The path forward for the EDGC rehabilitation plan has become significantly more perilous. Eone Diagnomics Genome Center Co., Ltd. (EDGC), a genomics diagnostics company already navigating a complex corporate rehabilitation, has been hit with a devastating legal setback. The recent loss of a KRW 4.8 billion penalty lawsuit has sent shockwaves through its investor community, casting a dark shadow over the company’s prospects for recovery. This comprehensive analysis will dissect the lawsuit’s implications, explore the dire financial reality facing EDGC, and provide a clear-eyed view for current and potential investors.

Deep Dive: The KRW 4.8 Billion Lawsuit Ruling

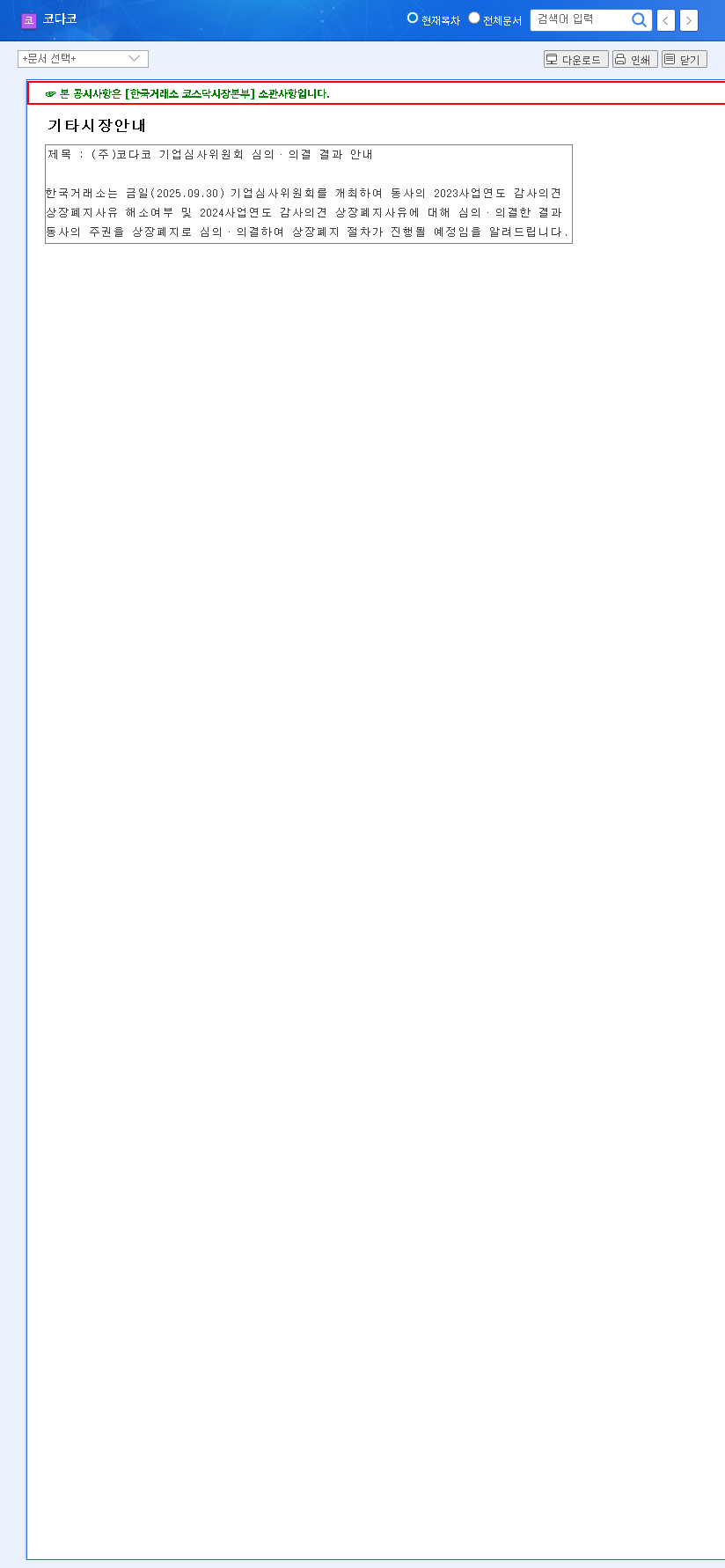

The Seoul High Court delivered an unfavorable ruling against EDGC in a ‘penalty claim lawsuit’ (Case No. 2025나207292) filed by Bitgwaelek Co., Ltd. This decision overturned a more favorable first-instance judgment, confirming an outstanding rehabilitation claim of KRW 4.8 billion. Compounding the financial blow, the court mandated an annual interest rate of 12% on this amount, accruing from July 8, 2023, until the debt is fully repaid. This substantial sum represents approximately 14.6% of EDGC’s total assets (based on 2022 financials) and adds a massive, unplanned liability to its balance sheet. The Official Disclosure on the DART system confirms these details, leaving no room for ambiguity about the severity of this financial obligation.

A Company on the Brink: EDGC’s Dire Financial State

This lawsuit could not have come at a worse time. The EDGC financial crisis is not a new development; the company has been in a precarious position for some time. The commencement of corporate rehabilitation procedures already raised significant doubts about its ability to continue as a ‘going concern’—a foundational principle of business valuation. An examination of its mid-year 2025 report reveals a catastrophic decline across all key metrics:

With current liabilities far exceeding current assets, EDGC is facing a severe short-term liquidity crisis. The company’s ability to meet its immediate financial obligations is under extreme threat, even before accounting for this new KRW 4.8 billion debt.

Revenue streams have all but dried up. Genomics diagnostic services, once a core business, saw revenues plummet by 53%. Product sales have collapsed by a staggering 97%, and its venture into health functional foods has dropped to zero. This isn’t just a slump; it’s a systemic failure across its primary business segments. The financial statements paint an equally grim picture: total equity has dwindled to just KRW 6.4 billion, while total assets have fallen by 60% to KRW 52.7 billion. The widening consolidated operating loss of KRW 8.2 billion and a net loss of KRW 12.2 billion for the half-year underscore the company’s inability to generate profit.

The Ripple Effect on the EDGC Rehabilitation Plan

Complicating an Already Fragile Process

A successful corporate rehabilitation hinges on a carefully crafted plan to restructure debt and restore operational viability. The introduction of a new, significant KRW 4.8 billion claim fundamentally alters the equation. This additional liability complicates negotiations with existing creditors, who must now account for a larger pool of debt being repaid from the same limited assets. The process of gaining creditor approval for the EDGC rehabilitation plan, already a challenging task, has now become exponentially more difficult. For more information on this process, you can read about the key steps in corporate rehabilitation. This development could also deter potential third-party acquirers or investors who might have been considering a buyout as part of the recovery strategy.

Market Outlook & Investor Advisory

The market’s reaction is expected to be swift and negative. Investor confidence, already shattered by the rehabilitation filing, will likely erode further. The materialization of this legal risk confirms worst-case scenarios and could trigger intensified selling pressure on EDGC stock. Investors must consider the following impacts:

- •Increased Financial Burden: The debt plus accumulating interest creates a significant cash outflow requirement that the company, in its current state, simply cannot meet.

- •Eroding Investor Confidence: This ruling validates legal and financial risks, likely causing a further flight of capital and stakeholder trust.

- •Heightened Stock Volatility: The stock is subject to extreme volatility and delisting risk, a common outcome for companies that fail to exit rehabilitation successfully, as outlined by the Korea Exchange (KRX) listing regulations.

- •Risk of Total Loss: If the rehabilitation process fails, there is a very real possibility of a total loss of investment capital for equity holders.

Frequently Asked Questions (FAQ)

What is the core issue facing Eone Diagnomics (EDGC)?

EDGC, already undergoing corporate rehabilitation, has lost a lawsuit resulting in a new KRW 4.8 billion debt plus 12% annual interest. This severely worsens its already critical financial situation and jeopardizes its chances of a successful recovery.

How does this lawsuit affect the EDGC rehabilitation process?

The massive new debt complicates the entire rehabilitation plan. It makes it harder to secure approval from creditors, deters potential buyers, and places an almost insurmountable financial strain on the company’s limited resources.

Is investing in EDGC stock a good idea now?

Investing in EDGC at this stage carries an extremely high level of risk. The combination of ongoing rehabilitation, collapsing fundamentals, and a new major legal liability creates a highly volatile and uncertain environment. There is a significant possibility of total investment loss if the rehabilitation fails. Extreme caution is strongly advised. Investors should focus on the outcome of the legal and rehabilitation processes, not on speculative recovery potential.