The financial markets took notice when South Korea’s largest institutional investor, the National Pension Service (NPS), increased its holdings in Cosmecca Korea (241710). While officially termed a ‘simple investment,’ such a move by the NPS is widely interpreted as a significant vote of confidence in a company’s long-term value and growth trajectory. This action has sparked considerable interest in Cosmecca Korea stock and its future prospects.

This comprehensive Cosmecca Korea analysis will delve into the implications of the NPS investment. We will examine the company’s robust fundamentals, analyze the prevailing macroeconomic environment, and identify both the opportunities and potential risks for investors. Our goal is to provide a clear, data-driven outlook to help you formulate a well-informed investment strategy.

The NPS Investment: A Signal of Confidence

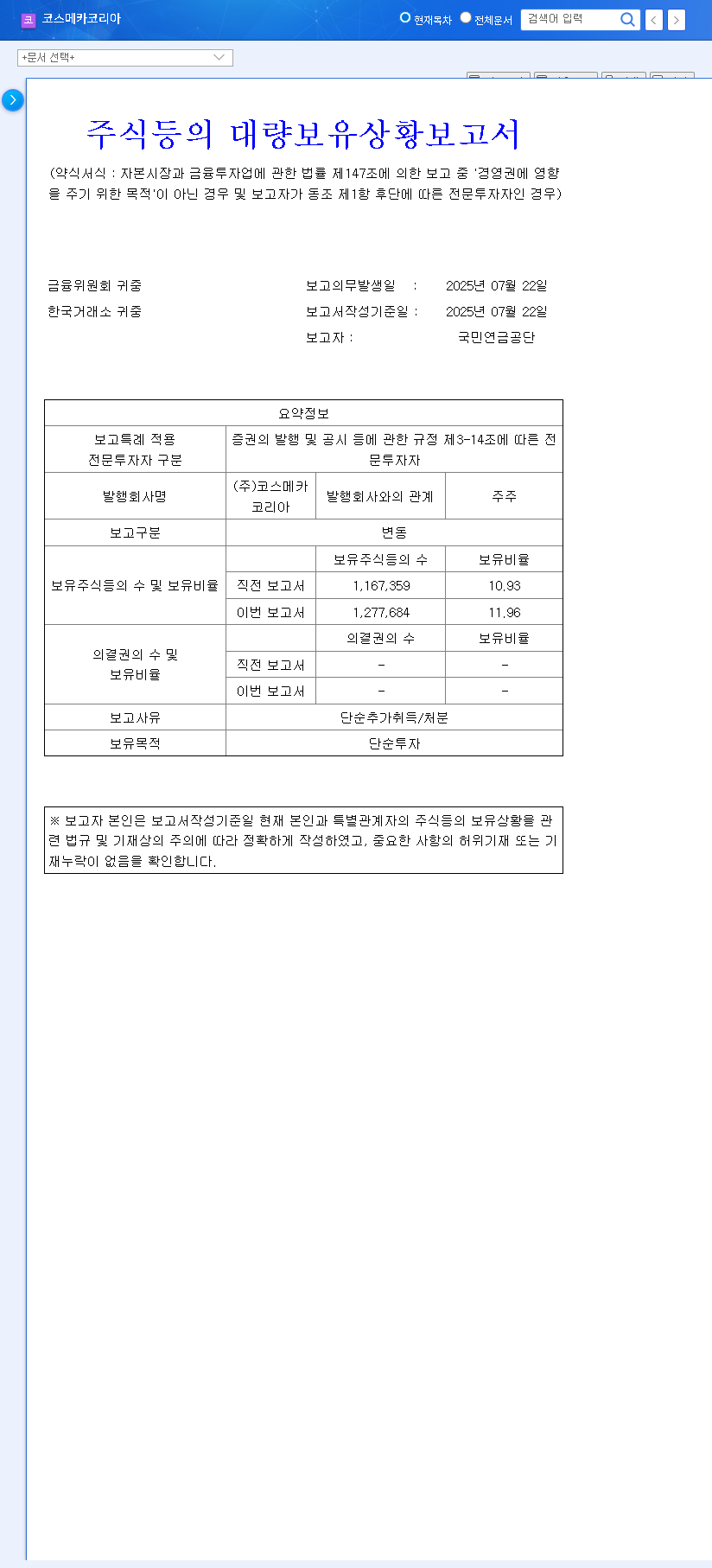

According to an official disclosure dated October 1, 2025, the National Pension Service acquired additional shares of Cosmecca Korea, raising its total holding from 10.93% to 11.96%. You can view the Official Disclosure on DART for verification. This seemingly small percentage increase carries substantial weight in the market for several key reasons:

- •Positive Market Signal: An increased stake from a respected institution like the NPS is a powerful endorsement of Cosmecca Korea’s financial health and future growth prospects.

- •Improved Investor Sentiment: This confidence can trigger a ripple effect, encouraging other individual and institutional investors to view the stock more favorably, potentially driving upward price momentum.

- •Enhanced Liquidity: Active trading by a major pension fund can improve the stock’s liquidity and trading volume, making it more attractive to a wider range of investors.

A Deep Dive into Cosmecca Korea’s Financial Health

To understand why the NPS is bullish on Cosmecca Korea, we must look beyond the headlines and into its core fundamentals. As a global cosmetics Original Design Manufacturer (ODM) and Original Equipment Manufacturer (OEM), the company is a key player in the supply chain for many leading beauty brands.

Robust Performance and Strategic Strengths

Based on the H1 2025 consolidated report, Cosmecca Korea demonstrates a solid financial foundation. Revenue reached KRW 280.1 billion, with a healthy operating profit of KRW 35.3 billion. The company’s competitive edge is built on:

- •Global Production Footprint: With advanced manufacturing bases in Korea, China, and the USA (through the strategic acquisition of Englewood Lab), it serves a diverse international clientele.

- •Innovation and R&D: R&D investment saw a significant jump to 4.9% of revenue in H1 2025. This commitment fuels product development aligned with major market trends like clean beauty and cosmeceuticals, securing future growth engines.

- •Operational Efficiency: Its proprietary OGM (Original Global Standard development and Manufacturing) and CPS (Creative Product Solution) systems ensure high quality and production efficiency.

Financial Stability: A Point of Caution

While performance is strong, investors should note the Debt-to-Equity ratio, which stood at 99.05% at the end of H1 2025. This increase from the previous year suggests a need for careful management of financial leverage. For more on this metric, authoritative sources like Investopedia offer detailed explanations. Continuous monitoring of this figure will be crucial in assessing long-term stability.

Cosmecca Korea’s commitment to R&D and its expanding global presence, particularly in the US market, are key pillars supporting its growth narrative, despite the need for prudent financial management.

Macroeconomic Tailwinds and Headwinds

No company operates in a vacuum. The broader economic landscape presents both opportunities and challenges for Cosmecca Korea.

- •Favorable Currencies & Interest Rates: A stable USD/KRW exchange rate is beneficial for export competitiveness. Furthermore, declining policy rates in both the US and South Korea reduce borrowing costs, positively impacting the bottom line.

- •Stable Input Costs: International oil prices (WTI) have remained relatively stable, limiting volatility in raw material procurement costs.

- •Logistics Cost Pressure: A key headwind is the rising China Container Freight Index. This indicates a potential increase in shipping and logistics expenses, which could squeeze profit margins if not managed effectively. This is a critical risk factor to monitor.

Investment Outlook & Strategy

Considering all factors, what is the verdict on Cosmecca Korea stock? The NPS investment acts as a powerful catalyst, strengthening market confidence. Combined with solid performance and a clear strategy for tapping into the booming K-beauty market, the mid-to-long-term outlook appears positive.

Key Takeaways for Investors

- •Short-Term: The NPS news provides positive momentum. Traders may look for short-term price appreciation driven by improved sentiment.

- •Long-Term: The investment case is based on fundamental strengths—global expansion, R&D leadership, and operational excellence. Long-term investors should feel encouraged but must monitor key risks.

- •Points to Monitor: Keep a close watch on quarterly earnings, future changes in NPS holdings, trends in the debt-to-equity ratio, and fluctuations in global freight costs.

In conclusion, the National Pension Service’s increased stake reinforces an already compelling growth story for Cosmecca Korea. While risks related to financial leverage and logistics costs require vigilance, the company’s strong fundamentals and strategic direction make it an attractive name for investors’ watchlists.