The recent announcement of the Hyupjin Co., Ltd. convertible bond exercise has sent ripples through the investment community. This pivotal financial event, officially disclosed on November 4, 2025, presents a complex scenario for shareholders. On one hand, it signals potential stock dilution; on the other, it points towards a strengthening financial foundation. For investors, this raises a critical question: is this a short-term risk to be navigated carefully or a long-term opportunity signaling corporate confidence? This comprehensive analysis will explore the details of the convertible bond conversion, assess Hyupjin’s improving fundamentals, and provide a strategic roadmap for making informed decisions.

The Details: Understanding the Convertible Bond Conversion

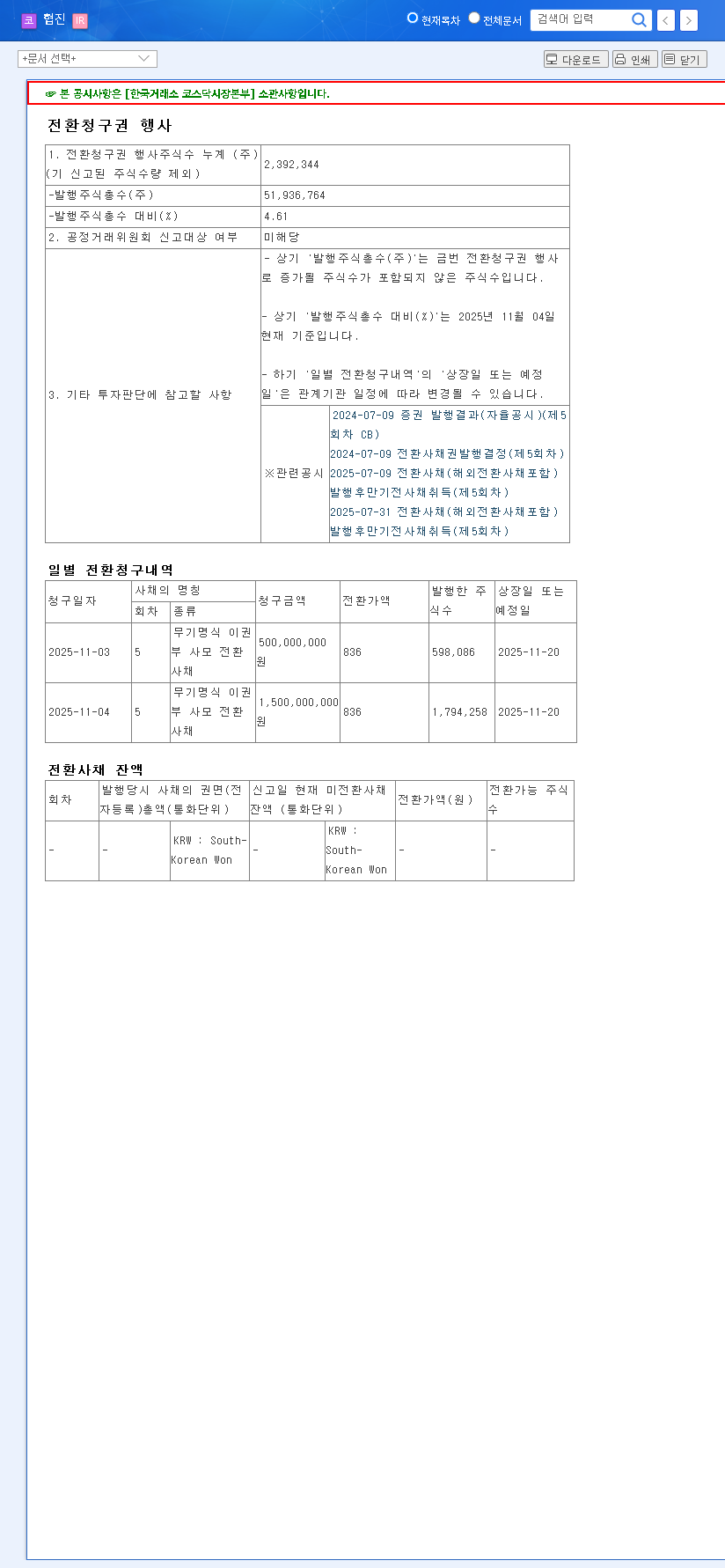

On November 4, 2025, Hyupjin Co., Ltd. formally announced a ‘Claim for Conversion Rights’. This action allows holders of the company’s convertible bonds to exchange their debt instruments for equity shares. As detailed in the Official Disclosure filed on DART, the key figures are as follows:

- •Company: Hyupjin Co., Ltd. (Market Cap: KRW 48.9 billion)

- •Shares to be Converted: 2,392,344 shares

- •Conversion Price: KRW 836 per share

- •Dilution Impact: Approx. 4.61% of total outstanding shares

- •Expected Listing Date: November 20, 2025

The conversion price of KRW 836 is notably lower than the recent stock price of KRW 941. This price difference creates a clear incentive for bondholders to exercise their rights, as it allows them to acquire stock at a discount and potentially realize immediate profits by selling on the open market. This is a primary driver behind the timing of this large-scale conversion.

Why Now? A Look at Hyupjin’s Improving Financial Health

While an event like the Hyupjin Co., Ltd. convertible bond exercise might initially spook the market due to stock dilution fears, it’s crucial to analyze it within the context of the company’s strengthening fundamentals. The December 2024 business report reveals several positive developments that paint a more optimistic picture.

Strengthened Financial Structure

Hyupjin has made significant strides in bolstering its financial stability. Through a combination of capital increases and strategic convertible bond issuance, the company has increased its cash reserves while simultaneously reducing its debt-to-equity ratio. This convertible bond conversion further reduces debt from its balance sheet, converting it into equity and signaling a healthier financial posture. For more on this topic, see our guide to analyzing corporate balance sheets.

Improved Profitability and Diversification

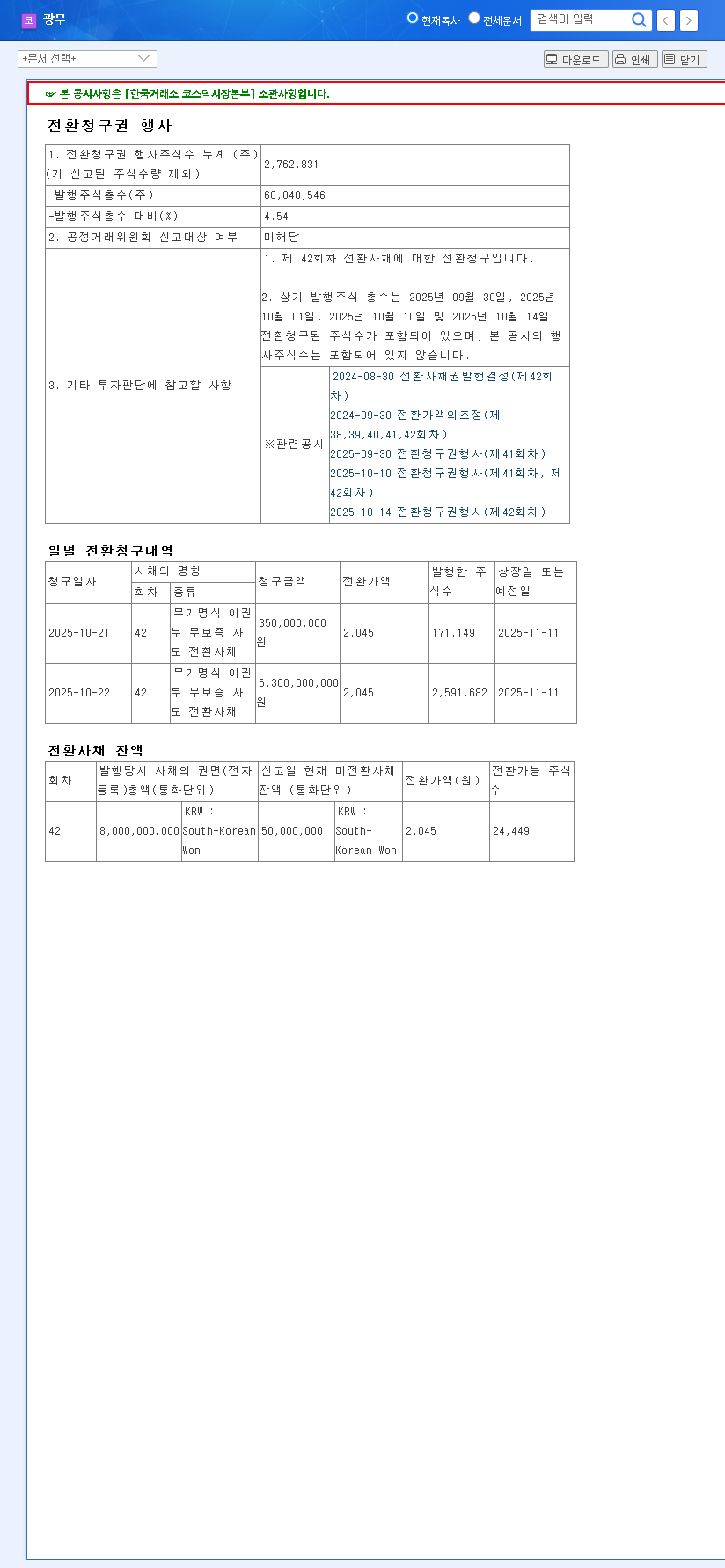

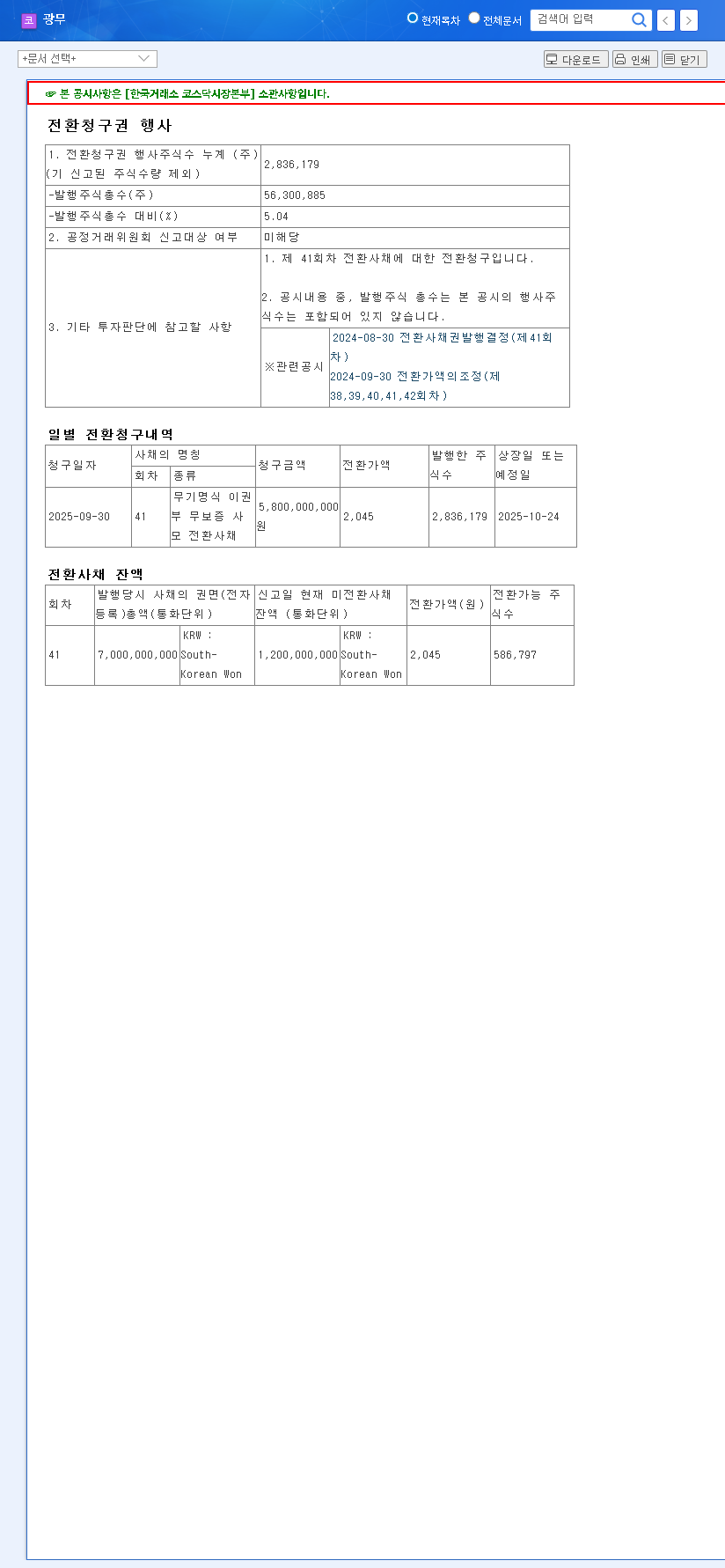

The company’s 2024 performance showed a remarkable turnaround, with a substantial revenue increase leading to a net profit. A significant portion of this success can be attributed to profitable investments in associate companies like ‘Kwangmu’. This diversification strategy is paying off, creating revenue streams beyond its core business and contributing positively to Hyupjin’s bottom line and Return on Equity (ROE).

The conversion of debt to equity is a double-edged sword: it dilutes existing shares but simultaneously de-risks the company by lowering its debt obligations, potentially paving the way for future growth investments.

Impact Analysis: Stock Price, Financials, and Operations

The immediate effect of this event will be felt across several areas of the company. Investors should anticipate both short-term pressures and long-term strategic shifts.

Short-Term Stock Price and Dilution

The listing of nearly 2.4 million new shares will cause a stock dilution of approximately 4.61%. In simple terms, the company’s net income will be spread across more shares, which can lead to a decrease in Earnings Per Share (EPS). This, combined with the potential for newly converted shareholders to sell their stock to lock in profits, could exert downward pressure on the stock price in the days following November 20, 2025.

Long-Term Financial and Business Impact

Financially, the move is a net positive for stability. Reducing debt lowers interest expenses and improves the company’s credit profile, which can reduce future borrowing costs. This improved financial flexibility can be a catalyst for growth. The capital can be channeled into R&D for its core food processing machinery business or used to expand its facility, as noted by leading industry analysts at authoritative sources like the Financial Times. Operationally, the core business remains unaffected, but a stronger balance sheet provides the fuel for strategic expansion.

A Strategic Guide for Investors

A comprehensive investor analysis must weigh the short-term dilution against the long-term benefits of enhanced financial health. While the immediate market reaction may be negative, the underlying fundamentals suggest a more resilient company is emerging. Investors should consider the following:

- •Monitor Sell-Offs: Keep an eye on trading volume around the listing date. A massive sell-off could create a buying opportunity if you believe in the long-term story.

- •Evaluate Macro-Factors: Favorable macroeconomic conditions, such as expected interest rate cuts, could improve overall market sentiment and mitigate some of the downward pressure on the stock.

- •Assess Risk Factors: It is critical to remember Hyupjin’s past. A history of administrative stock designation and auditors’ remarks on revenue recognition are risk factors that demand cautious optimism.

In conclusion, the Hyupjin Co., Ltd. convertible bond exercise is a pivotal moment. For the patient investor, looking beyond the immediate stock dilution reveals a company actively working to strengthen its financial base, which is the cornerstone of sustainable, long-term growth.