![(192410) Onule&M CB Acquisition: A Lifeline or a Trap for Investors? [In-Depth Analysis]](https://note12345-images.s3.ap-southeast-2.amazonaws.com/wp-content/uploads/2025/09/30042610/192410.png)

The recent Onule&M CB acquisition has sent ripples through the investment community, raising a critical question: is this a signal of a potential turnaround for the beleaguered company, or simply another layer of complexity for investors to navigate? With ‘Marchellus Mezzanine Investment Union’ securing a massive 17.25% stake through convertible bonds, understanding the full picture is more crucial than ever. This in-depth Onule&M financial analysis will unpack the details of the deal, dissect the company’s precarious financial health, and provide a clear action plan for current and prospective investors.

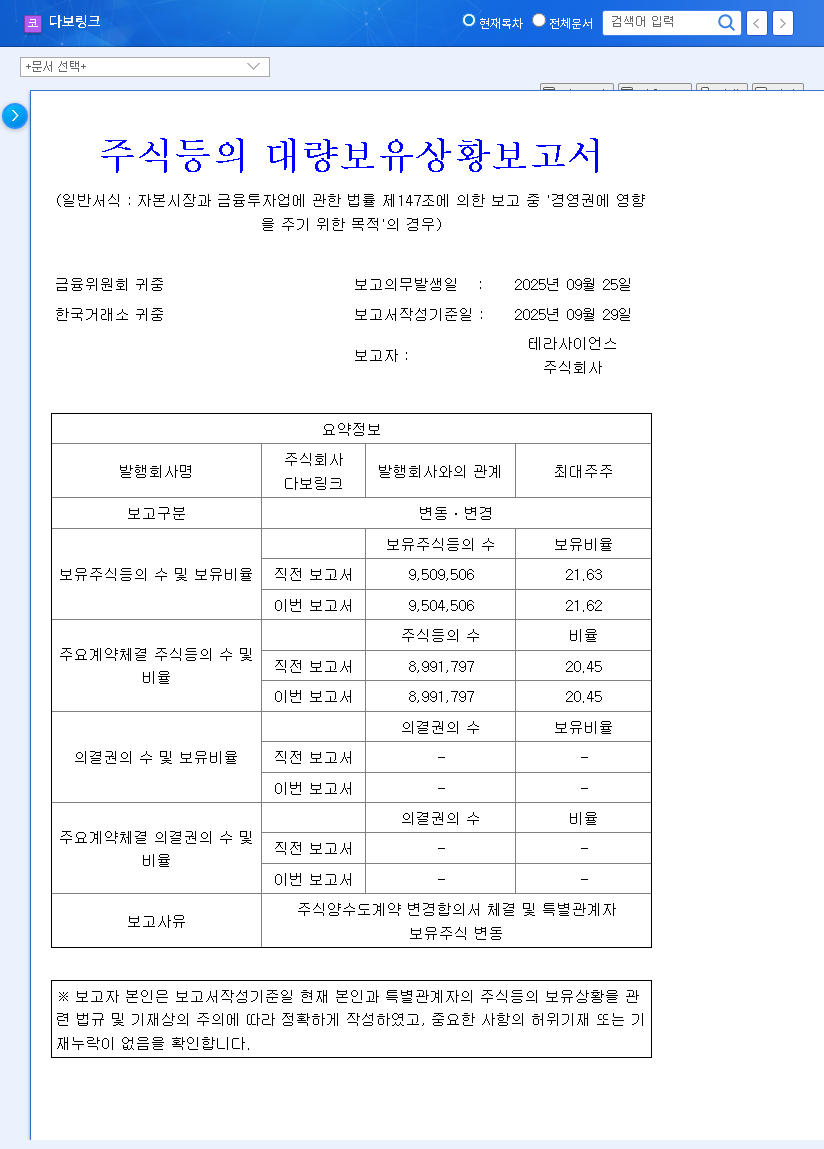

Deconstructing the Onule&M CB Acquisition

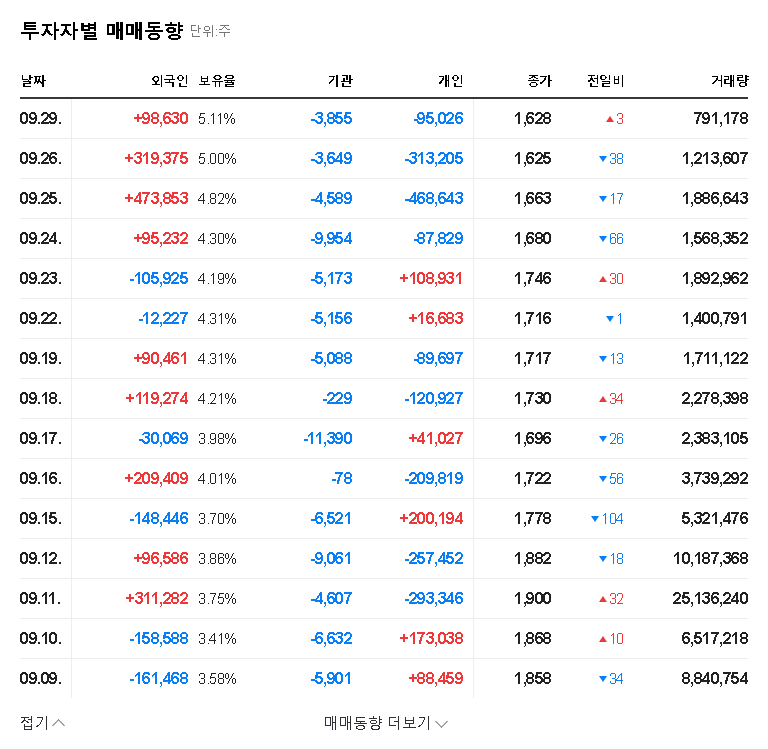

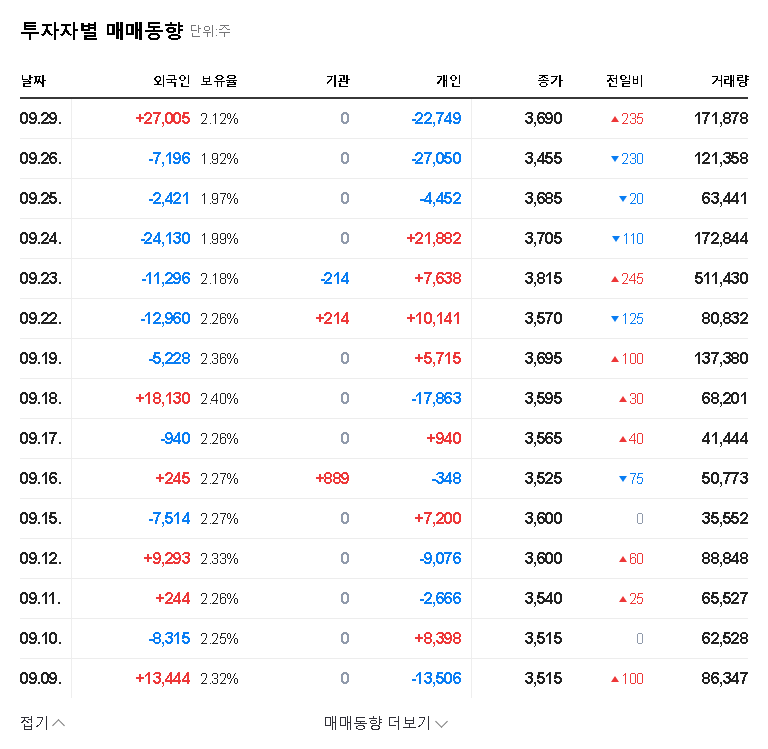

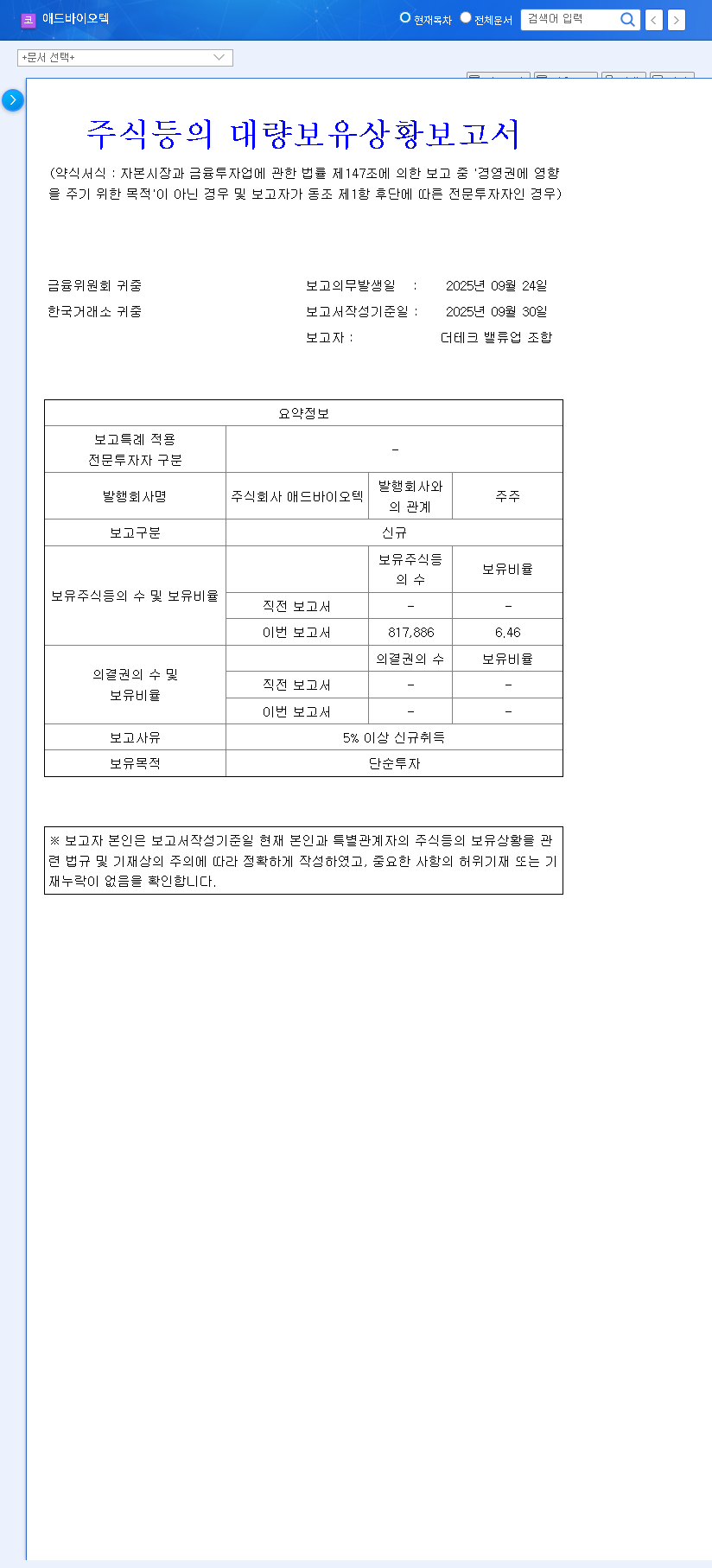

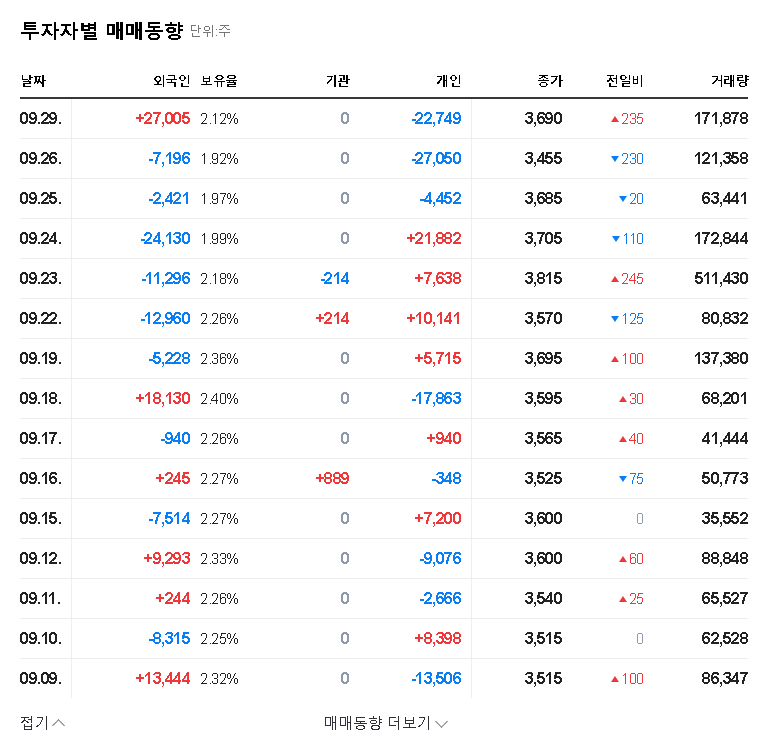

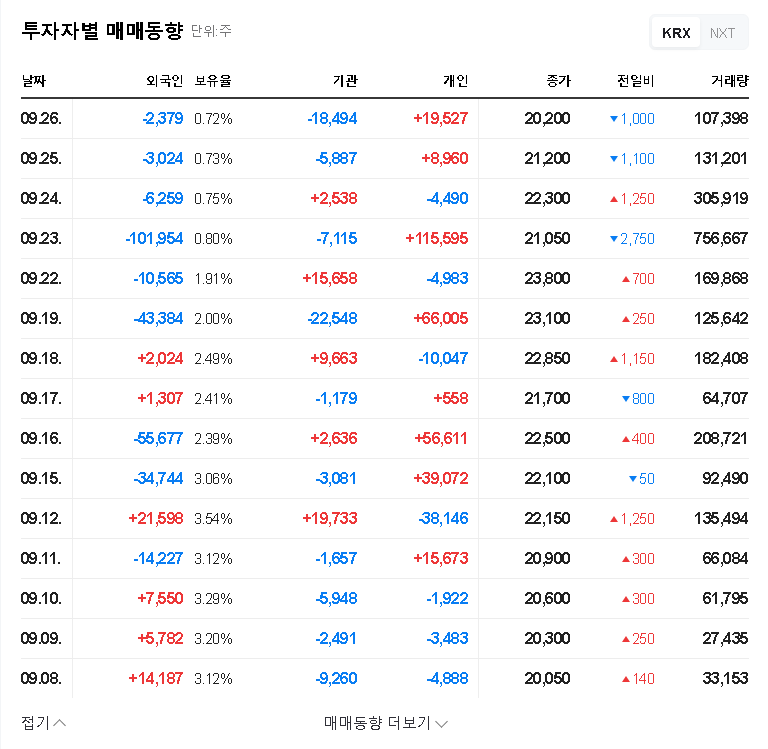

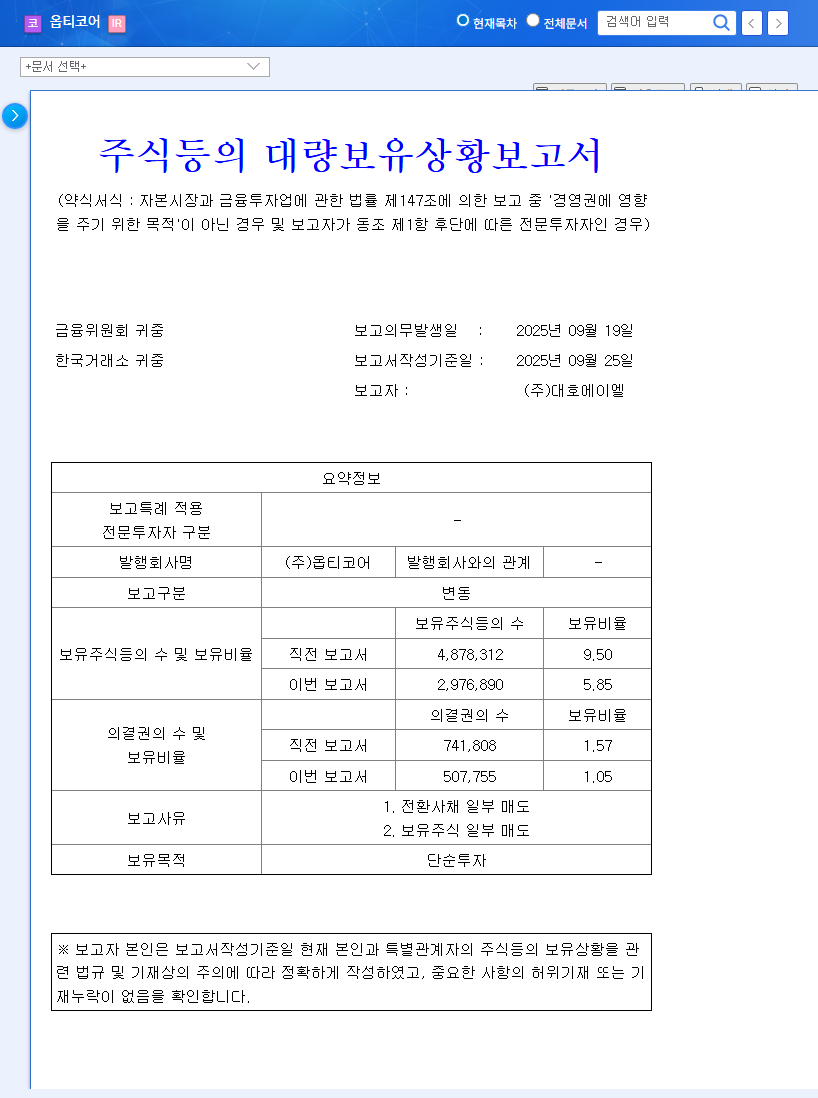

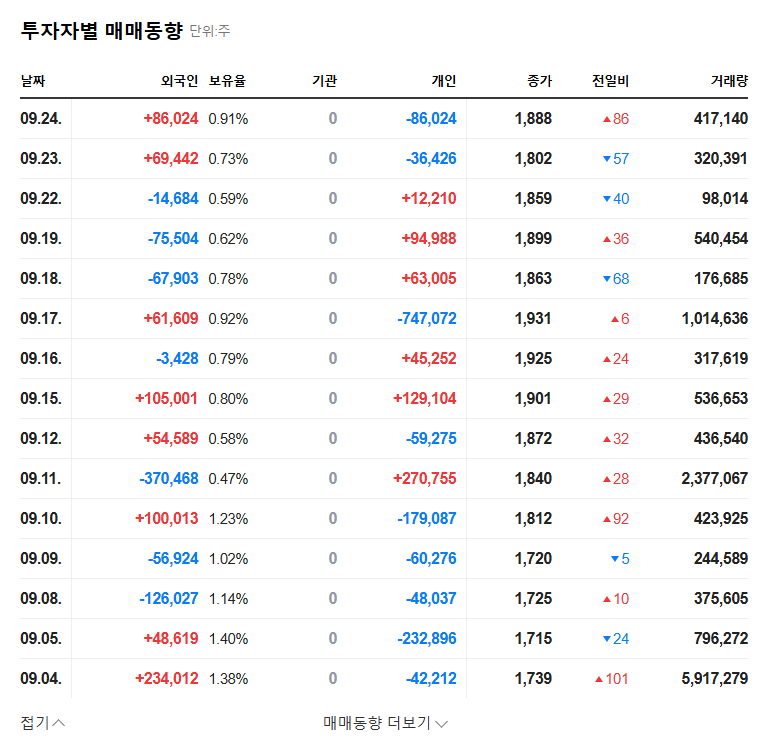

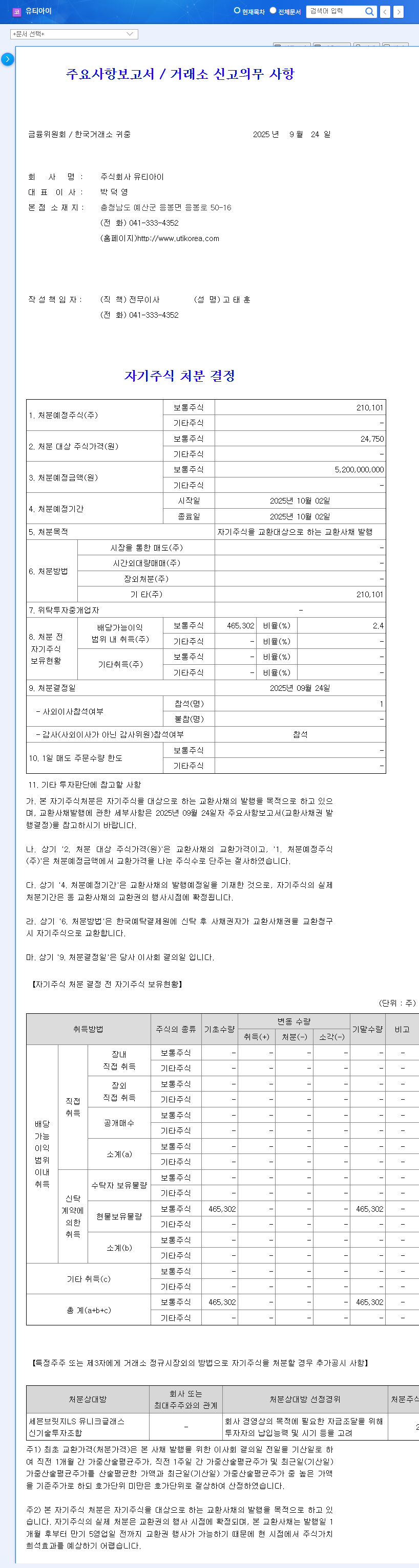

On September 30, 2025, Onule&M disclosed that ‘Marchellus Mezzanine Investment Union’ acquired 6,256,410 of its convertible bonds. According to the Official Disclosure (DART), this gives the union a potential 17.25% stake if converted to common stock. While the stated purpose is for ‘simple investment’, the sheer size of the stake suggests it could lead to significant shifts in shareholder power and corporate direction. This kind of convertible bond investment is often a double-edged sword, providing much-needed capital but also introducing major risks.

A convertible bond is a hybrid security that blends features of both debt and equity. It acts as a loan to the company, but gives the holder the option to convert the bond into a predetermined number of common shares. For a deeper understanding, you can learn about convertible bond mechanics on Investopedia.

A Company on the Brink: Onule&M’s Financial Crisis

The context for this acquisition is a company in severe distress. A comprehensive Onule&M financial analysis reveals a grim picture across all key metrics, which is why this cash infusion was necessary in the first place.

Collapsing Core Business and Deepening Losses

The foundation of Onule&M, its antenna manufacturing business, is crumbling. Revenue plummeted from 17.45 billion KRW in 2023 to just 7.19 billion KRW in the first half of 2025. This isn’t just a slowdown; it’s a catastrophic decline. Consequently, profitability has deteriorated alarmingly. The company posted an operating loss of -1.66 billion KRW and a staggering net loss of -55.07 billion KRW in H1 2025, largely inflated by tax-related provisions.

The Alarming State of the Balance Sheet

The company’s financial health is precarious at best. As of June 2025, key indicators paint a picture of a liquidity crisis:

- •Liquidity Crisis: Current liabilities have ballooned to 68.12 billion KRW, raising serious doubts about the company’s ability to meet its short-term obligations.

- •Capital Impairment: Total capital has fallen into negative territory at -20.69 billion KRW, a severe sign of financial erosion.

- •Negative Cash Flow: Operating cash flow is a massive -78.58 billion KRW, indicating the core business is burning cash at an unsustainable rate.

Investor Impact: Dilution, Debt, and Uncertainty

For existing shareholders, the primary concern of the Onule&M CB acquisition is the threat of share dilution. If Marchellus converts its bonds into common stock, it will create millions of new shares, thereby reducing the ownership percentage and potentially the value of each existing share. This overhang can place significant downward pressure on the stock price.

While some may view the large investment as a vote of confidence, it’s crucial to adopt a realistic perspective. This event does not solve Onule&M’s fundamental problems. Instead, it highlights the severity of its debt burden and introduces dilution risk. Furthermore, the company’s ambitious pivot into new ventures like AI semiconductors and data centers carries immense execution risk and capital requirements, adding yet another layer of uncertainty for anyone following this investor guide.

An Action Plan for Investors

Given the extreme financial distress, business outlook, and risks associated with the convertible bond deal, an extremely cautious investment approach is warranted. Short-term price volatility may occur, but it’s unlikely to be driven by a fundamental improvement in the company’s value. Prudent investors should keep a close watch on several key developments:

- •Financial Restructuring: Look for concrete plans for additional fundraising and tangible steps towards shoring up the balance sheet.

- •Marchellus’s Next Moves: Monitor any statements or actions from the investment union regarding their intent to convert the bonds or become actively involved in management.

- •Operational Performance: It is critical to see a stabilization or rebound in the core antenna business and any tangible, profitable results from new ventures. For more on this, see our guide on How to Analyze Turnaround Stocks.

- •Legal Risk Resolution: The outcome of the administrative lawsuit over a large tax penalty must be tracked closely.

In conclusion, investment in Onule&M should be considered extremely high-risk until the company presents a clear and viable path to fundamental recovery. It is wise to maintain a reserved stance, avoiding speculation and evaluating the company’s long-term value from a sober, data-driven perspective.

![(192410) Onule&M CB Acquisition: A Lifeline or a Trap for Investors? [In-Depth Analysis] 관련 이미지](http://note12345-images.s3.ap-southeast-2.amazonaws.com/wp-content/uploads/2025/09/30042616/192410_%EA%B3%B5%EC%8B%9C.png)

![(192410) Onule&M CB Acquisition: A Lifeline or a Trap for Investors? [In-Depth Analysis] 관련 이미지](http://note12345-images.s3.ap-southeast-2.amazonaws.com/wp-content/uploads/2025/09/30042623/192410_%ED%88%AC%EC%9E%90%EC%9E%90%EB%8F%99%ED%96%A5.png)