This in-depth analysis of the PUM-TECH KOREA Q3 2025 earnings report dissects the company’s latest performance. As a key player in the global K-Beauty packaging and health food sectors, PUM-TECH KOREA’s financial health is a critical indicator for investors. While the company posted year-over-year growth, its results fell short of market consensus, prompting questions about its future trajectory. We will explore the core numbers, uncover the underlying factors driving performance, and provide a clear outlook for the PUM-TECH KOREA stock.

PUM-TECH KOREA Q3 2025 Earnings: The Official Numbers

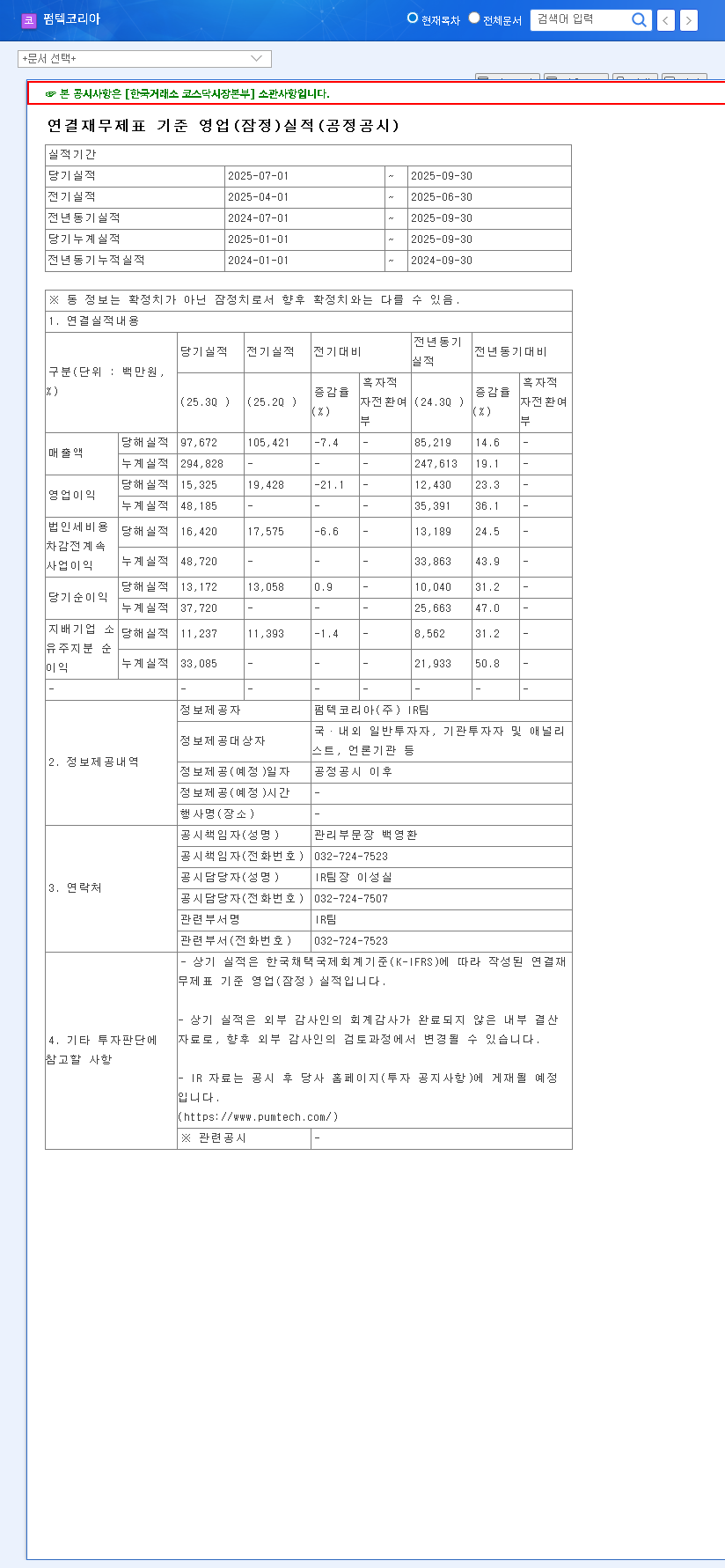

On November 7, 2025, PUM-TECH KOREA released its preliminary consolidated financial results for the third quarter. While demonstrating solid growth compared to the previous year, the figures slightly missed the high expectations set by market analysts. The full details can be reviewed in the company’s Official Disclosure filed with DART.

Here is a summary of the key performance indicators:

- •Revenue: KRW 97.7 billion (a 14.7% YoY increase, but 1.0% below estimates).

- •Operating Profit: KRW 15.3 billion (a 23.4% YoY increase, but 5.0% below estimates).

- •Net Income: KRW 11.2 billion (a 10.7% YoY increase, but 8.2% below estimates).

The discrepancy, especially in operating profit and net income, suggests that while top-line growth remains healthy, cost pressures or non-operating expenses may be impacting the bottom line more than anticipated.

Despite missing quarterly estimates, PUM-TECH KOREA’s double-digit year-over-year growth underscores its resilient business model. The key for investors is to differentiate between temporary headwinds and a structural shift in fundamentals.

Fundamental Analysis: Growth Drivers vs. Potential Risks

A balanced PUM-TECH KOREA analysis requires looking beyond the headline numbers. Several factors contribute to the company’s current position and future outlook.

Positive Catalysts & Core Strengths

- •Dominance in K-Beauty Packaging: The cosmetic container division remains the company’s powerhouse. Fueled by the relentless global demand for K-Beauty, PUM-TECH’s innovative and high-quality packaging solutions are sought after by top brands. The growing trend toward sustainable and eco-friendly packaging, as detailed in reports by market research firms, presents another significant growth avenue.

- •Strategic Health Food Expansion: The acquisition of JALLON NATURAL Co., Ltd. is a strategic diversification into the high-growth health functional food market. This segment is showing gradual revenue contribution and offers synergy potential with the core business through packaging and distribution.

- •Solid Financial Foundation: The company maintains a healthy balance sheet with a favorable debt-to-equity ratio and consistent positive operating cash flow, providing stability and the capacity for future investment.

Headwinds and Investor Concerns

- •Subsidiary Impairment Charges: A key reason for the profit miss appears to be the recognition of impairment losses related to investments in its subsidiary, JALLON NATURAL. This suggests that the subsidiary’s profitability may be weaker than initially projected, raising concerns about the acquisition’s short-term success.

- •Macroeconomic Pressures: Volatility in raw material prices (like plastics and resins) and fluctuating currency exchange rates can directly squeeze profit margins. A global economic slowdown could also temper consumer demand for cosmetics, impacting sales. For more information, see our guide on navigating economic cycles as an investor.

- •Intensifying Competition: The K-Beauty packaging landscape is highly competitive. While PUM-TECH is a leader, constant innovation is required to maintain its edge and pricing power against both domestic and international rivals.

Investment Outlook: What’s Next for PUM-TECH KOREA Stock?

The market’s immediate reaction to the PUM-TECH KOREA Q3 2025 earnings miss is likely to be negative, potentially causing short-term pressure on the stock price. However, savvy investors will look deeper.

The central question is whether the profit miss is due to temporary, one-off events (like the impairment charge) or a more concerning structural decline in profitability. If the core cosmetics business continues its strong export-led growth and the company can effectively manage costs and integrate JALLON NATURAL, the long-term thesis remains intact.

Key points for investors to monitor in the upcoming quarters:

- •Company guidance on the reasons for the earnings miss and margin pressures.

- •Performance and growth strategy for the JALLON NATURAL health food division.

- •Management’s strategies for mitigating raw material cost inflation and currency risks.

In conclusion, while the Q3 2025 results introduce a note of caution, PUM-TECH KOREA’s fundamental strengths in a growing market are undeniable. A cautious, long-term approach is recommended, with investors closely watching for signs of improved profitability and successful strategic execution in the quarters ahead.