The recent announcement of the CSA COSMIC rights offering has sent ripples through the investment community. On one hand, the 10 billion KRW capital injection signals a proactive step by CSA COSMIC CO., LTD. (KRX: 083660) to mend its finances and fuel growth. On the other, it presents existing shareholders with the immediate and unwelcome reality of shareholder dilution. This creates a critical dilemma: is this a strategic pivot towards a brighter future or a desperate measure with significant downside risk? This in-depth analysis will dissect the offering, evaluate the company’s fundamentals, and provide a strategic roadmap for investors.

Unpacking the CSA COSMIC Rights Offering

On November 10, 2025, CSA COSMIC CO., LTD. formally announced its plan for a rights offering to raise 10 billion KRW. This move involves issuing new shares to specific investors at a predetermined price, a common method for companies to raise capital without taking on new debt. However, the specifics of this deal are crucial for a complete stock analysis. Here are the key details:

- •Shares to be Issued: 1,436,781 new common shares.

- •Issuance Price: 696 KRW per share, a significant discount to recent trading prices.

- •Total Capital Raised: 10 billion KRW.

- •Key Investors: KB&N Holdings and Nian.

- •Important Dates: Payment on November 18, 2025; New shares listed on December 3, 2025.

For complete, verified details, investors should review the Official Disclosure (DART Report).

The Rationale: Why is CSA COSMIC Raising Capital?

A company doesn’t undertake such a significant financial maneuver without compelling reasons. The decision for a rights offering stems from a combination of financial distress, strategic necessity, and a history of restructuring efforts.

Deteriorating Financial Health

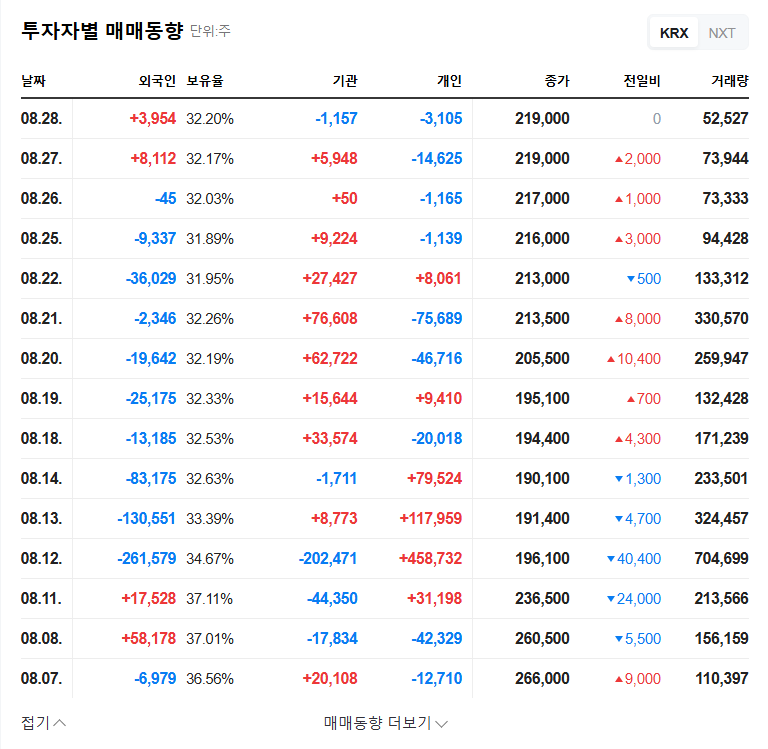

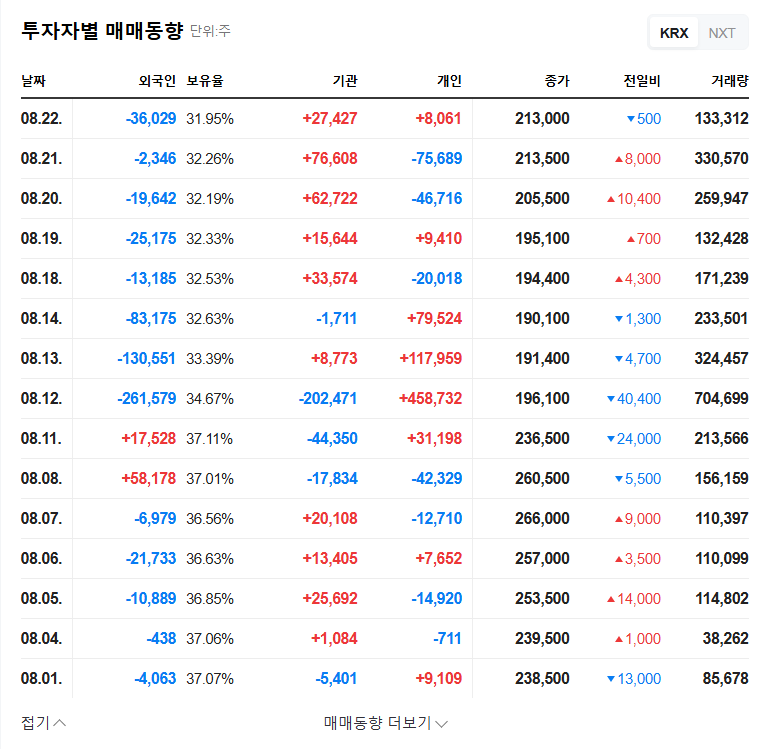

The company’s H1 2025 financial report painted a grim picture. Declining revenue combined with mounting operating and net losses revealed deep-seated issues. The primary culprit was a sharp downturn in its core cosmetics business, which its more stable construction materials segment could not offset. This performance indicates an urgent need for liquidity to stabilize operations and fund a potential turnaround.

The most significant risk is the immediate shareholder dilution. By issuing new shares at a price far below market value, the ownership stake and per-share value for every existing investor is automatically reduced.

A Pattern of Restructuring and Management Instability

This is not the company’s first attempt to right the ship. An 8 billion KRW convertible bond was issued in June 2025, also aimed at securing capital. However, the deeply discounted prices of both the bonds and this rights offering suggest that raising funds has been challenging. Compounding these financial concerns is a history of frequent management changes. A new major shareholder is expected through this rights offering, adding another layer of uncertainty about strategic consistency and long-term vision.

A Strategic Action Plan for Investors

Given the complexities of the CSA COSMIC rights offering, a prudent investment approach is essential. Investors must weigh the potential for a turnaround against the significant, tangible risks. For more on this topic, you can read our guide on how to evaluate a rights offering.

The Bull Case: A Path to Recovery?

Optimists might see this capital injection as the catalyst needed for a new beginning. Potential positive outcomes include:

- •Improved Financials: The 10 billion KRW will immediately strengthen the balance sheet, providing runway to execute a new strategy.

- •Investment in Growth: Funds can be used for R&D, new brand launches, or marketing to revive the struggling cosmetics division.

- •New Management Vision: A change in leadership could bring fresh ideas and a more effective business plan.

The Bear Case: Navigating the Significant Risks

Conversely, the risks are substantial and cannot be ignored. The primary concerns are:

- •Guaranteed Dilution: Existing shareholders will see their ownership percentage decrease. Learn more about shareholder dilution from Investopedia.

- •Execution Risk: There is no guarantee that the new capital will be used effectively or that past performance issues will be resolved.

- •Market Headwinds: Intense competition in cosmetics and macroeconomic pressures could hinder any recovery efforts.

- •Stock Volatility: The low issuance price is likely to cause significant short-term price fluctuations.

Frequently Asked Questions (FAQ)

Q1: What exactly is the CSA COSMIC rights offering?

It is a corporate action where CSA COSMIC CO., LTD. is issuing 1.44 million new shares at 696 KRW each to raise 10 billion KRW. This capital is intended to improve its financial stability and provide funds for future business investments.

Q2: How does this rights offering impact existing CSA COSMIC shareholders?

The primary impact is shareholder dilution, as the issuance of new shares at a low price reduces the value and ownership percentage of existing shares. Shareholders should also expect increased stock price volatility in the short term.

Q3: What should investors monitor going forward?

Investors should closely monitor how the 10 billion KRW is utilized, the strategic vision of the new management team, and whether there are tangible improvements in quarterly earnings reports, especially in the cosmetics division.