The recent announcement of the WSI Co., Ltd. convertible claim exercise has sent ripples through the investment community, leaving many shareholders and potential investors asking critical questions. This corporate action, involving the conversion of debt into equity, is a pivotal moment for the company (ticker: 299170). It presents both short-term risks, like stock dilution, and long-term opportunities, such as a strengthened financial position. This comprehensive WSI stock analysis will dissect the event, examine the company’s fundamentals, and provide a clear investment strategy to navigate the potential volatility and capitalize on future growth.

Deconstructing the Convertible Claim Exercise

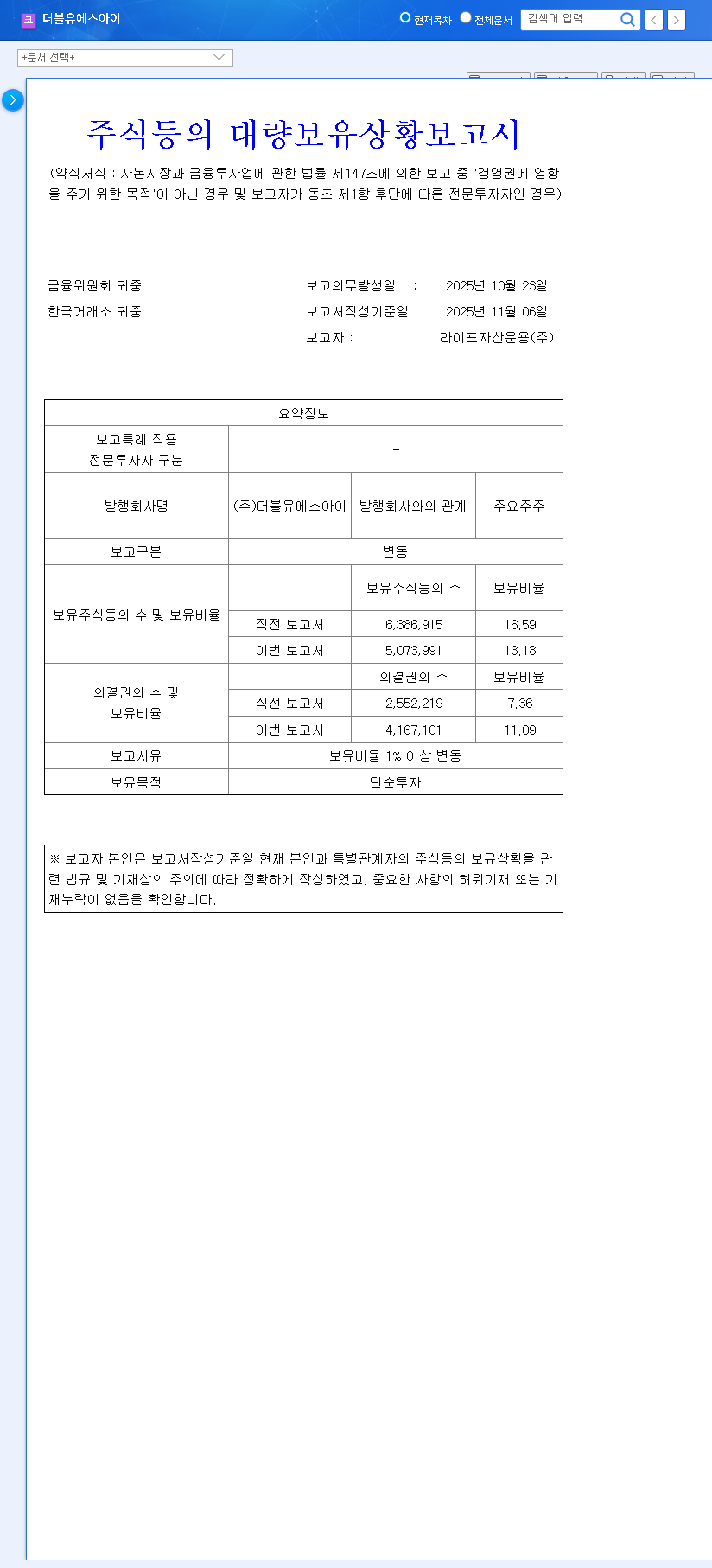

At its core, a convertible claim exercise is a mechanism where holders of convertible debt (like convertible bonds or convertible redeemable preferred shares) choose to exchange that debt for a predetermined number of common shares. On November 13, 2025, WSI Co., Ltd. officially announced this action. Understanding the specifics is the first step in a sound 299170 investment strategy.

Key Details of the Event

- •Event Date: November 13, 2025

- •New Shares Claimed: 604,593 common shares

- •Scheduled Listing Date: November 27, 2025

- •Conversion Price: 1,654 KRW per share

- •Estimated Dilution: Approximately 1.59% of total outstanding shares

This information, sourced from the company’s Official Disclosure (DART), highlights a crucial point: the conversion price is significantly lower than the recent stock price of 2,385 KRW. This creates an immediate arbitrage opportunity for bondholders, which can influence short-term market dynamics.

Fundamental Analysis of WSI Co., Ltd.

To understand the long-term convertible bonds impact, we must look beyond the single event and evaluate the underlying health of the business. WSI is a company in transition, aggressively pursuing diversification to fuel new growth.

Strengths & Opportunities

- •Strategic Diversification: The acquisition of IntroBiopharma Co., Ltd. has created a more robust, three-pronged business model spanning distribution, pharmaceuticals, and medical robots. This reduces reliance on a single revenue stream.

- •Future-Facing Ventures: Entry into high-growth markets like medical robotics (EasyMedibot Co., Ltd.) and cardiovascular devices shows a forward-thinking strategy to capture future value.

- •Profitability Signals: A recent year-over-year increase in operating profit, driven by these new businesses, suggests the diversification strategy is beginning to bear fruit.

Weaknesses & Risks

- •Financial Strain: The very convertible debt now being exercised has increased total borrowings, leading to net losses from derivative valuation adjustments and higher interest costs.

- •New Business Uncertainty: The medical robot and cardiovascular ventures are still nascent. They require significant capital and time to prove their market viability and become major revenue contributors.

- •Macroeconomic Headwinds: As explored in our guide to evaluating macroeconomic factors, high interest rates, a strong USD/KRW exchange rate, and volatile oil prices can pressure margins and dampen investor sentiment.

Stock Price Impact: Short-Term Pain, Long-Term Gain?

The WSI Co., Ltd. convertible claim exercise creates a classic conflict between short-term market mechanics and long-term corporate health.

The primary short-term concern is stock dilution. When new shares are created, the ownership stake of existing shareholders is reduced. This can lead to a temporary drop in earnings per share (EPS) and the stock price.

The Short-Term Outlook: Navigating Volatility

The introduction of 604,593 new shares, priced well below the market rate, will likely create selling pressure. Investors who converted their bonds may look to lock in quick profits by selling their newly acquired shares. This supply increase could temporarily depress the stock price around the November 27th listing date. However, sophisticated investors, like those who read market analysis from sources like Bloomberg, often anticipate such events, meaning some of this impact may already be priced in.

The Long-Term Outlook: A Healthier Company

Looking beyond the immediate market reaction, this event is a net positive for WSI’s balance sheet. By converting debt to equity, the company reduces its liabilities and interest expense. This improves its debt-to-equity ratio, making it a financially sounder entity. The capital infusion is also critical for funding the very growth engines—pharmaceuticals and medical devices—that are key to its long-term success. A successful execution of these new ventures, funded by this move, will ultimately create far more value than the ~1.59% dilution erodes.

Our Recommended WSI Investment Strategy

Given the competing factors, a nuanced 299170 investment strategy is required. A one-size-fits-all approach is ill-advised.

- •For Short-Term Traders: A cautious, wait-and-see approach is prudent. The risk of downward pressure post-listing is significant. Monitoring trading volume and price action around November 27th is key before committing capital. Impulsive buying is not recommended.

- •For Long-Term Investors: The focus should be on the execution of the business strategy. This event improves the company’s financial footing to pursue its goals. The potential for a short-term price dip could represent a buying opportunity if you believe in the long-term vision of WSI’s diversified model.

Ultimately, we recommend a ‘Conservative Wait-and-See’ stance. The potential for long-term upside is real, but the uncertainties surrounding the new ventures and the macroeconomic climate demand patience. Continuously monitor progress on the key initiatives outlined below to make an informed decision.

Frequently Asked Questions (FAQ)

What is the main short-term risk of the WSI convertible claim exercise?

The main short-term risk is stock dilution and selling pressure. The addition of over 600,000 new shares can decrease the value of existing shares and lead to a temporary price drop as new shareholders sell to realize profits.

How does this event benefit WSI Co., Ltd. in the long run?

In the long term, it improves the company’s financial health by reducing debt and interest payments. This de-risks the balance sheet and provides the necessary capital to invest in high-growth areas like their pharmaceutical and medical robot divisions, which are crucial for future value creation.

What should investors monitor moving forward?

Investors should monitor the revenue growth and profitability of IntroBiopharma, tangible market penetration of the medical robot and cardiovascular businesses, improvements in the debt-to-equity ratio in subsequent quarterly reports, and the company’s response to ongoing macroeconomic trends.

Disclaimer: This article is for informational purposes only and is based on publicly available data. It does not constitute financial advice. All investment decisions carry risk, and the ultimate responsibility lies with the individual investor.