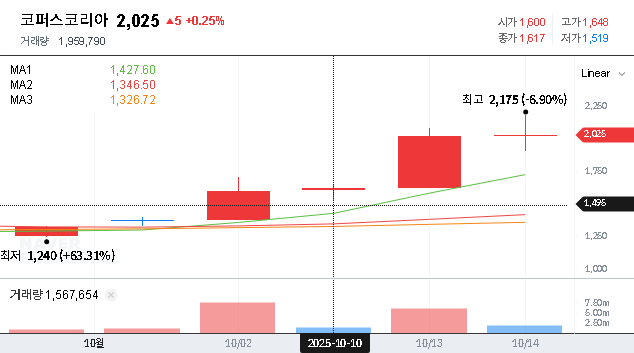

COPUS KOREA Co., Ltd. has recently become a focal point for investors following its announcement of a 10 billion KRW COPUS KOREA convertible bond issuance. This strategic financial maneuver, designed to raise crucial capital, presents a classic dilemma: Is it a lifeline signaling a future turnaround, or a red flag indicating deeper financial distress? For shareholders and potential investors, this move raises critical questions about stock dilution, financial stability, and the long-term stock outlook.

This comprehensive analysis will dissect the intricacies of the CB issuance, evaluate the company’s underlying fundamentals, and project the potential ramifications for its corporate value and stock price. We will provide a clear investment strategy to help you navigate the uncertainty and make a well-informed decision regarding COPUS KOREA stock.

Unpacking the 10 Billion KRW CB Issuance

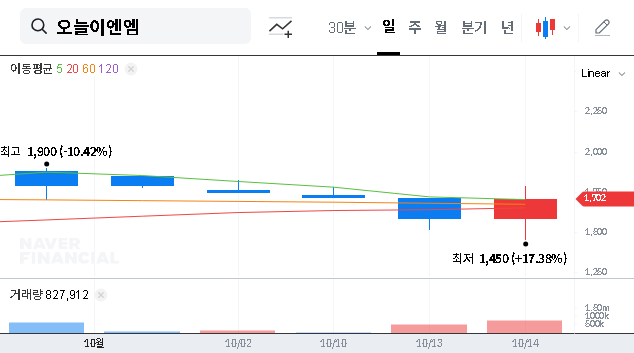

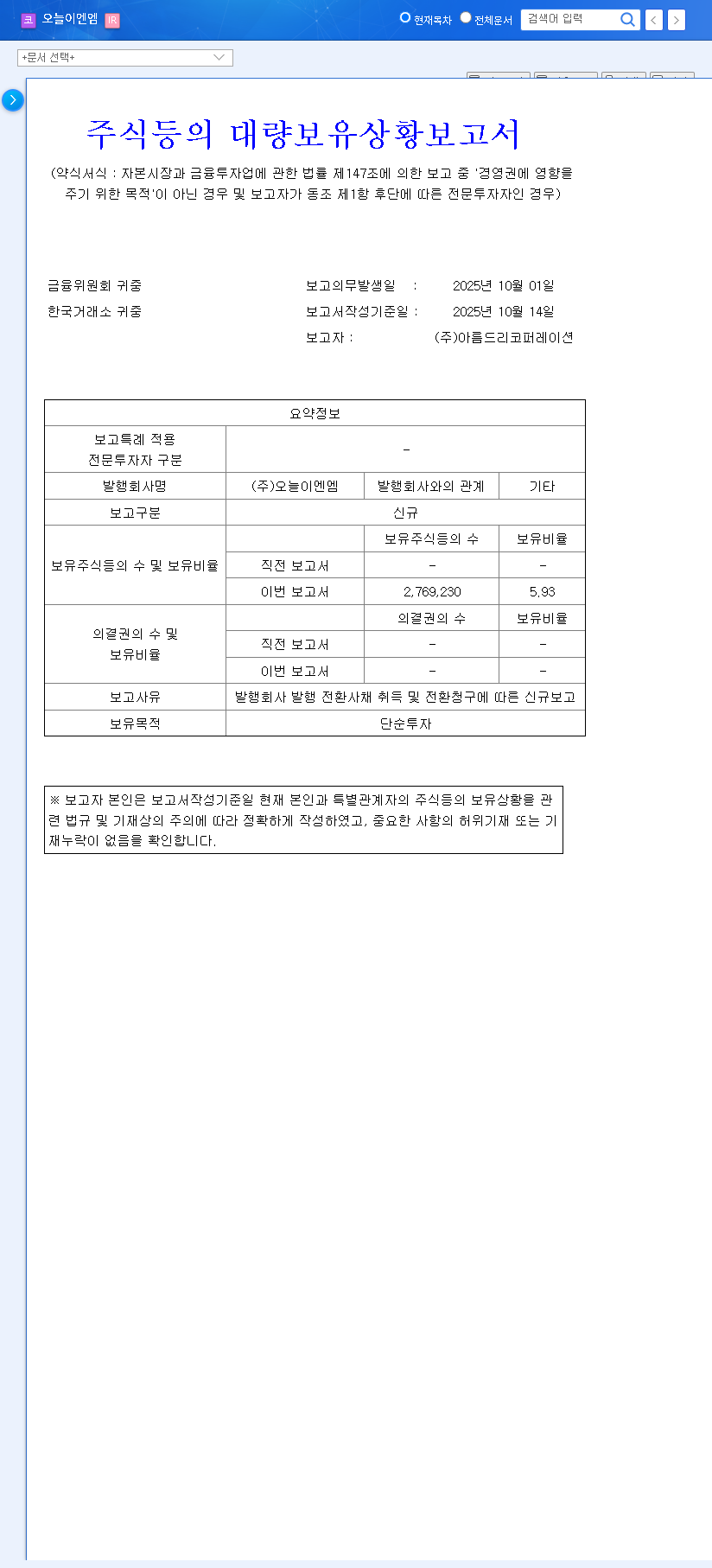

On October 15, 2025, COPUS KOREA officially announced its decision to raise 10 billion KRW through a private placement of convertible bonds. Understanding the terms is the first step in assessing the potential impact. You can view the Official Disclosure on DART for complete details.

Key Terms of the Bond:

- •Total Amount: 10 billion KRW

- •Investor: Green Innovation (via private placement)

- •Conversion Price: 1,914 KRW per share

- •Payment Date: November 13, 2025

- •Conversion Period: November 13, 2026, to October 13, 2028

This structure gives the investor, Green Innovation, the right to convert their debt into COPUS KOREA stock within the specified period. This is a common financing tool, but the reasons behind it are what truly matter.

The Financial Pressures Driving the Decision

The issuance of a COPUS KOREA convertible bond was not a decision made in a vacuum. It is a direct response to significant financial and operational headwinds facing the company. A look at their fundamentals reveals a challenging picture:

With declining revenue, widening losses, and a debt ratio soaring to 219.03%, securing fresh capital became a strategic imperative for survival and future growth.

- •Worsening Profitability: Revenue plummeted by 37.8% year-on-year to 6.48 billion KRW, largely due to the conclusion of the major drama production ‘Okssibu-in-jeon’. The company remains deep in an operating deficit of -4.18 billion KRW, compounded by valuation losses on existing financial instruments.

- •Deteriorating Financial Health: A shrinking asset base and rising liabilities have pushed the debt-to-equity ratio to a concerning 219.03%. This indicates a highly leveraged position that increases financial risk.

- •A Silver Lining: Despite the gloom, the content distribution business showed robust health, growing 23.3% to 4.84 billion KRW, thanks to a booming Japanese OTT market. This division remains a key pillar of strength. For more context, you can explore our guide on Analyzing Financial Statements for Tech Stocks.

The capital injection from this CB issuance is intended to shore up working capital, pay down debt, and invest in new growth areas, such as its nascent short-form platform.

Impact on COPUS KOREA Stock: A Double-Edged Sword

For existing shareholders, a convertible bond issuance often brings mixed feelings. It can provide the fuel for a turnaround but also comes with significant risks.

The Potential Upside (Opportunity)

- •Improved Liquidity: The immediate cash infusion provides financial breathing room, allowing the company to meet its obligations and operate more smoothly.

- •Fuel for Growth: These funds can be deployed to strengthen the high-performing content distribution arm and successfully launch new ventures, creating future revenue streams.

The Inherent Downsides (Crisis)

- •Stock Value Dilution: This is the primary concern. If and when the bonds are converted, the total number of outstanding shares will increase, potentially decreasing the value and earnings per share for existing stockholders. Learn more about how this works from authoritative sources like Investopedia.

- •Increased Debt Burden: Until conversion, these bonds are debt. They add to the company’s liabilities and interest expenses, further straining a weak balance sheet.

- •Execution Risk: There’s no guarantee the funds will be used effectively. A failure to generate a return on this new capital could leave the company in an even worse position.

Investment Strategy: A Prudent Path Forward

Given the high stakes, a cautious and diligent investment strategy is paramount for anyone considering COPUS KOREA stock. Short-term volatility and downward pressure are likely as the market digests the risk of dilution.

Actionable Checklist for Investors:

- •Adopt a Conservative Stance: The company’s fundamentals are weak. Avoid speculative buying until there are clear signs of a business turnaround.

- •Monitor Fund Utilization: Track company announcements to see precisely how the 10 billion KRW is being spent. Is it going toward high-growth projects or just covering operational shortfalls?

- •Watch Key Performance Indicators (KPIs): Pay close attention to the next few quarterly reports. Look for a recovery in the production business, sustained growth in distribution, and any improvements in the debt ratio and profit margins.

- •Understand the Bond Terms: Scrutinize the CB agreement for clauses like ‘re-pricing’, which could allow the conversion price to be lowered, increasing potential dilution.

In conclusion, while the COPUS KOREA convertible bond issuance provides a necessary financial bridge, it places the burden of proof squarely on the company’s management. Long-term value creation will depend entirely on their ability to execute a successful turnaround. For now, diligent monitoring from the sidelines is the most prudent approach.