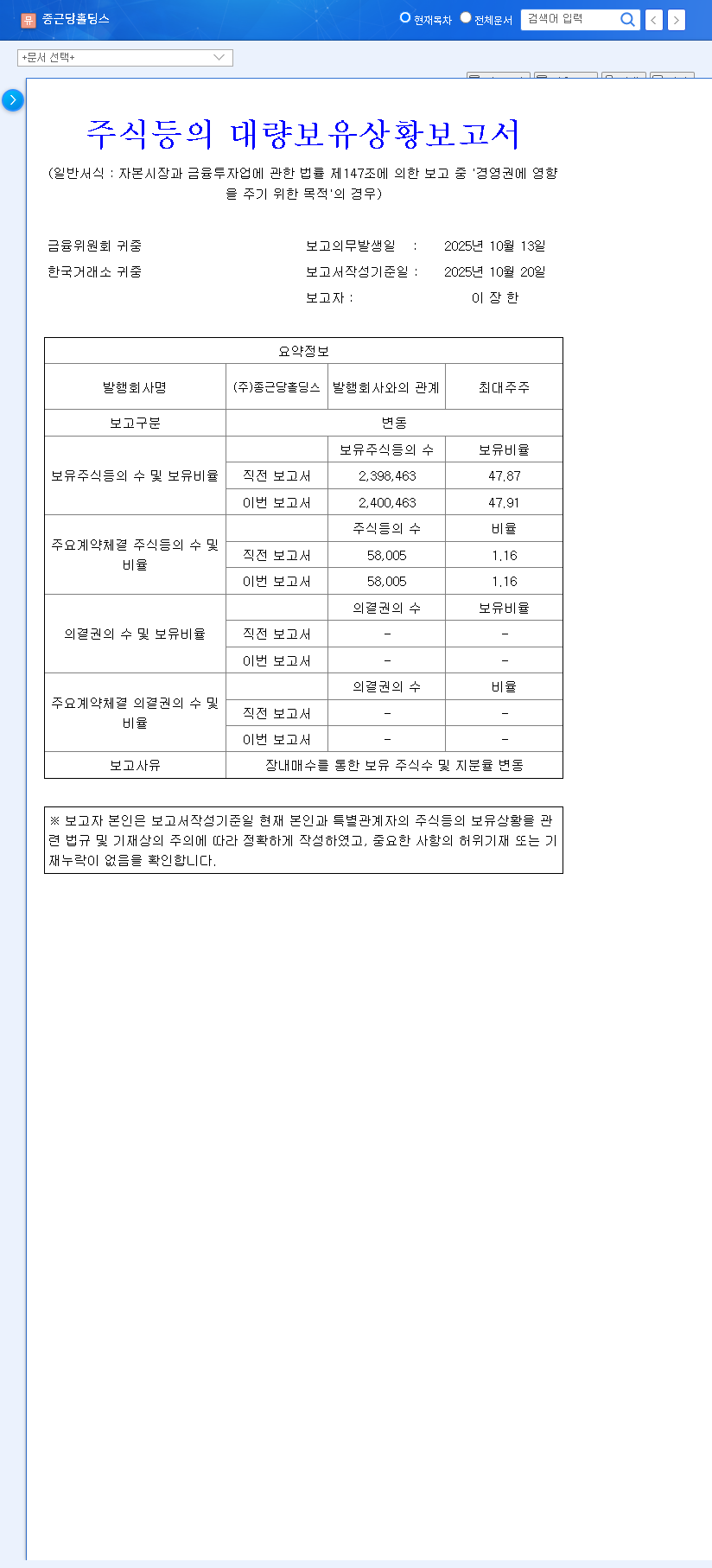

The recent CHONGKUNDANG HOLDINGS CORP. stake change has sent a subtle but significant signal to the market. When a controlling shareholder like CEO Lee Jang-han increases their position, even slightly, investors take notice. The explicitly stated purpose of ‘management control influence’ transforms this minor transaction into a critical event worthy of deep analysis. This guide unpacks the details, explores the potential strategic motives, and provides a clear action plan for investors monitoring CKD Holdings’ stock.

Understanding the nuances of insider transactions is key to anticipating corporate direction. Let’s delve into what this move could mean for the company’s future and your investment portfolio.

The Core Transaction: A Detailed Look

According to a recent filing, the key details of the shareholding change are straightforward but packed with meaning. Here’s a breakdown based on the official report:

- •Reporter: Lee Jang-han (CEO)

- •Purpose of Holding: Management control influence

- •Transaction: On-market purchase of 2,000 common shares

- •Resulting Change: Shareholding ratio increased from 47.87% to 47.91% (+0.04%p)

This transaction was executed via an entity named Bell S.M. Co., Ltd. The complete details can be verified in the Official Disclosure (Source). While the 0.04% increase appears nominal, the strategic intent behind it is what truly matters.

Why Strengthen Control? Analyzing the Motives

The phrase ‘management control influence’ is a clear declaration. For a shareholder who already holds a commanding stake, any further acquisition signals a deliberate strategic objective. Several possibilities could explain this CHONGKUNDANG HOLDINGS CORP. stake change.

In corporate finance, an insider buy, no matter the size, is often seen as the ultimate vote of confidence. It signals that leadership believes the company’s stock is undervalued and its future prospects are bright.

1. Solidifying Leadership and Stability

The most direct interpretation is a move to reinforce stable management. By increasing his stake, Mr. Lee Jang-han reduces the risk of potential challenges from other shareholders and ensures his vision for the company remains unchallenged. This is a proactive measure to guarantee stability in decision-making for long-term projects.

2. Preparing for Future Corporate Actions

A stronger controlling stake can be a prerequisite for significant corporate actions. This could include preparing for a large-scale merger or acquisition (M&A), a strategic partnership, or a major capital investment. Having unshakable control simplifies the approval process for such transformative initiatives.

3. Sending a Signal of Confidence

An on-market purchase by a CEO is a powerful signal to investors. It demonstrates personal belief in the company’s intrinsic value and future growth prospects. In a volatile market, such an action can boost investor sentiment and potentially set a floor for the stock price.

Impact on CKD Holdings Stock Price

Short-Term Outlook

Given the small transaction size (2,000 shares), a dramatic, immediate surge in the stock price is unlikely. However, the news can create a positive undercurrent. The market often interprets insider buying as a bullish signal, which could lend modest support to the stock and improve investor sentiment in the short term.

Mid-to-Long-Term Outlook

The true impact will unfold over the mid-to-long term. The significance of this stake increase will be measured by the actions that follow. If it precedes positive changes in corporate strategy, successful business expansions, or improved financial performance, it will be viewed in hindsight as a prescient move. The ‘management control influence’ purpose puts the onus on leadership to deliver results that justify this consolidation of power. For more context on market reactions, investors often consult major financial news outlets like Bloomberg for expert analysis.

Action Plan for Investors

A single data point, even an important one, should not be the sole basis for an investment decision. Prudent investors should use this event as a catalyst for further due diligence. Here’s what to monitor:

- •Continued Insider Activity: Is this an isolated purchase or the beginning of a trend? Consistent buying from Mr. Lee Jang-han would amplify the signal’s strength.

- •Corporate Communications: Watch for announcements regarding new strategic initiatives, M&A activity, or changes in dividend policy that may follow this move.

- •Fundamental Analysis: Re-evaluate CHONGKUNDANG HOLDINGS CORP.’s financial health, earnings reports, and competitive position. Strong fundamentals are essential to support any long-term stock appreciation. To learn more, consider reading our guide on effective fundamental analysis for holding companies.

- •Clarify Bell S.M. Co., Ltd.’s Role: Understanding if this entity is a related party or a third-party vehicle would provide deeper insight into the transaction’s structure.

In conclusion, while CEO Lee Jang-han’s additional purchase is a positive signal, it is best viewed as a piece of a larger puzzle. Investors should adopt a ‘watchful waiting’ approach, combining this information with rigorous fundamental analysis before making any decisive moves.