A significant development is unfolding for investors in COPUS KOREA Co., Ltd., as recent disclosures signal an imminent COPUS KOREA major shareholder change. The news, stemming from a ‘Report on Status of Large Shareholdings’, has sent ripples through the investment community, raising critical questions about the company’s future leadership, strategic direction, and ultimately, its stock valuation. This comprehensive analysis will break down the official disclosure, explore the potential market ramifications, and provide a clear, actionable roadmap for investors navigating this period of uncertainty.

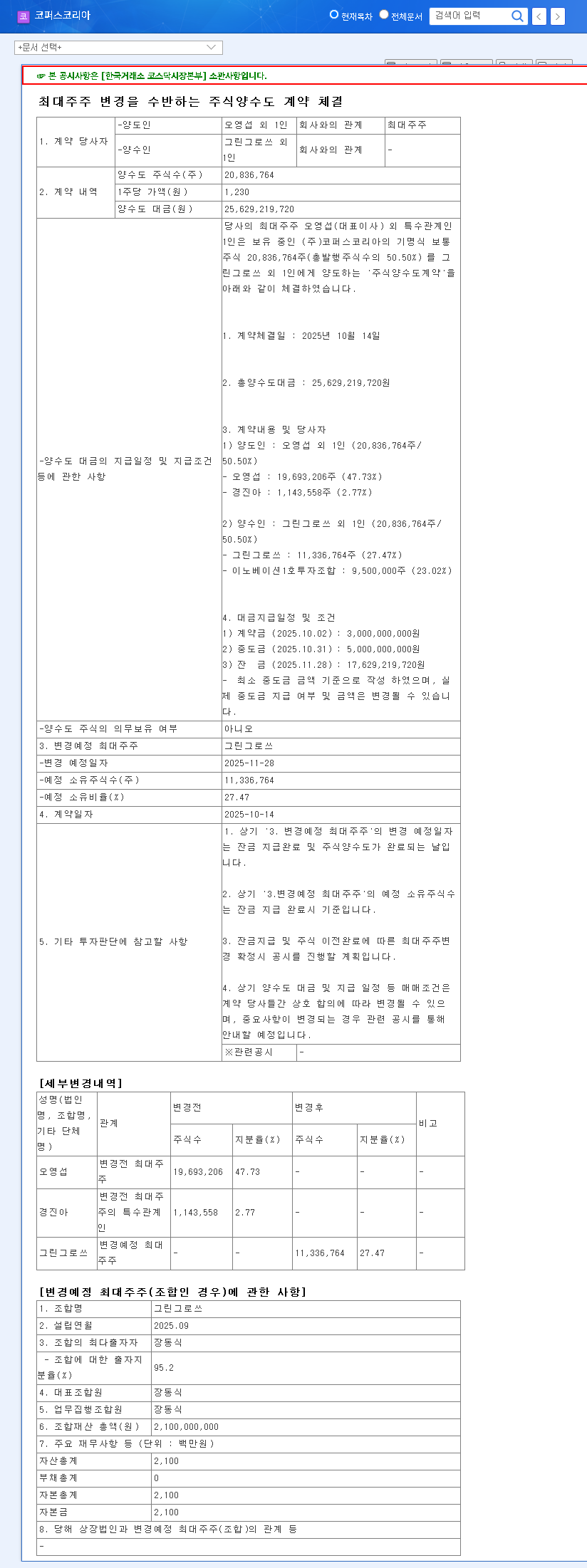

The report reveals that major shareholder Mr. Oh Young-seop has significantly reduced his stake, not as a simple stock sale, but as part of a stock transfer agreement explicitly designed to change the company’s largest shareholder. This isn’t just a portfolio adjustment; it’s a potential changing of the guard.

Deconstructing the Disclosure: What Exactly Happened?

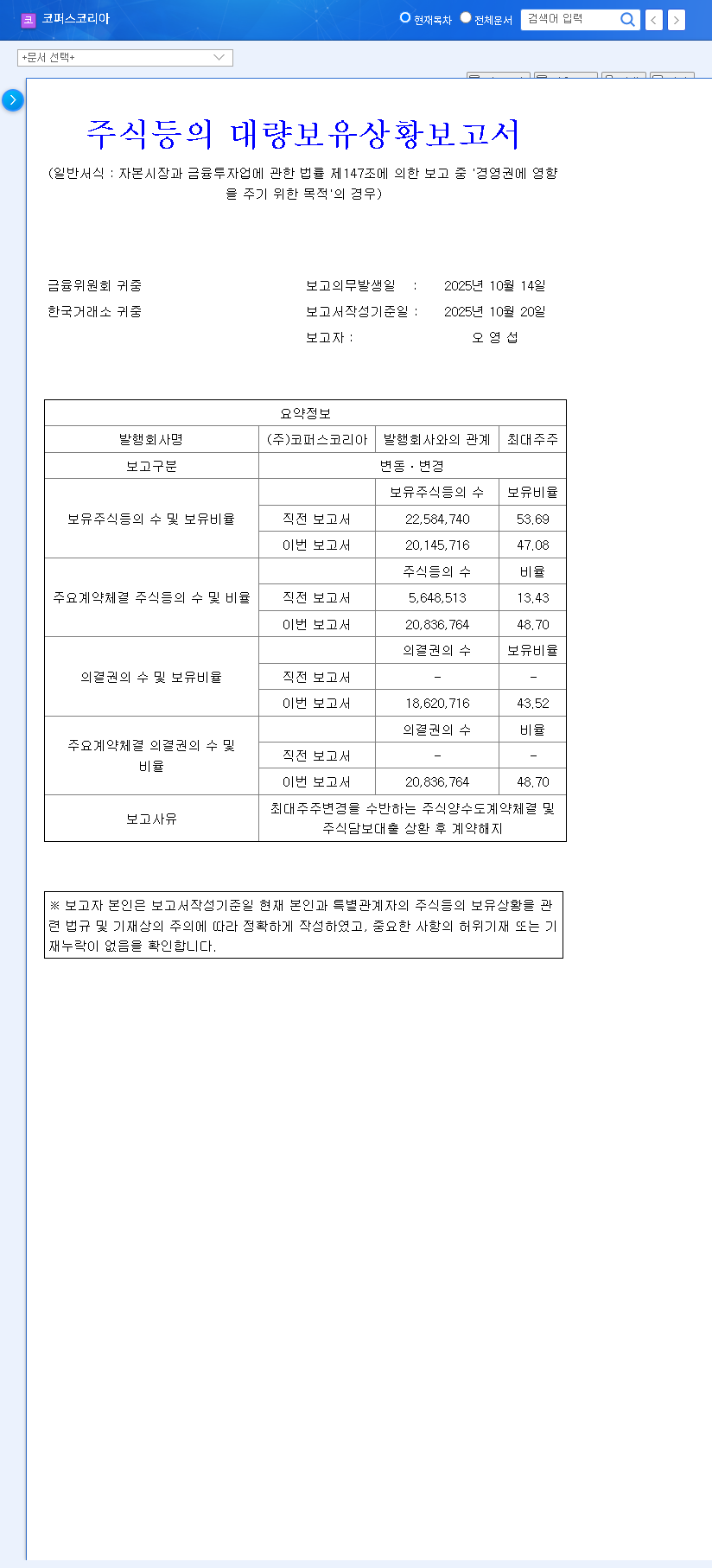

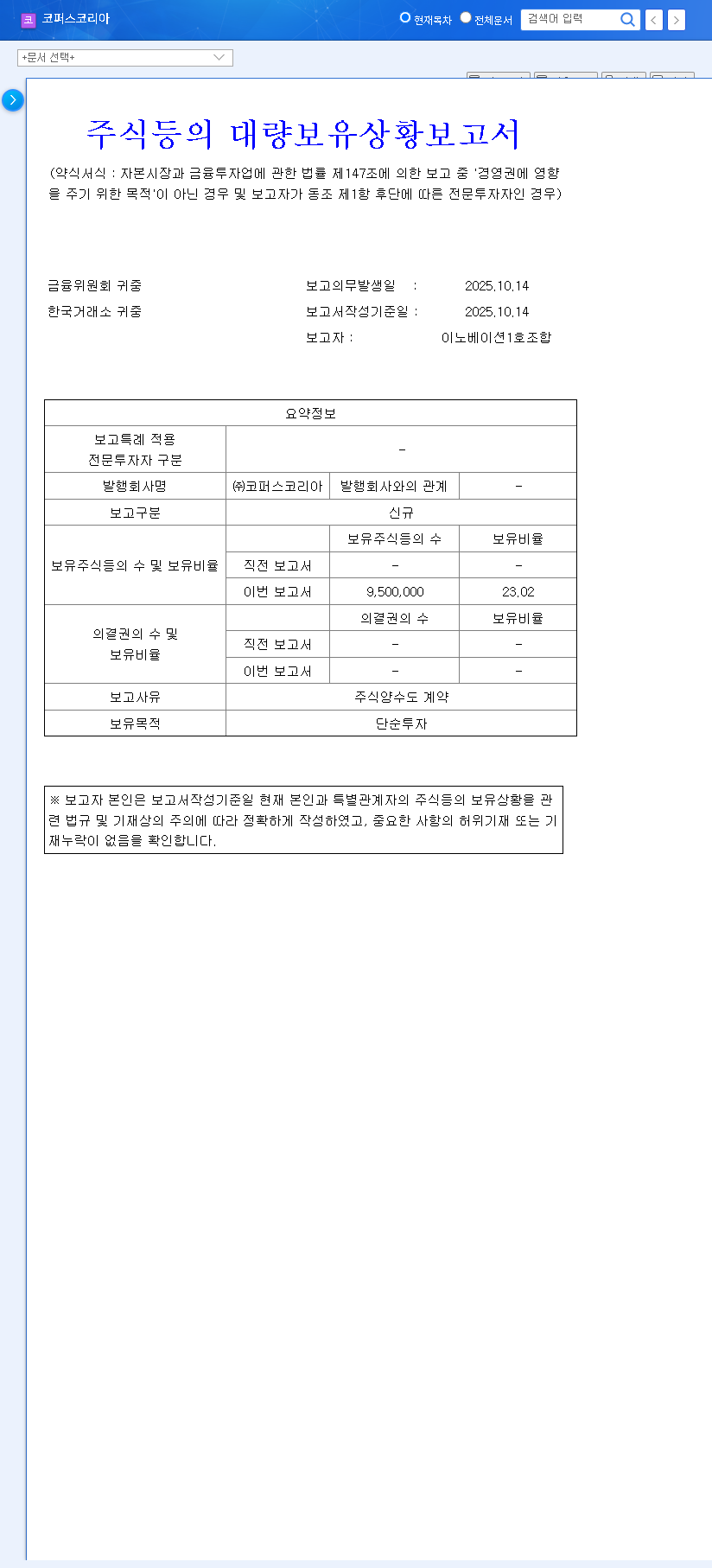

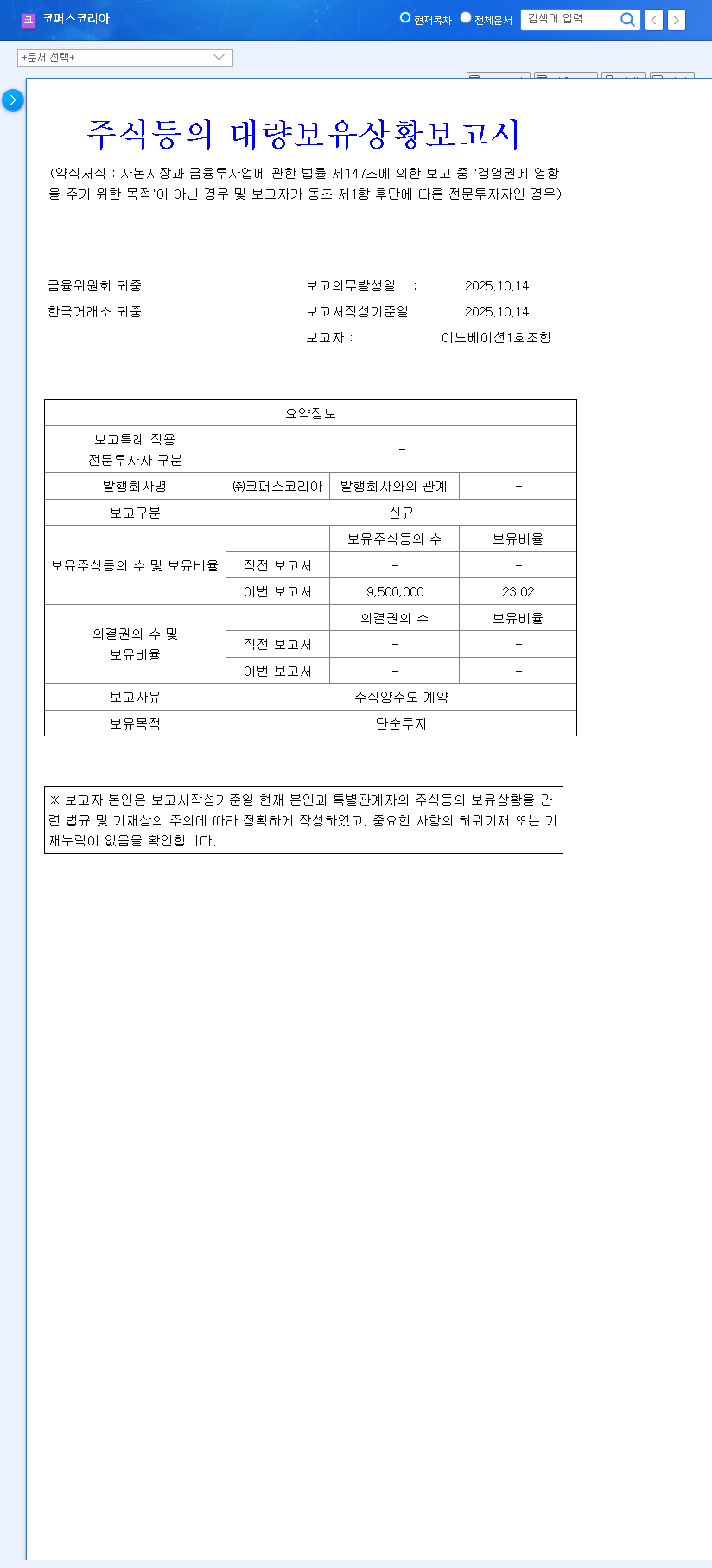

The official filing, disclosed on May 15, 2024, provides the core facts of this transaction. Understanding these details is the first step in a thorough investment analysis. You can view the original document directly from the source: Official Disclosure (DART Report).

Key Details from the Shareholding Report

- •Significant Stake Reduction: The primary shareholder, Mr. Oh Young-seop, saw his stake decrease from 53.69% to 47.08%, a substantial reduction of 6.61 percentage points.

- •Explicit Purpose: The reason cited was the ‘Execution of stock transfer agreement entailing a change in the largest shareholder.’ This language removes ambiguity and confirms a transfer of management control is intended.

- •Transaction Specifics: A total of 2,439,024 common shares were sold by Mr. Oh Young-seop in an off-market transaction, indicating a pre-arranged deal with a specific buyer rather than a sale on the open stock exchange.

The most critical phrase in the report is ‘entailing a change in the largest shareholder.’ This signals that the COPUS KOREA major shareholder change is not just a possibility, but a planned strategic event with a new controlling entity set to emerge.

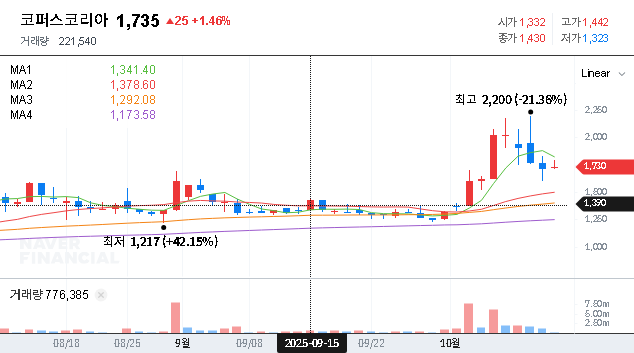

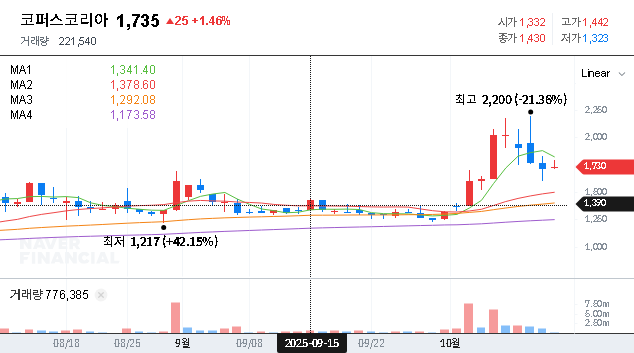

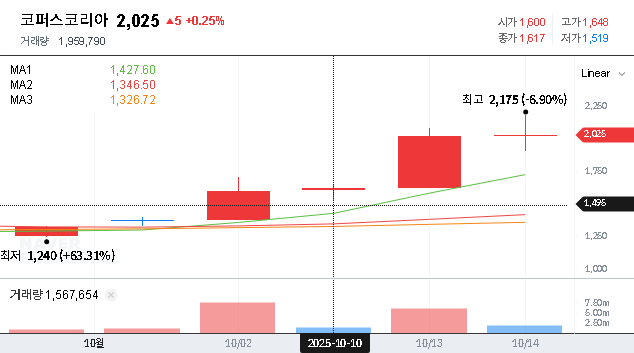

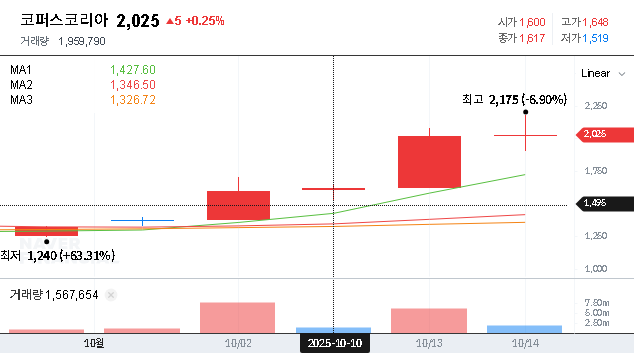

Impact Analysis: Volatility vs. Long-Term Value

Any change in control introduces both risk and opportunity. For the COPUS KOREA stock, we can anticipate distinct short-term and long-term effects.

Short-Term Market Reaction

In the immediate future, uncertainty is the dominant force. The market dislikes ambiguity, and until the new major shareholder’s identity and plans are revealed, we can expect heightened stock price volatility. Speculative trading may increase as the market attempts to price in various potential outcomes. A sale by a founding or long-term major shareholder can sometimes be perceived negatively, but the context of a strategic transfer often mitigates this.

Long-Term Corporate Revaluation

The long-term trajectory depends entirely on the new leadership. The company’s corporate value could be significantly re-evaluated based on several factors: the new owner’s strategic vision, their capacity to inject new capital or technology, and the potential for synergy with COPUS KOREA’s existing media and content businesses. This is where diligent investors can find opportunity; for more on this, see our guide to analyzing M&A deals for value.

An Investor’s Action Plan: Key Monitoring Points

With information still emerging, a patient and watchful approach is paramount. Rather than making rash decisions, investors should focus their attention on the following key areas and await further disclosures.

- •The New Shareholder’s Profile: Who is the acquirer? Are they a strategic player in the media industry or a financial investor? Analyze their track record, financial health, and past acquisitions to predict their likely strategy for COPUS KOREA.

- •Details of the Transfer Agreement: Subsequent disclosures must be scrutinized for the acquisition price, payment terms, and any attached conditions. The price paid per share will be a key indicator of how the new owner values the company.

- •Future Strategic Announcements: Pay close attention to any announcements regarding changes in the management team, revised business plans, or a new corporate vision. These will be the clearest signals of the company’s future direction.

- •Fundamental Business Performance: Amidst the ownership news, don’t lose sight of COPUS KOREA’s underlying business fundamentals. Continue to monitor revenue growth, profitability, and industry trends.

Conclusion: Finding Opportunity in Transition

The pending COPUS KOREA major shareholder change represents a pivotal moment for the company and its investors. While the current lack of complete information creates short-term risk, it also sets the stage for a potential long-term re-rating of the company’s value. The capabilities, resources, and strategy of the incoming management will be the ultimate determinants of success. For now, the best strategy is not to react, but to prepare. By conducting thorough due diligence and closely monitoring new information as it is released, investors can position themselves to make well-informed decisions as this new chapter for COPUS KOREA unfolds.