Understanding the HB Investment Stock Option Exercise

The recent announcement of the HB Investment stock option exercise has captured significant investor attention. When a company like HB Investment, Inc. (440290) sees its executives exercise options, it can trigger questions about potential share dilution and short-term price pressure. However, it can also be a powerful signal of internal confidence in long-term growth. This guide provides a comprehensive venture capital analysis to help you navigate this event and make informed decisions.

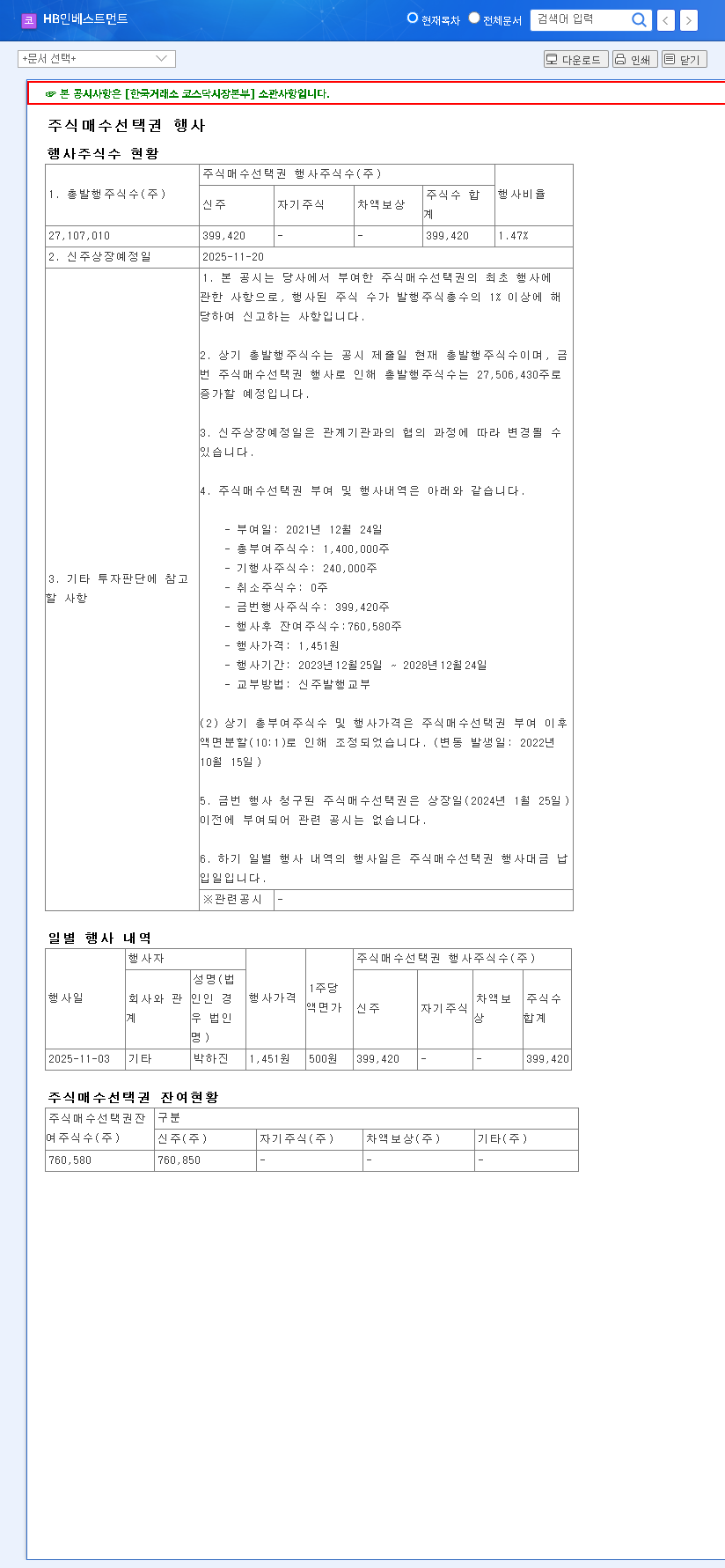

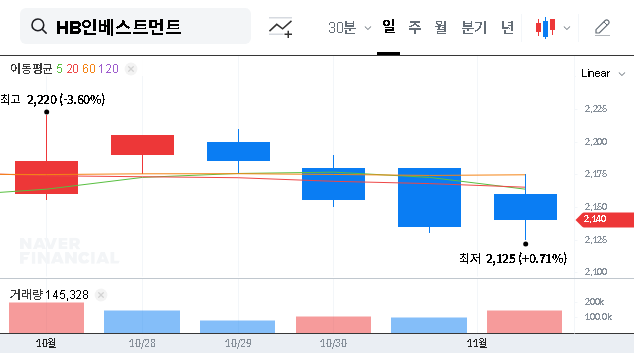

On November 3, 2025, the company disclosed the exercise of 400,000 stock options, which are set to be listed on the market on November 20, 2025. This volume represents 1.47% of the total outstanding shares. Stock options are a form of equity compensation that gives key employees the right to purchase company stock at a predetermined price, aligning their interests with those of shareholders. For official details, you can view the Official Disclosure on DART.

Analyzing HB Investment’s Core Financial Strength

Robust Fundamentals and Growth Drivers

A deep dive into HB Investment, Inc.’s 2025 semi-annual report reveals a company on a stable growth trajectory. Both operating revenue and net income have shown significant year-over-year increases. The primary engine for this growth is the equity method gains from its ‘investments in associates,’ which means the success of the companies in its venture portfolio is directly fueling its bottom line. This is a critical indicator of a well-managed VC firm.

HB Investment’s financial health is exceptionally strong, marked by a very low debt-to-equity ratio of 5.97% and a high current ratio of 1,335.95%. This demonstrates minimal reliance on debt and excellent liquidity.

A Note of Caution on Performance Fees

While the overall picture is positive, one area for investors to monitor is the proportion of ‘performance fees,’ which has decreased compared to the previous year. This could suggest potential headwinds in the investment recovery cycle or challenges in realizing gains from certain assets. Continuous monitoring of this metric is warranted to ensure the company’s profit-generating mechanisms remain robust.

The Macroeconomic Landscape for Venture Capital

No venture capital analysis is complete without considering the broader economic environment. Several key factors could create both opportunities and threats for HB Investment:

- •Interest Rate Trajectory: Anticipated interest rate cuts in the U.S. and Korea could inject more liquidity into the market, creating a favorable climate for VC investment and new fund formation.

- •Exchange Rate Volatility: A weak EUR/KRW and strong USD/KRW trend introduce currency risks that could impact the value of global investment portfolios.

- •Global Economic Signals: Fluctuating commodity prices and shipping indices could signal easing inflation but also hint at a potential economic slowdown, affecting the growth prospects of portfolio companies.

The Dual Impact: Management Confidence vs. Share Dilution

A Vote of Confidence from Leadership

The HB Investment stock option exercise can be viewed as a strong positive signal. Stock options are a key tool for motivating management and aligning their personal success with the company’s long-term performance. When executives exercise these options, it often demonstrates their confidence in the company’s future value. This act reinforces a commitment to responsible management and a shared vision for growth. To learn more, see this authoritative guide on equity compensation from a top financial resource.

Potential for Short-Term Supply Pressure

On the other hand, the introduction of 400,000 new shares to the market raises concerns about share dilution. While the 1.47% increase in total outstanding shares is relatively modest and unlikely to cause severe long-term dilution, it could create short-term supply pressure. As these new shares become available for trading on November 20, a concentrated wave of selling could place temporary downward pressure on the stock price. Prudent investors should be aware of this possibility.

Strategic Investor Takeaways & Action Plan

In conclusion, the HB Investment stock option exercise presents a nuanced picture. The company’s fundamentals are robust, and the event itself signals strong management confidence. However, short-term market dynamics must be considered. Investment decisions should be based on a holistic view that balances long-term potential with short-term risks. For a deeper understanding of this sector, consider our guide on how to evaluate VC firms.

Frequently Asked Questions (FAQ)

What does this stock option exercise mean for investors?

It signifies that key personnel are purchasing 400,000 shares, reflecting confidence in the company. However, investors should watch for potential short-term price volatility when these shares are listed on November 20, 2025.

How significant is the share dilution from this event?

The dilution is limited, as the 400,000 shares represent only 1.47% of the total outstanding shares. The long-term impact on share value is expected to be minimal compared to the company’s fundamental growth drivers.

What are HB Investment, Inc.’s primary long-term growth drivers?

The company’s primary growth driver is the value generated from its ‘investments in associates.’ The success of the companies within its portfolio translates directly into earnings for HB Investment, Inc.