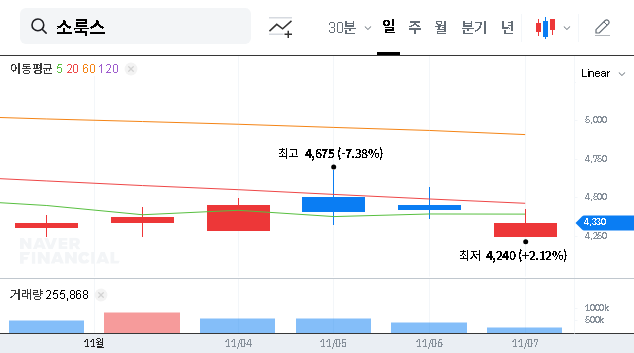

In a surprising move that caught investors’ attention, Solux Co., Ltd. (290690) has abruptly withdrawn its decision to acquire ₩15 billion in tangible assets. This reversal, announced just two weeks after the initial resolution, raises significant questions about the company’s strategy, financial stability, and the future of Solux stock. For investors navigating this uncertainty, a deep understanding of the situation is paramount. This comprehensive analysis will dissect the event, examine the underlying weaknesses in Solux’s fundamentals, and evaluate the short and long-term impact on the company’s valuation and stock performance, providing the critical insights needed for informed investment decisions.

The Canceled Deal: What Exactly Happened?

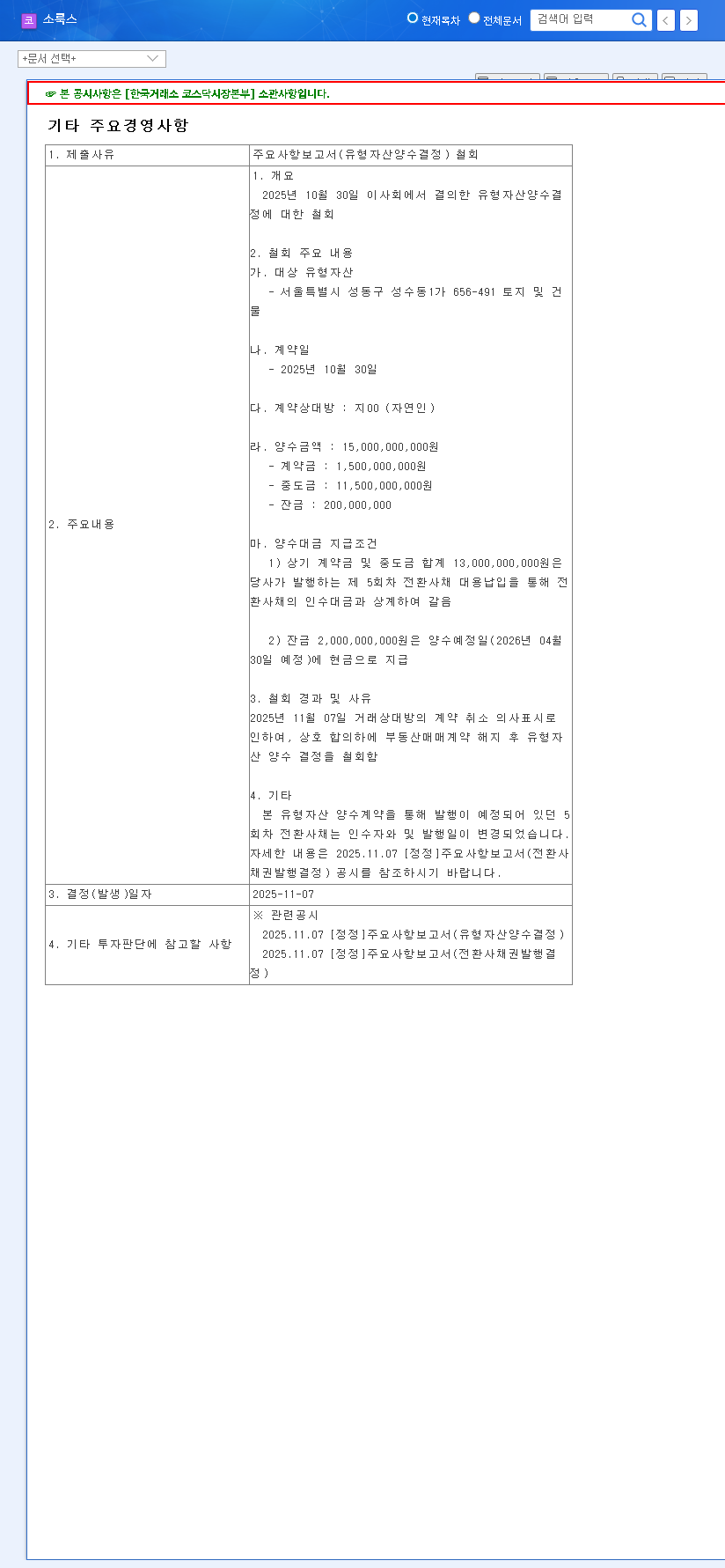

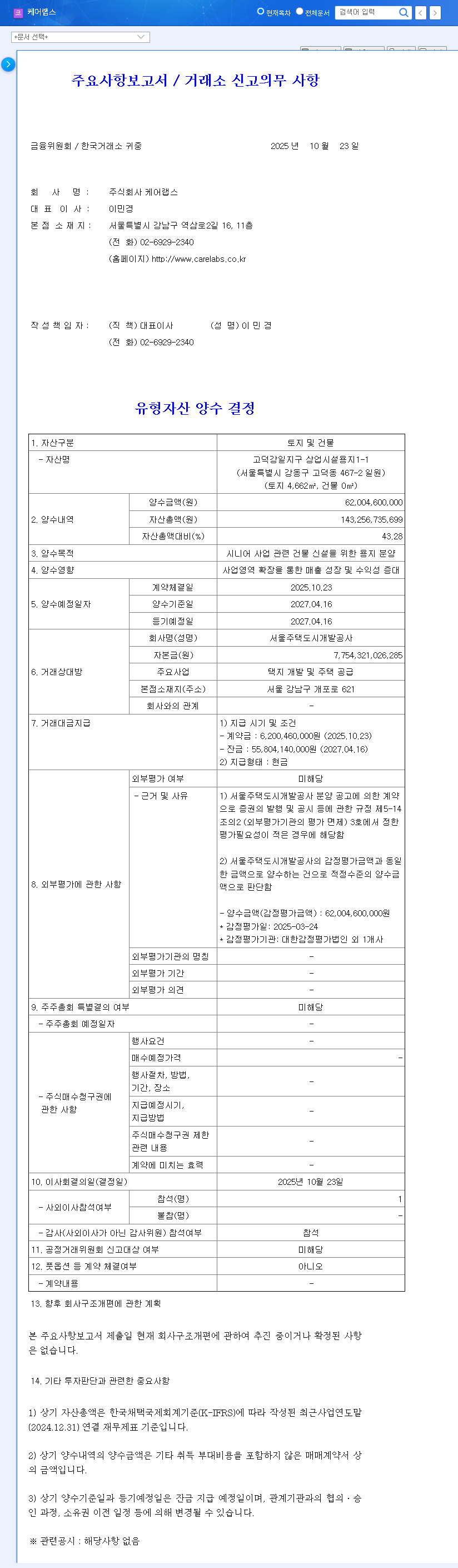

On October 30, 2025, the board of directors for Solux Co., Ltd. resolved to acquire land and buildings in the strategic Seongsu-dong area of Seoul, a deal valued at ₩15 billion KRW. However, this plan was short-lived. By November 7, 2025, the company announced the complete withdrawal of this resolution. According to the official disclosure, the reversal stemmed from a mutual agreement to terminate the contract after the counterparty expressed an intent to cancel. You can view the Official Disclosure on DART for verification. This cancellation also directly impacts the planned financing method, which involved an in-kind payment using the 5th series of convertible bonds, complicating the company’s capital management strategy.

Decoding the Reversal: A Look at Solux’s Unstable Fundamentals

This sudden Solux asset acquisition withdrawal isn’t an isolated event; it’s a symptom of deeper, more systemic issues within the company’s financial structure. Understanding these underlying problems is key to performing a thorough 290690 stock analysis.

- •Deteriorating Profitability: Despite growth in sales and capital in the first half of 2025, Solux reported significant losses in both operating and net income. This points to bloated selling, general, and administrative (SG&A) expenses and potentially inefficient investment activities that are failing to generate returns.

- •Weakened Financial Position: The company’s financial health is being eroded by rising financial expenses, particularly from investments in associates and the issuance of convertible bonds. This increases leverage and makes the company more vulnerable to market shocks.

- •Intense Core Business Competition: A two-year decline in sales, culminating in operating losses, suggests that Solux is struggling in its core lighting business. The company may be losing market share or failing to adapt to evolving consumer demands and technological shifts.

- •Burdensome New Ventures: Strategic investments aimed at diversification, such as the stake in Aribio Co., Ltd., are creating a significant short-term financial drain. Impairment losses and delayed viability assessments for these new businesses are negatively impacting the company’s balance sheet.

- •Risk of Share Dilution: The frequent issuance of convertible bonds and stock options creates a persistent overhang on the stock. This potential for future share dilution can suppress the stock price and deter new investors. For more on this, you can read about the impact of convertible bonds on stock prices.

While the canceled deal avoids a ₩15 billion expenditure, it fails to address the core operational inefficiencies and financial weaknesses plaguing Solux Co., Ltd. The company’s path forward depends on fundamental reform, not just canceled transactions.

Analyzing the Impact on Solux Co., Ltd. (290690) Stock

Short-Term Repercussions

In the immediate term, the withdrawal presents a mixed bag. On the positive side, it alleviates the ₩15 billion financial burden, reducing immediate cash outflow and the dilutive pressure from the associated convertible bonds. However, it also signals disarray in the company’s strategic planning and fund management. This abrupt reversal, occurring so soon after a board resolution, could damage management’s credibility among institutional investors and create uncertainty around future projects.

Mid- to Long-Term Outlook

Looking ahead, the long-term trajectory of Solux stock depends entirely on whether management can tackle its fundamental problems. The canceled deal does not fix the operating losses or excessive spending. The key drivers for future value will be the company’s ability to strengthen its core lighting business, achieve tangible success from its new ventures like Aribio, and prudently manage its capital structure, especially concerning its convertible bonds. Without clear progress in these areas, the stock is likely to face continued headwinds, as noted by market analysts at authoritative financial news sources.

Investment Strategy: Key Factors to Watch

For current and prospective investors in Solux Co., Ltd. (290690), this event should be viewed as a neutral-to-negative signal. A cautious approach is warranted. Focus should shift from this single event to the broader operational picture. Monitor the following key areas closely in upcoming quarterly reports:

- •Path to Profitability: Look for concrete evidence of cost controls and a return to operating profit in the core business.

- •New Business Performance: Demand tangible results and revenue generation from new ventures, not just investment announcements.

- •Financial Health: Track debt levels, financial costs, and any further plans for issuing convertible bonds that could dilute equity.

- •Management Strategy: Assess the coherence and execution of the company’s long-term strategy in official communications.

In conclusion, the withdrawal of the asset acquisition is a significant development, but it’s merely a headline. The real story for Solux Co., Ltd. (290690) lies in its ability to execute a fundamental turnaround. Until clear evidence of such a turnaround emerges, investors should remain vigilant and cautious.