The upcoming Hyundai Department Store earnings report for Q3 2025 represents a critical juncture for investors and market analysts. On November 5, 2025, HYUNDAI DEPARTMENT STORE CO.,LTD (KRX: 069960) will unveil its performance metrics and strategic outlook in its much-anticipated Investor Relations (IR) session. This event is more than a routine financial update; it’s a comprehensive look into the company’s ability to navigate a complex economic landscape, from fierce retail competition to the promising global expansion of its subsidiaries.

This in-depth investment analysis will dissect the core pillars of Hyundai’s business, evaluate the market’s expectations, and provide a strategic roadmap for investors looking to make informed decisions about 069960 stock. Can the company solidify its premium market position, steer its duty-free segment to profitability, and capitalize on the international success of Zinus? Let’s explore the key factors to watch.

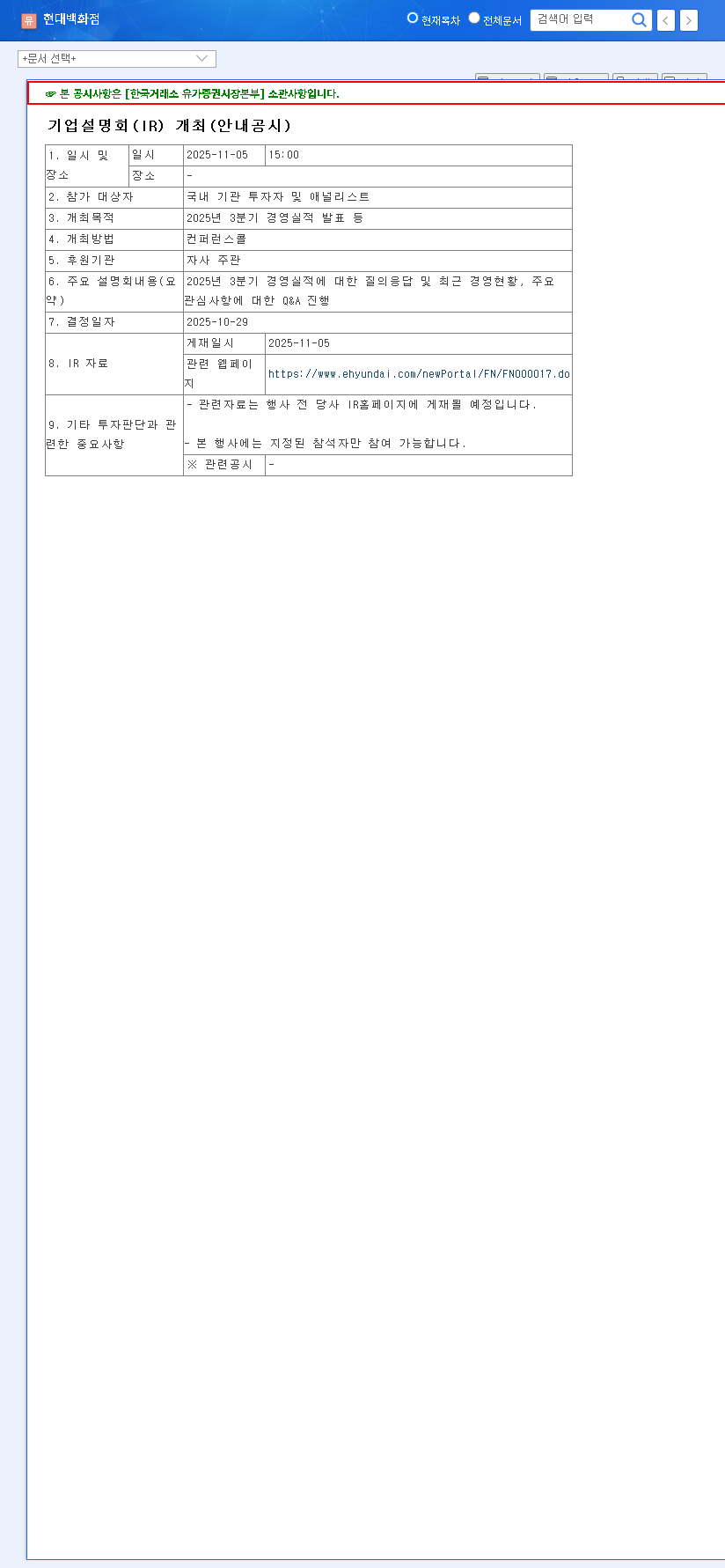

The Main Event: Q3 2025 IR Announcement Details

Mark your calendars: HYUNDAI DEPARTMENT STORE CO.,LTD has scheduled its Q3 2025 earnings release and IR session for November 5, 2025, at 3:00 PM KST. The session will provide a detailed review of third-quarter performance, an update on current management initiatives, and a crucial Q&A on future growth strategies. With a market capitalization hovering around 1.84 trillion KRW, the disclosures from this event will be closely scrutinized. The official announcement can be reviewed in the company’s regulatory filing (Official Disclosure: Click to view DART report).

This IR is a litmus test for Hyundai’s diversified strategy. The market is eager for signs of a turnaround in the duty-free business and continued momentum from Zinus to offset the highly competitive domestic retail environment.

Analyzing the Core Business Segments

A thorough investment analysis of Hyundai Department Store requires a deep dive into its three primary revenue streams. The Q3 results will provide clarity on their individual trajectories.

1. Department Store Division: The Premium Anchor

Constituting over half of the company’s revenue (52.5% in H1 2025), this division is the bedrock of the business. Its strategy hinges on premiumization and creating destination shopping experiences, exemplified by flagships like The Hyundai Seoul and upcoming projects in Busan and Gwangju. However, intense competition from rivals like Shinsegae and Lotte, coupled with shifting consumer habits towards online platforms, presents an ongoing challenge. The Q3 figures will be vital in assessing if these premium strategies are effectively protecting and growing market share.

2. Duty-Free Division: The Path to Profitability

The Duty-Free segment (26.1% of revenue) has been a drag on profitability, posting an operating loss in the first half of the year. Yet, there are silver linings. The operating loss is narrowing year-over-year, and the recovery of international travel, particularly from key markets, offers significant tailwinds. The strategic closure of the underperforming Dongdaemun store should also aid in cost consolidation. The key question for the Hyundai Q3 2025 IR will be: when can this division finally turn a profit?

3. Zinus (Furniture Division): The Global Growth Engine

The standout performer has been Zinus (21.3% of revenue), the furniture manufacturing arm acquired by Hyundai. Its innovative ‘Mattress-in-a-box’ model has resonated with consumers globally, leading to robust sales and a successful turnaround to profitability. Continued Zinus performance is crucial for Hyundai’s overall growth story. Investors will be listening for updates on its expansion into new international markets and its strategies for mitigating risks associated with raw material price volatility, a common concern in the manufacturing sector. For more on market trends, see our 2025 Global Retail Trends Report.

Financial Health and Key Risk Factors

As of mid-2025, Hyundai’s financial standing appears stable, with a manageable debt-to-equity ratio of 78.94%. However, investors must remain aware of external macroeconomic risks that could impact the bottom line.

- •Foreign Exchange Volatility: With significant foreign currency assets and liabilities, a 10% swing in exchange rates could affect profitability by an estimated 9 billion KRW.

- •Interest Rate Fluctuations: A 1% increase in interest rates could raise annual interest expenses by approximately 2 billion KRW due to variable-rate borrowings.

- •Intense Competition: The relentless competition across department stores, duty-free shops, and the online furniture market remains the most significant operational threat.

Actionable Investment Strategy Post-IR

The outcome of the Hyundai Department Store earnings call could trigger significant stock price movement. A proactive investment approach is essential.

- •Analyze the Data, Not the Noise: Wait for the official transcript and analyst reports. Focus on key metrics like same-store sales growth, operating margins for each division, and any revisions to full-year guidance. Reports from high-authority sources like Reuters can provide unbiased context.

- •Evaluate Management’s Vision: Pay close attention to the Q&A session. A confident and transparent management team with clear strategies for mitigating risks and driving growth can significantly boost long-term investor confidence.

- •Focus on Long-Term Fundamentals: Avoid knee-jerk reactions to short-term price volatility. Re-evaluate your investment thesis based on whether the company’s fundamental value and growth prospects have materially changed. Consider the valuation of 069960 stock relative to its industry peers.

In conclusion, the Q3 2025 IR is a pivotal event that will offer a clearer picture of Hyundai Department Store’s corporate health and future. By focusing on the performance of its core divisions and the clarity of its strategic path forward, investors can position themselves to make prudent and profitable decisions. We wish all investors successful trading.