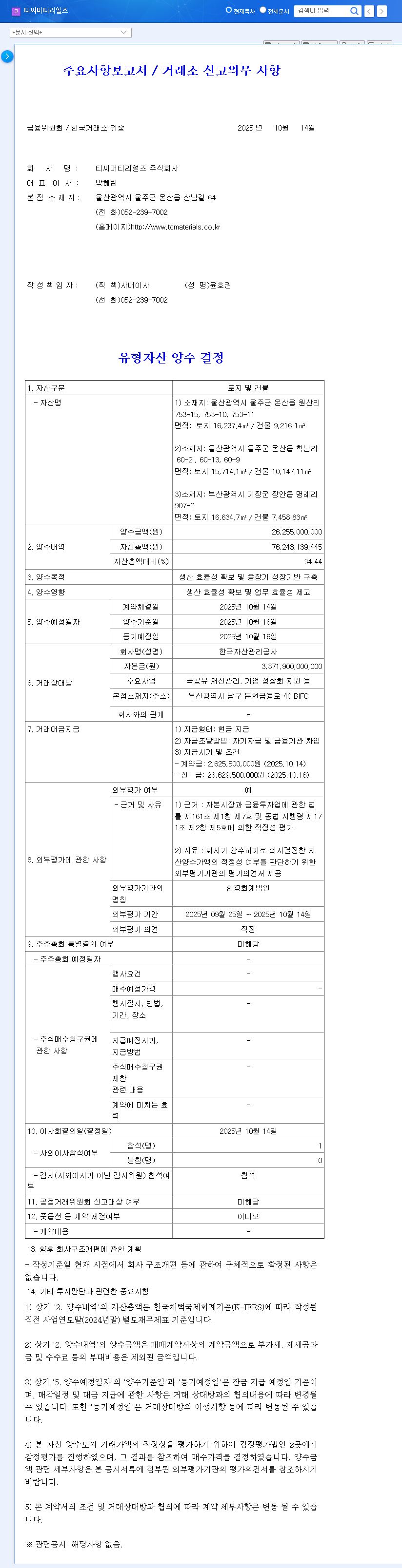

In a significant move capturing market attention, TC Materials Co., Ltd. (티씨머티리얼즈) has announced a landmark decision to acquire tangible assets valued at ₩26.3 billion. This strategic investment, representing a substantial 34.44% of the company’s equity, is far more than a simple transaction. It signals a pivotal moment for the company’s future, raising a critical question for investors: Is this the catalyst for long-term growth or a short-term financial burden? This comprehensive analysis of the TC Materials asset acquisition will dissect the corporate fundamentals, market dynamics, and macroeconomic indicators to provide you with the clarity needed for sound investment decisions.

We will explore the profound implications of this acquisition, weigh the opportunities against the risks, and outline a clear investment strategy to help you navigate potential stock price fluctuations. Join us as we delve into the future of TC Materials.

Breaking Down the TC Materials Asset Acquisition

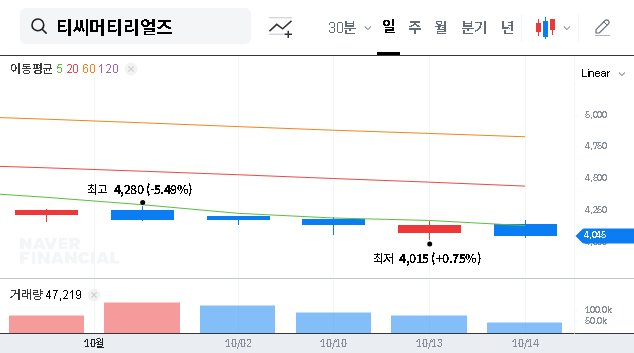

On October 14, 2025, TC Materials officially disclosed its decision to acquire significant tangible assets, a move seen as a cornerstone for its future operational capacity and strategic positioning. The specifics of this pivotal investment are crucial for understanding its potential impact.

Key Details of the Transaction

- •Event: Decision to acquire tangible assets (land and buildings) from the Korea Asset Management Corporation.

- •Value: ₩26.3 billion, equivalent to 34.44% of the company’s total equity.

- •Assets: Land and buildings located in Ulsan and Busan, totaling approximately 95,000㎡.

- •Purpose: Officially stated as a strategic investment to enhance production efficiency and establish a mid-to-long-term growth foundation.

- •Funding: A combination of the company’s own capital and loans from financial institutions. The final cash payment of ₩23.629 billion is due on October 16, 2025.

- •Official Disclosure: The complete details can be reviewed in the Official Disclosure (DART report).

Current State: Corporate Health & Market Environment

To grasp the full weight of this investment, we must first analyze TC Materials’ current financial standing and the broader economic landscape it operates within.

Company Financial Snapshot (H1 2025)

TC Materials operates primarily in Power Infrastructure (56.76%), Automotive Materials (20.74%), and Home Appliances (18.06%). However, its recent performance shows signs of strain:

- •Revenue: ₩144.865 billion (a slight year-over-year decrease).

- •Operating Profit: ₩3.807 billion (a significant decline).

- •Net Income: -₩1.391 billion (shifted to a deficit).

- •Key Concern: A substantial financial burden from existing borrowings and outstanding convertible bonds continues to weigh on net income. For more on this, you can read our guide on how convertible bonds impact investors.

Macroeconomic Headwinds

The external environment presents additional challenges. Rising government bond yields, as reported by authoritative sources like Bloomberg, suggest that borrowing costs for the new loans could be higher than anticipated. Furthermore, climbing crude oil prices and shipping indexes point to increased costs for raw materials like copper, potentially squeezing profit margins further.

Impact Analysis: Opportunities vs. Risks

This tangible asset investment is a double-edged sword, presenting both a clear path to growth and significant financial risks.

This large-scale investment can be seen as a proactive commitment from management to drive future growth, but it arrives at a time of underlying financial weakness, creating a classic risk/reward scenario for investors.

The Bull Case (Positive Implications)

- •Enhanced Production Efficiency: New facilities can streamline manufacturing, automate processes, and expand capacity, leading to long-term cost reductions.

- •Foundation for Growth: The investment strengthens TC Materials’ ability to meet rising demand in high-growth sectors like electric vehicle components and power grid modernization.

- •Increased Asset Base: Expanding tangible assets can improve the company’s long-term financial structure and borrowing capacity if it translates to higher revenue.

The Bear Case (Negative Risks)

- •Short-Term Liquidity Strain: The ₩26.3 billion outlay is a massive expenditure that could strain cash flow, especially when combined with existing debt.

- •Increased Debt Burden: Taking on new loans on top of existing convertible bonds elevates financial risk and interest expenses, which could further suppress net income.

- •Delayed ROI: The positive effects on profitability are not immediate. Unexpected costs and a slow ramp-up period could delay the return on investment.

- •Weak Underlying Performance: Making a large investment while revenue is declining and the company is at a net loss is a bold, but risky, strategy that could amplify negative sentiment if performance doesn’t improve quickly.

Investment Strategy & Stock Outlook

Given these conflicting factors, a nuanced investment strategy is essential. The TC Materials stock outlook hinges on management’s ability to execute its vision without succumbing to financial pressures.

Short-Term Outlook (3-6 Months)

The stock price is likely to face downward pressure. The significant cash payment due in October, combined with current performance weakness and broader market concerns about interest rates, could create volatility and negative sentiment. Investors should anticipate potential price adjustments.

Mid-to-Long-Term Outlook (1-3 Years)

The long-term success of this acquisition depends entirely on execution. If TC Materials can leverage the new assets to improve margins, capture new contracts, and show a clear path to profitability, the investment will be a significant long-term positive for corporate value and the stock price.

Recommendations for Investors

- •Cautious Buy: For new investors, the long-term potential is appealing. However, it is prudent to wait for the short-term volatility to subside. Monitor the company’s Q4 2025 and Q1 2026 earnings reports for signs of improving operational efficiency before committing capital.

- •Hold: For existing shareholders, this event validates a long-term growth thesis. It may be wise to hold through the short-term turbulence and focus on management’s execution of their strategic plan.

- •Monitor Closely: All investors should watch for specific details on loan terms, the new facility’s operational roadmap, and any changes in the competitive landscape.

In conclusion, the TC Materials asset acquisition is a transformative bet on the company’s future. While it bolsters long-term growth prospects, the immediate financial risks are undeniable. Prudent investors will weigh these factors carefully, stay informed, and make strategic decisions based on execution rather than speculation.