The latest DL E&C Q3 2025 earnings report has sent a strong signal to the market, showcasing a remarkable performance that significantly outpaced analyst expectations. In a construction sector fraught with uncertainty, DL E&C CO.,LTD. (ticker: 375500) delivered preliminary results that suggest robust operational health and strategic resilience. This in-depth analysis will dissect the key figures, explore the fundamental drivers behind this success, evaluate the macroeconomic environment, and provide a comprehensive investment outlook for the DL E&C stock.

DL E&C Q3 2025 Earnings: A Decisive Beat

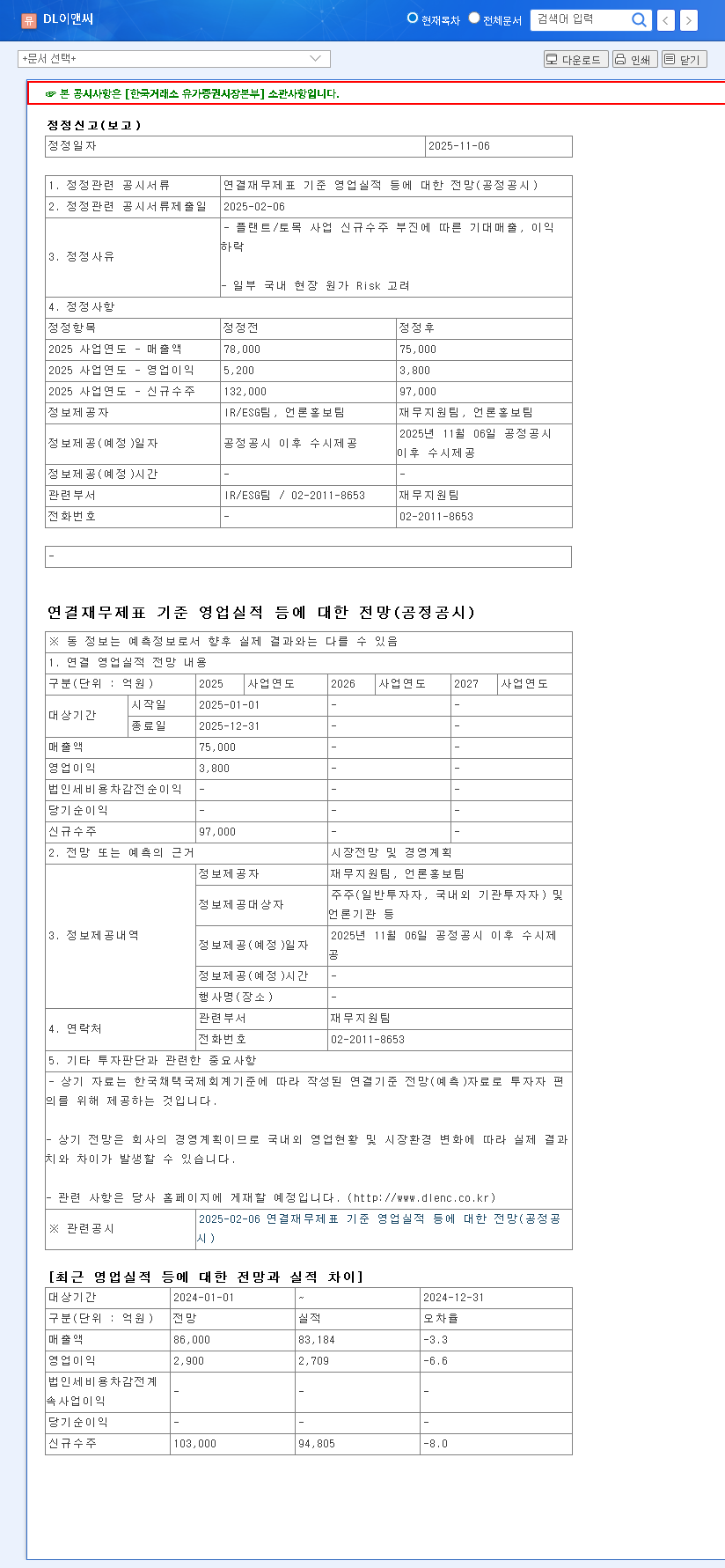

On November 6, 2025, DL E&C released its preliminary Q3 earnings, which immediately captured investor attention. The numbers were not just good; they were a significant ‘earnings surprise’. The official disclosure, available via the DART system, confirms these impressive figures. You can view the full report here: Official Disclosure.

Let’s break down the key performance indicators:

- •Revenue: KRW 1.907 trillion, which is a solid 4% above market consensus.

- •Operating Profit: KRW 116.8 billion, coming in 6% higher than anticipated.

- •Net Income: KRW 126.3 billion, an astonishing 29% surge above market expectations, highlighting exceptional profitability.

The 29% beat on net income is the standout figure, suggesting that DL E&C is not only growing its top line but is also managing its bottom line with remarkable efficiency. This points to strong financial health and bodes well for future shareholder value.

Core Drivers: Why Did DL E&C Outperform?

This success wasn’t accidental. It stems from a combination of strong internal management and navigating external factors adeptly. Our DL E&C investment analysis identifies two primary categories of drivers.

1. Robust Corporate Fundamentals

The company’s core operations are firing on all cylinders. While Q3 revenue saw a slight dip from the previous quarter, the improvement in operating profit indicates that one-off costs from Q2 have been resolved, revealing the company’s true competitive strength.

- •Substantial Order Backlog: Stable execution of a large and diverse project pipeline in both housing and industrial plants provided a consistent revenue stream.

- •Effective Cost Management: Proactive measures to control raw material and logistics costs have protected profit margins, a critical achievement in an inflationary environment.

- •Seasonal Strength: The company capitalized on the construction industry’s seasonal peak period, maximizing operational output and project progression.

2. Navigating the Macroeconomic Landscape

The broader construction industry outlook remains complex, influenced by global economic trends. For more on this, see this analysis of global construction trends from authoritative sources. However, signs are emerging that headwinds may be easing. The potential peak of the interest rate hike cycle, with US and Korean 10-year Treasury yields stabilizing, could reduce financing costs and stimulate new projects. While currency fluctuations and volatile commodity prices remain a risk, DL E&C’s balanced portfolio provides a crucial buffer against sector-wide shocks.

Investment Outlook: What’s Next for the DL E&C Stock?

The strong 375500 earnings report is expected to act as a powerful catalyst for its stock price. After a period of volatility driven by macroeconomic pressures, this performance provides tangible proof of the company’s value and resilience. It is likely to reverse negative sentiment and restore investor confidence.

However, prudent investors should remain vigilant. The construction industry is inherently cyclical. For a deeper understanding, you might want to read our Guide to Investing in the South Korean Construction Sector.

Key Observation Points Moving Forward:

- •Future Order Intake: Monitor the company’s ability to secure new high-margin projects to sustain its backlog.

- •Interest Rate & Real Estate Trends: Keep an eye on central bank policies and the health of the domestic and international real estate markets.

- •Government Policies: Changes in infrastructure spending or housing regulations could significantly impact the entire industry.

Conclusion: A Positive Outlook with Prudent Optimism

In summary, the DL E&C Q3 2025 earnings report is a highly positive development. It underscores the company’s robust operational capabilities and sound financial management. This performance should provide strong upward momentum for the stock and improve overall market sentiment. The investment recommendation is ‘Positive’, but investors should continue to monitor the key macroeconomic and industry-specific variables outlined above to make well-informed decisions.