Amid a challenging global economic climate, HanWool Semiconductor, Inc. has announced a significant financial maneuver: the issuance of ₩5 billion in private convertible bonds. This decision prompts a critical question for stakeholders and potential investors: is this a strategic move to secure future growth, or a necessary measure to navigate a crisis? This comprehensive HanWool Semiconductor stock analysis will dissect the details of the HanWool Semiconductor convertible bond, evaluating its short-term benefits, long-term implications, and the crucial factors investors must consider before making their next move.

The Details: A ₩5 Billion Convertible Bond Issuance

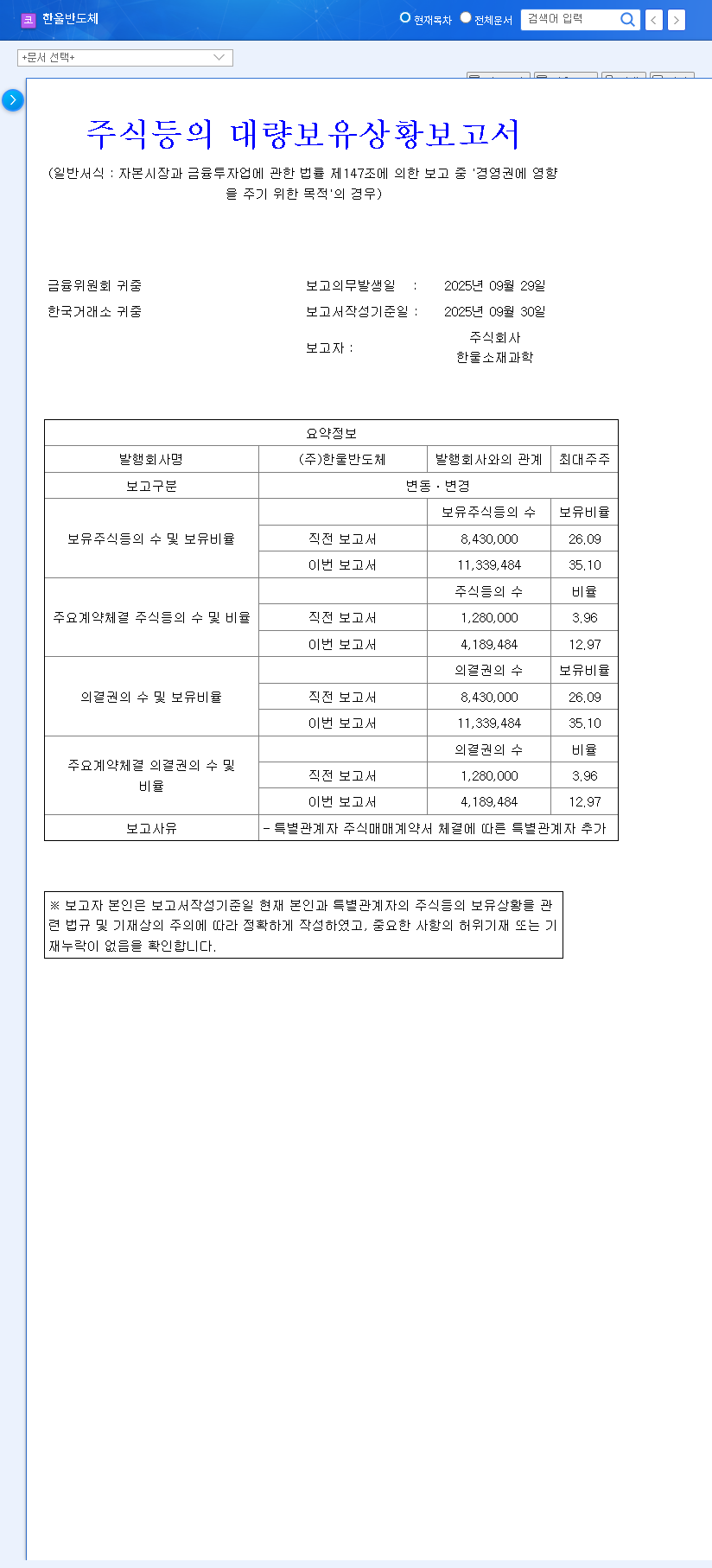

On November 13, 2025, HanWool Semiconductor officially announced its decision to issue private placement convertible bonds (CBs) valued at ₩5 billion. This sum is notable, representing approximately 7.43% of the company’s market capitalization. A convertible bond is a type of debt security that the holder can convert into a specified number of shares of common stock in the issuing company. This private placement is designated for a single entity, Global Lowell Union. The key terms are outlined in the Official Disclosure (DART) and summarized below:

- •Issuance Amount: ₩5 billion

- •Issuance Method: Private placement to Global Lowell Union

- •Conversion Price: ₩1,928 per share (below the current market price of ₩2,200)

- •Coupon/Maturity Interest Rate: 3%

- •Conversion Period: December 12, 2026 – November 12, 2028

The conversion price being set below the current stock price is a critical detail. It creates a strong incentive for the bondholder to convert the debt into equity, which signals confidence but also introduces the risk of stock dilution down the line.

The ‘Why’: Underperformance and Urgent Liquidity Needs

This HanWool Semiconductor CB issuance is not happening in a vacuum. It’s a direct response to the company’s recent financial struggles and the broader industry downturn. Performance in the first half of 2025 was sluggish, marked by declining sales and a growing operating loss. The core reasons include:

- •Front-End Market Contraction: A significant reduction in investment from the semiconductor and display industries has directly hurt sales, particularly in HanWool’s Film inspection equipment division.

- •Rising Operational Costs: An increase in selling, general, and administrative (SG&A) expenses has further squeezed profitability.

- •Uncertainty in New Ventures: While strategic pivots into AI machine vision and semiconductor IP are promising for the long term, they are in early stages and unlikely to generate revenue soon.

While the company’s debt ratio has improved, its cash reserves have dwindled. This capital injection is therefore crucial for managing operational liquidity and stabilizing the balance sheet while it navigates these challenges.

This bond issuance is a classic double-edged sword: it provides a vital short-term cash lifeline but simultaneously places immense pressure on the company to deliver on its long-term growth promises to justify the potential shareholder dilution.

An Actionable Guide for Investors

For investors, the HanWool Semiconductor convertible bond news requires a nuanced perspective. While it addresses immediate liquidity concerns, the ultimate success depends on execution. Here’s what to monitor:

Potential Upsides & Investment Points

- •New Business Success: The most significant catalyst would be tangible progress in the AI machine vision and semiconductor IP businesses. Look for milestones, partnerships, and early revenue generation.

- •Efficient Use of Capital: Track how the ₩5 billion is deployed. Investments in R&D and strategic initiatives that enhance long-term value are positive signs.

- •Industry Recovery: An upturn in the broader semiconductor market, as detailed in our previous semiconductor industry forecast, would lift HanWool’s core inspection equipment business.

Critical Risks to Consider

- •Prolonged Industry Downturn: If the macroeconomic environment worsens, the industry’s recovery could be delayed, further straining HanWool’s finances. Learn more about market dynamics from authoritative sources like McKinsey’s Global Economics Intelligence.

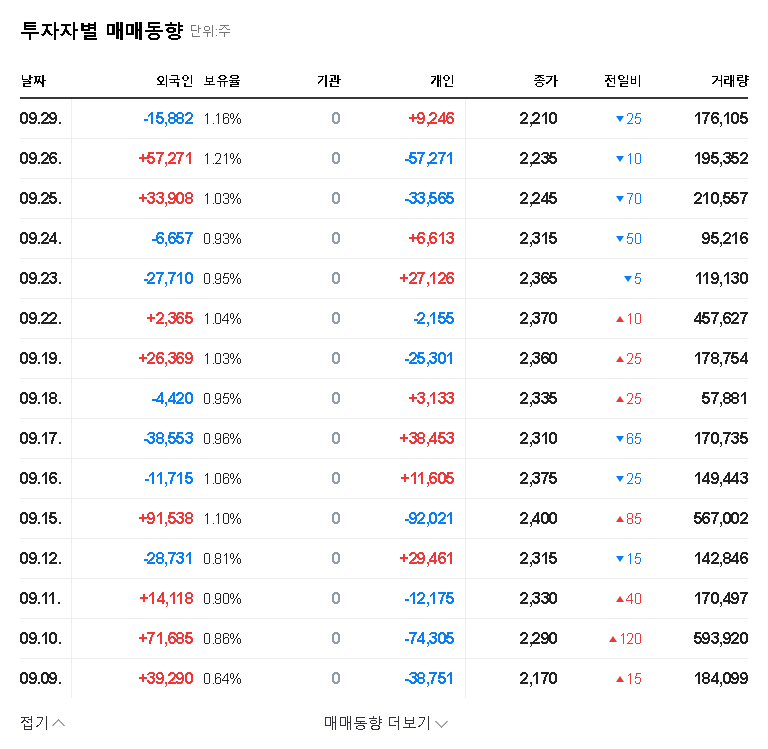

- •Stock Dilution Overhang: While not immediate, the potential conversion of bonds into nearly 2.6 million new shares creates a supply overhang that could pressure the stock price in the future.

- •Failure to Execute: If the new ventures fail to gain traction, the company will have increased its debt (via interest payments) and potentially diluted shareholders without a corresponding increase in corporate value.

Final Verdict: ‘Neutral’ with a Cautious Approach

Our investment opinion on HanWool Semiconductor, Inc. is ‘Neutral’. The CB issuance is a necessary and positive step for securing short-term operational stability. However, the company’s underlying fundamentals remain weak, and its future hinges on unproven business ventures. A positive investment case cannot be made on this fundraising alone.

A cautious approach is warranted. Investors should wait for concrete evidence of financial improvement and tangible results from the new business segments. Closely monitoring quarterly earnings reports, the specific use of the CB funds, and progress updates on the AI and IP initiatives will be essential for making an informed decision. The path forward is laden with both risk and potential reward, demanding careful and continuous due diligence.