GLOBON CO., LTD. (KOSDAQ: 019660) has entered the spotlight with a significant financial maneuver: a 4.2 billion won convertible bond issuance. This move has sparked a crucial debate among investors. Is this a strategic masterstroke to fund future growth, or a red flag signaling potential share dilution risk? This comprehensive analysis will dissect the details of the GLOBON convertible bond, evaluate its potential impact on the company’s value, and provide a clear investment framework.

Unpacking the 4.2 Billion Won Issuance

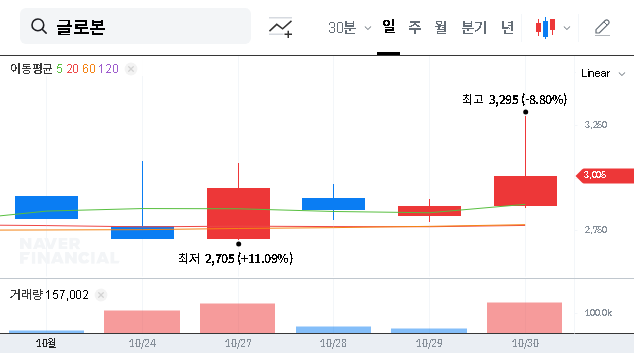

On October 30, 2025, GLOBON’s board approved the issuance of 4.2 billion won in private placement convertible bonds (CBs). Understanding the terms is the first step in a thorough GLOBON stock analysis. The key details are as follows:

- •Investors: The bonds were allocated to private investors, identified as Baitree and Jeon Hye-soo.

- •Payment Date: The capital injection is scheduled for November 7, 2025.

- •Conversion Price: The bonds can be converted into common stock at a price of 2,863 KRW per share.

- •Market Context: At the time of the announcement, GLOBON’s stock price was trading at 3,005 KRW, slightly above the conversion price.

Essentially, a convertible bond is a hybrid security that acts like a loan but gives the holder the option to convert it into a predetermined number of common shares. This financial instrument allows companies to raise capital, often at a lower interest rate than traditional loans. For a deeper understanding, you can learn more about how convertible bonds work on authoritative finance sites.

The Strategic Rationale: Fueling Growth or Patching Leaks?

GLOBON’s decision is a tale of two narratives. On one hand, it’s a proactive step to secure capital for promising new ventures. On the other, it addresses underlying weaknesses in its current business model.

The Bull Case: A Pivot to Future-Proof Industries

The primary motivation is business diversification. GLOBON is actively expanding into high-growth sectors, including fertilizer, hydrogen plants, secondary batteries, AI, and the metaverse. The 4.2 billion won raised from this GLOBON convertible bond is expected to directly fund these initiatives. This move, combined with a recent capital increase, has already improved the company’s financial health, evidenced by a significantly lowered debt-to-equity ratio of 11.53%. The growing fertilizer export business provides an early proof-of-concept for this diversification strategy.

The Bear Case: Overcoming Core Business Challenges

Investors must also consider the risks. GLOBON’s traditional flagship business, cosmetics, has seen declining sales, leading to persistent operating losses. Furthermore, the new ventures are still in their infancy with low visibility on revenue generation and potential fundraising hurdles. This capital raise, while positive, is also necessary to shore up the balance sheet and provide a runway for these new businesses to mature while the core business is restructured.

The ultimate success of this financing hinges not on the capital raised, but on the tangible returns generated from its strategic deployment into these new growth engines.

Investor Playbook: A Smart Strategy for GLOBON (019660)

Given the dual nature of this GLOBON convertible bond issuance, a prudent investment strategy requires careful monitoring. The key variable is execution. Will management allocate this new capital efficiently to generate sustainable profits?

Investors should focus on the following key performance indicators over the coming quarters:

- •New Business Milestones: Track concrete progress, partnerships, or initial revenue from the fertilizer, hydrogen, AI, and other new ventures.

- •Core Business Turnaround: Look for signs of stabilization or recovery in the cosmetics division’s sales and profitability.

- •Cash Burn Rate: Analyze how quickly the company is using its newly acquired capital against the progress being made.

- •Official Disclosures: For complete due diligence, investors should always refer to the primary source documents. You can review the Official Disclosure via the DART report.

In conclusion, the GLOBON convertible bond is a pivotal event. It provides the necessary fuel for a potentially lucrative transformation but also carries the inherent share dilution risk. The long-term impact on the stock price will be a direct reflection of management’s ability to turn this capital into tangible corporate value. For more insights on similar opportunities, you can explore our analysis of high-growth tech stocks.