The market is buzzing about the latest move involving DGP Co.,Ltd. stock, a small-cap company that has suddenly found itself in the spotlight. A significant disclosure has revealed that Perplexity Investment Union has acquired a substantial 18.35% stake in the company. This move has left shareholders and potential investors asking a critical question: What does this major DGP investment signify for the company’s future value and stock price?

In this comprehensive analysis, we will dissect the details of this large-scale acquisition, explore the mechanics of the Convertible Bonds (CBs) used in the deal, and provide an expert perspective on the short-term and long-term implications for DGP’s valuation. Our goal is to equip you with the insights needed to make well-informed investment decisions.

The Landmark Deal: Analyzing the Stake Acquisition

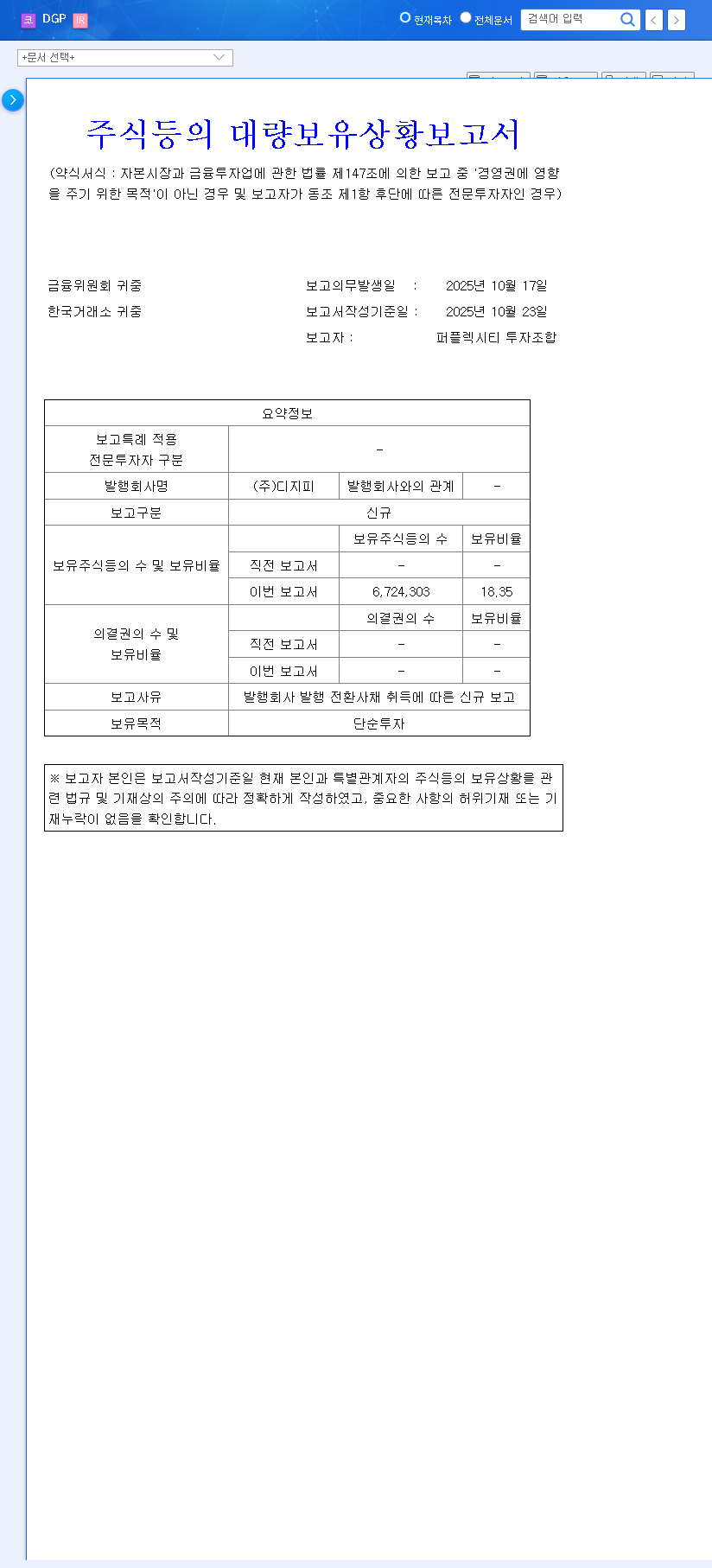

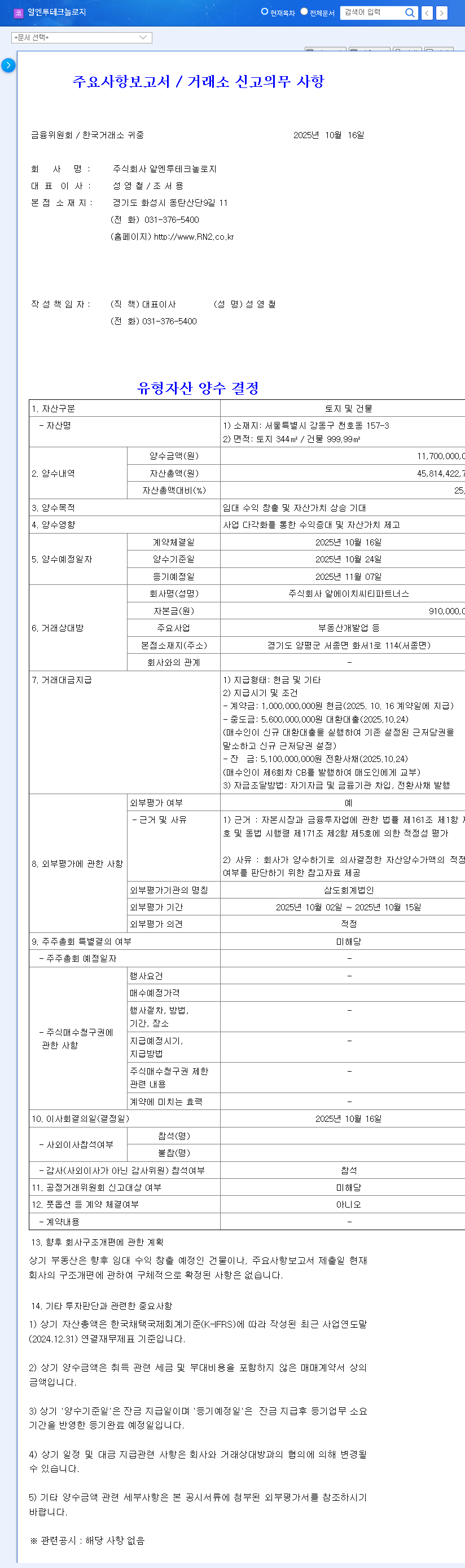

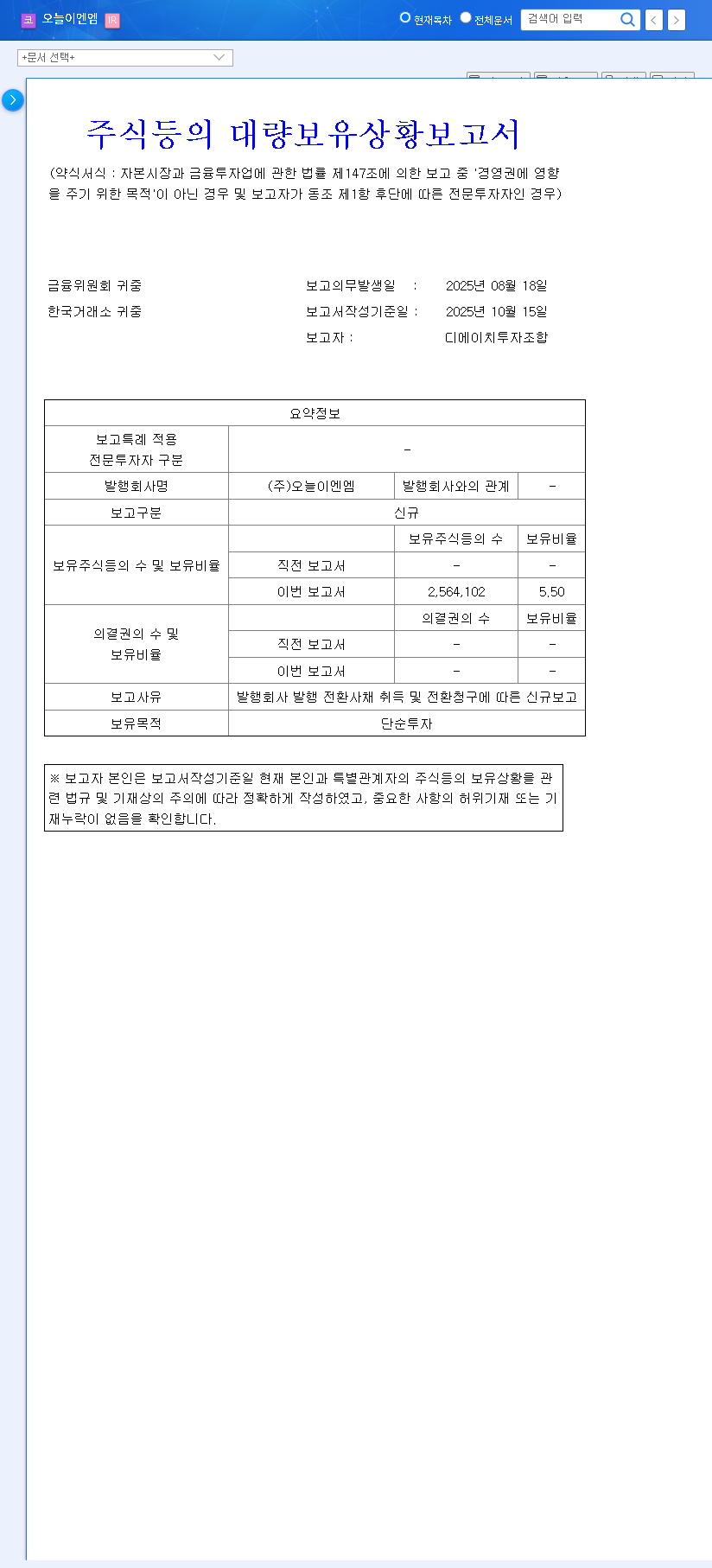

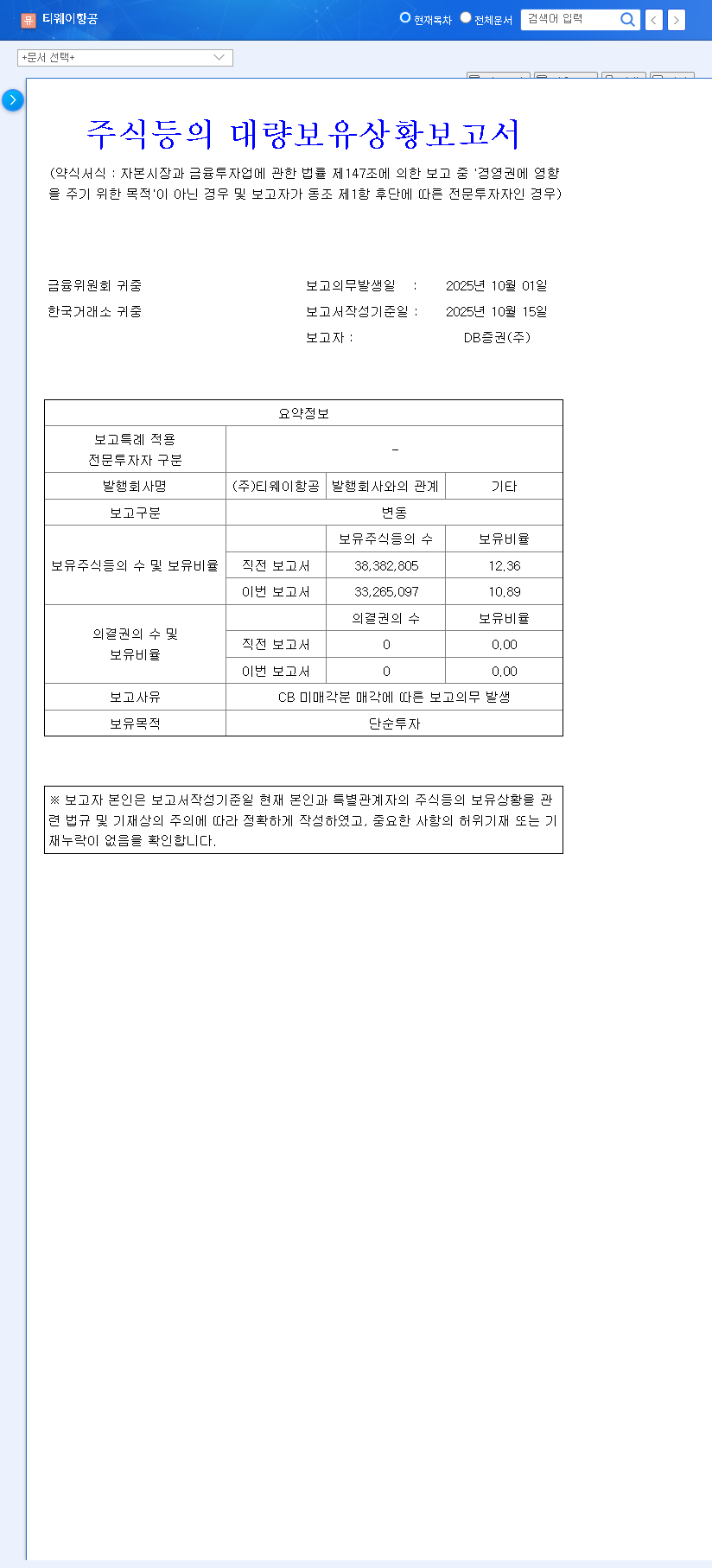

On October 23, 2025, a ‘Report on the Status of Large Shareholdings’ was filed, sending ripples through the market. The report, available via the official disclosure system (Source: DART), detailed that Perplexity Investment Union had acquired 6,724,303 shares of DGP’s 34th series Convertible Bonds (CB). This transaction effectively gives the union a new 18.35% stake in DGP Co.,Ltd., a company with a market capitalization of KRW 43 billion. While the stated purpose of the investment is ‘simple investment,’ the sheer scale of the deal suggests a deeper confidence in DGP’s potential.

What Are Convertible Bonds and Why Do They Matter?

Understanding this deal requires understanding Convertible Bonds. A CB is a hybrid financial instrument that starts as a bond (a loan to the company) but carries an option for the holder to convert it into a predetermined number of common shares at a later date. For Perplexity Investment Union, this is a strategic move. It allows them to earn interest like a traditional bondholder while retaining the upside potential of an equity investor. If the DGP Co.,Ltd. stock performs well, they can convert their bonds into shares and realize significant capital gains. This indicates they are betting not just on DGP’s ability to repay debt, but on its future growth and stock appreciation. For more detailed information, you can explore our guide to advanced investment strategies.

Projected Impact on DGP Co.,Ltd. Stock Price

Short-Term Volatility and Market Sentiment

In the short term, this news is a powerful positive signal. A large, sophisticated entity like Perplexity Investment Union taking such a significant position often attracts market attention, potentially increasing trading volume and driving up the stock price as retail investors follow the ‘smart money’. However, as a small-cap stock, DGP is inherently susceptible to volatility. The ‘simple investment’ clause may also temper expectations, as it suggests the union may not take an active role in management to drive immediate change. Uncertainty around the exact conversion terms of the CBs could also create short-term market jitters.

Long-Term Value vs. Dilution Risk

The long-term outlook is a tale of two possibilities. On one hand, this major DGP investment could trigger a fundamental re-evaluation of the company’s intrinsic value, as highlighted by authoritative financial analyses on Bloomberg. If the capital from the CB issuance is deployed effectively into high-growth projects, it could fuel substantial long-term corporate growth. On the other hand, the primary risk is share dilution. When the bonds are eventually converted into stock, the total number of outstanding shares will increase. This means that each existing share represents a smaller percentage of the company, which can put downward pressure on the earnings per share and the overall stock price if not offset by significant growth.

Given the balance of a strong vote of confidence against the technical risks of dilution and market volatility, our provisional investment opinion is a cautious ‘Watch’. A deeper investigation is non-negotiable before committing capital.

The Astute Investor’s Due Diligence Checklist

To move from ‘watching’ to a definitive investment decision, a thorough investigation is essential. Here are the critical areas you must research:

- •Analyze DGP’s Fundamentals: Go beyond the headlines. Scrutinize the company’s financial health, including revenue trends, profit margins, debt levels, and cash flow. What are its core business segments and competitive advantages?

- •Profile Perplexity Investment Union: Research the investor. What is their track record? Are they known for long-term strategic partnerships or short-term profit-taking? Understanding their typical strategy provides clues to their intentions with DGP.

- •Examine the CB Terms: The devil is in the details. Find the specifics of the 34th series CB: the conversion price, maturity date, and any mandatory conversion clauses. This will allow you to calculate the potential dilution accurately.

- •Assess Market and Industry Context: How does DGP stack up against its competitors? Is the broader industry facing headwinds or tailwinds? Context is crucial for determining if this investment is a bet on the company, the industry, or both.

Final Verdict

The acquisition of an 18.35% stake in DGP Co.,Ltd. by Perplexity Investment Union is undeniably a significant event that validates the company’s potential. It provides a strong positive catalyst and could lead to a re-evaluation of DGP Co.,Ltd. stock. However, the ‘simple investment’ purpose and the inherent risks of convertible bonds—namely, future share dilution—necessitate caution. A comprehensive due diligence process, as outlined above, is paramount before any capital is deployed. The future trajectory of DGP’s stock will ultimately depend on the company’s ability to leverage this new capital for fundamental growth.