The recent announcement regarding the Dongjin Semichem company split has generated significant buzz in the investment community. This pivotal restructuring separates the core business into two specialized entities: the surviving Dongjin Semichem, focused on high-growth electronic materials, and the newly formed Dongjin Innovachem, dedicated to the foaming agents business. Far more than a simple division, this is a calculated strategy to unlock specialization, drive innovation, and ultimately enhance shareholder value. For investors, understanding the nuances of this split is critical. According to the Official Disclosure, this move is designed to create two more agile and competitive companies. This comprehensive analysis will explore the strategic rationale, dissect the prospects of each new entity, and provide a clear action plan for making informed investment decisions.

The Core Strategy Behind the Dongjin Semichem Company Split

A corporate spin-off or split is a powerful tool used to streamline operations and unlock hidden value. The primary motivation for the Dongjin Semichem company split is to create two distinct, highly focused organizations that can better navigate their respective markets. This strategic uncoupling allows each business to pursue tailored growth strategies, allocate capital more efficiently, and respond with greater agility to industry-specific challenges and opportunities.

Sharpening Business Focus and Specialization

The electronic materials and foaming agents markets have vastly different dynamics. The former is driven by rapid technological innovation and deep integration with semiconductor giants, while the latter relies on scale, supply chain efficiency, and industrial application. By separating them, each management team can concentrate its expertise and resources on securing a competitive advantage in its specific global market, without being constrained by the priorities of the other division.

Maximizing Management Efficiency and Agility

A leaner corporate structure fosters faster, more professional decision-making. The new entities will be able to react swiftly to market shifts, customer demands, and technological breakthroughs. This improved management efficiency is crucial for both the high-velocity electronics sector and the competitive industrial materials space, leading to more effective implementation of business-specific strategies and a better allocation of resources.

The ultimate goal of this strategic division is clear: to foster long-term, sustainable growth for both companies, which in turn is expected to significantly enhance corporate and shareholder value.

A Tale of Two Companies: Post-Split Deep Dive

Following the split, investors will hold shares in two distinct companies, each with its own unique profile and growth trajectory. Let’s analyze what the future holds for each.

1. The New Dongjin Semichem: A Titan in Electronic Materials

The surviving entity, Dongjin Semichem, will consolidate its position as a powerhouse in the electronic materials business. It will continue supplying core materials for the ever-expanding semiconductor and display industries. Its competitive edge lies in its ability to co-develop solutions with major manufacturers and its in-house synthesis capabilities. With the robust growth of the global semiconductor market and expanding display demand, particularly from China, stable revenue growth is anticipated. Furthermore, its investment into renewable energy is a key long-term catalyst. R&D in areas like fuel cells (MEA manufacturing) and secondary batteries (CNT conductive materials, silicon anode materials) could unlock significant new revenue streams and position the company at the forefront of green technology. You can learn more about related industry trends in our analysis of the semiconductor market.

2. Dongjin Innovachem: Forging a New Path in Foaming Agents

The newly established Dongjin Innovachem will inherit the foaming agents business, providing it with an independent foundation for growth. Its products are essential in diverse industries like footwear, construction materials, and automotive interiors, offering a stable revenue base. The key growth driver to watch is the commercialization of Microspheres, a high-value-added product with the potential to significantly boost sales and profitability. An efficient supply chain, supported by its Indonesian subsidiary, will help maintain a competitive edge in the global market.

Financial Outlook & What to Expect for Dongjin Semichem Stock

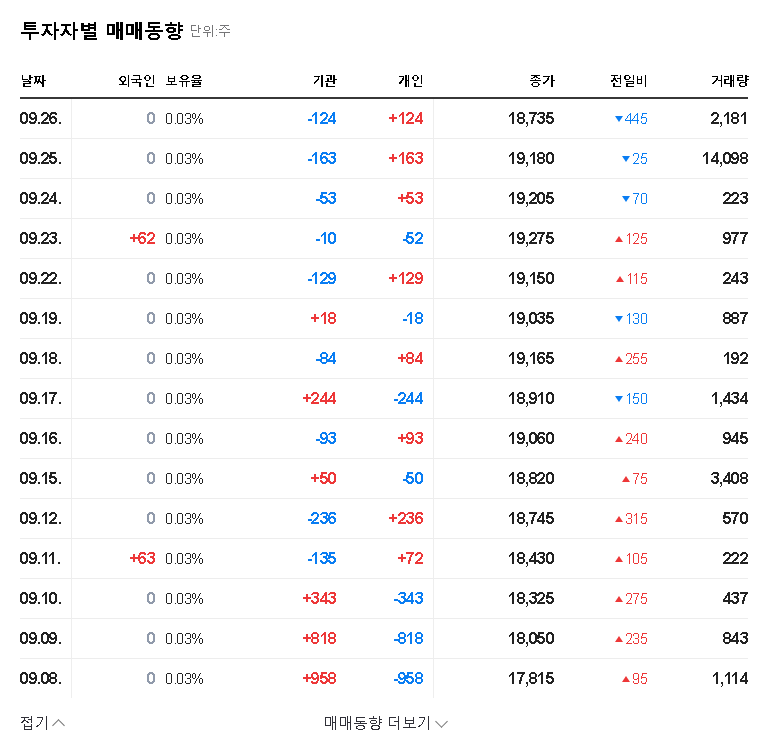

Recent financial performance has been strong, with first-half sales reaching 744.9 billion KRW and operating profit hitting 112.3 billion KRW, showcasing solid fundamentals. Post-split, each company’s independent growth is expected to maintain this positive trajectory. From a market perspective, the enhancement of corporate value through specialization is expected to have a positive long-term impact on the Dongjin Semichem stock price (and the new Dongjin Innovachem stock). However, investors should be prepared for potential short-term volatility as the market digests the split. Over time, the stock prices of the two companies will likely diverge based on their individual performance, a concept well-explained by experts at high-authority financial sites like Investopedia.

Investor Action Plan: Navigating the Split

While the long-term outlook is promising, proactive monitoring is key. Here are the crucial points for investors to focus on during this transition:

- •Monitor Split Execution: Ensure the split process unfolds smoothly and according to the announced timeline. Any delays or complications could introduce uncertainty.

- •Analyze Segment Performance: Once separated, closely track the quarterly financial reports and business performance of both Dongjin Semichem and Dongjin Innovachem to evaluate their independent progress.

- •Track Renewable Energy Milestones: For Dongjin Semichem, progress in its renewable energy R&D (fuel cells, batteries) will be a critical indicator of its long-term growth potential beyond its core business.

- •Observe Macroeconomic Factors: Keep an eye on variables like raw material costs, currency exchange rates, and interest rates, as these can impact the profitability of both new entities.

In conclusion, the Dongjin Semichem company split represents a significant and strategic turning point. By creating two specialized, agile companies, it paves the way for focused growth and enhanced competitiveness. For investors with a long-term perspective, this strategic realignment could present a compelling opportunity to capitalize on the distinct potential of both the electronic materials and foaming agents markets.