio (PBR) of 0.7x or more by 2027. This metric is key to addressing the ‘Korea discount’ and bringing the company’s market valuation more in line with its intrinsic asset value.

Fundamental Diagnosis of SeAH Besteel Holdings

As a pure holding company, the financial health of SeAH Besteel Holdings is intrinsically linked to the performance of its subsidiaries. A balanced view requires examining both its foundational strengths and the potential risks on the horizon.

Positive Fundamental Factors

- •Reliable Dividend Stream: With over 91% of its operating revenue coming from subsidiary dividends (notably from SeAH Besteel and SeAH Changwon Specialty Steel), the company has a stable income base.

- •Strong Creditworthiness: An A+ (Stable) corporate bond rating and A2+ commercial paper rating underscore its financial stability and access to capital markets, reducing financing risks.

- •Commitment to Innovation: Ongoing R&D investments by its subsidiaries in new materials and technologies are crucial for maintaining a competitive edge and long-term value creation.

Negative and Cautionary Factors

- •Subsidiary Performance Volatility: The specialty steel and aluminum industries are highly cyclical. A global economic slowdown or a downturn in key sectors like construction and automotive could directly impact profitability.

- •Rising Debt Levels: An increased consolidated debt-to-equity ratio heightens the company’s sensitivity to fluctuations in interest rates and foreign exchange, potentially pressuring margins.

- •Macroeconomic Headwinds: External risks, including volatile raw material prices, currency fluctuations, and rising protectionist trade policies, remain significant threats to business stability. For more on this, see analysis from leading financial experts at authoritative sources like Bloomberg.

By transparently outlining its mid-to-long-term growth objectives, SeAH Besteel Holdings is making a clear promise to investors. The key will be translating these ambitious targets into tangible financial results.

Impact Analysis and Investor Strategy

The announcement of the plan is a positive signal, but savvy investors must look beyond the headlines. The successful execution of this plan is contingent on both internal discipline and favorable market conditions. The company’s own projections, as detailed in its Official Disclosure (Source), show a path to improvement but highlight the significant effort required.

Achieving an ROE of 8% from its current low base will demand substantial operational improvements. While the enhanced dividend policy provides a strong incentive, its sustainability hinges on generating consistent net profit. For those unfamiliar with these metrics, our guide on understanding key financial ratios can provide more context.

Recommended Investment Approach

Given the current ‘initial phase’ of the plan, a ‘wait and see’ strategy followed by a cautious approach is prudent.

- •Short-Term (3-6 Months): The announcement may create some positive price momentum. However, this is likely to be speculative. Substantial appreciation in the SeAH Besteel stock price will require concrete proof of execution in upcoming quarterly reports.

- •Mid-to-Long-Term (1-3 Years): The key is to monitor the execution. Investors should closely track quarterly earnings, management commentary on profitability initiatives, and shareholder communication. The interim review scheduled for the end of 2025 will be a pivotal moment to reassess the plan’s viability and the company’s commitment.

In conclusion, while the Corporate Value Enhancement Plan from SeAH Besteel Holdings is a commendable and positive step, it is a statement of intent, not a guarantee of results. The path forward involves navigating significant industry and macroeconomic challenges. Diligent monitoring of the plan’s progress is essential before committing significant capital.