The unfolding Sangji Construction financial crisis has sent shockwaves through the investment community. A recent disclosure revealing a decrease in a major shareholder’s stake is not merely a routine filing; it’s a critical signal pointing to a company grappling with severe operational and financial distress. With revenues in freefall, staggering losses, and a precarious balance sheet, investors are left wondering if this is a temporary downturn or the beginning of the end. This comprehensive investor analysis for Sangji Construction will dissect the company’s current predicament, evaluate the implications of the shareholder movements, and provide a clear action plan for navigating this high-risk environment.

The Catalyst: A Major Shareholder Stake Decrease

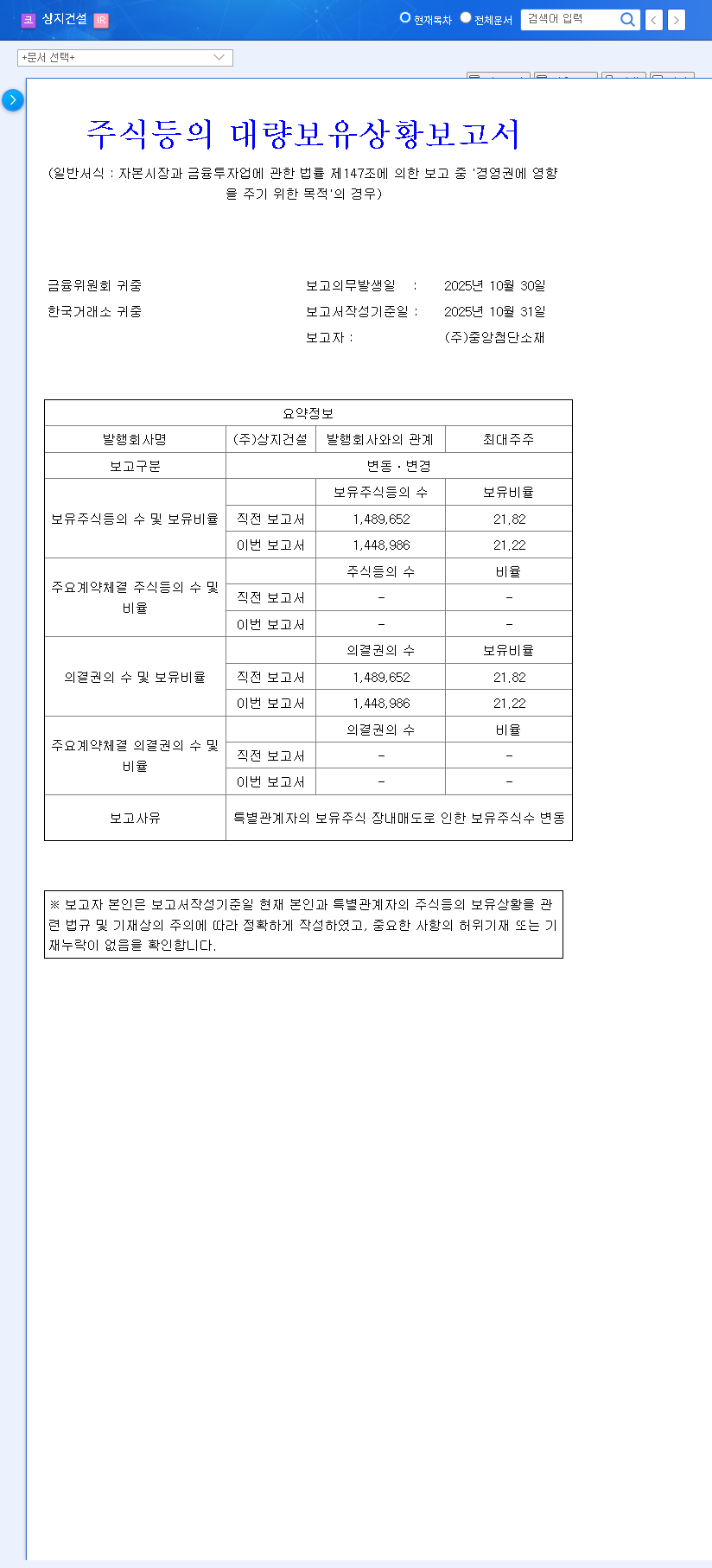

On October 31, 2025, Sangji Construction, Inc. (Market Cap: KRW 53 billion) filed a significant equity change report. The disclosure, officially available on DART (Official Disclosure), revealed that the primary reporting party, Joongang Advanced Materials/Republic of Korea, reduced its stake from 21.82% to 21.22%. This 0.60 percentage point reduction resulted from open market sales by related parties. While the stated purpose remains ‘exercising management influence,’ the sale itself, occurring amidst a deep crisis, speaks volumes. It suggests a potential erosion of confidence from those with the most intimate knowledge of the company’s operations, a major red flag for the Sangji Construction stock.

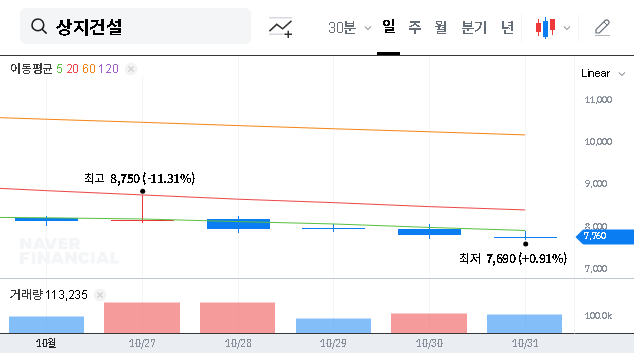

When insiders sell shares during a period of extreme financial duress, it often signals a belief that a near-term recovery is unlikely. This action can significantly amplify negative market sentiment and increase downward pressure on the stock price.

Anatomy of the Sangji Construction Financial Crisis

The shareholder sale is a symptom of a much deeper disease. An analysis of Sangji Construction’s Q1 2025 semi-annual report paints a grim picture of a company whose fundamentals are collapsing. Understanding these core issues is critical for any potential investor.

Plummeting Revenue and Deepening Losses

The company’s top-line performance is alarming. Consolidated revenue for the first half of 2025 was a mere KRW 4.942 billion, a staggering 75% decrease from KRW 20.428 billion in the same period last year. This has led to a consolidated operating loss of KRW 4.762 billion and a net loss of KRW 2.305 billion. Most concerning is the construction for sale revenue, which went from KRW 3.456 billion to a negative KRW 345 million, indicating severe project struggles and potential reversals.

Crushing Debt and Negative Cash Flow

Financial health is deteriorating rapidly. Total liabilities stand at KRW 103.691 billion, with a liabilities-to-equity ratio of 93.70%. While this is a slight improvement, it remains a heavy burden. The most shocking figure is the operating cash flow, which recorded a negative -KRW 1.026 trillion. This indicates the company is burning through cash at an unsustainable rate, unable to generate funds from its core business operations. For a deeper understanding of these metrics, you can review our guide on analyzing a company’s financial statements.

External Pressures and Operational Risks

The crisis isn’t entirely self-inflicted. Sangji Construction faces significant headwinds from the broader market, as reported by authoritative sources like Bloomberg. These include:

- •Market Slowdown: A downturn in the construction and real estate sectors, coupled with rising interest rates, has stifled demand and project viability.

- •Rising Costs: Inflation in raw material costs for essentials like cement, rebar, and concrete is squeezing already thin profit margins.

- •Project Uncertainty: Many of the company’s secured projects are conditional, facing delays in project financing (PF) reviews, which creates significant uncertainty about future revenue streams.

Previous attempts at financial restructuring, including capital increases and a name change from ‘Kailoom Co., Ltd.’ in 2024, have clearly been insufficient to address these deep-rooted fundamental problems.

Investor Action Plan: Is the Sangji Construction Stock a Buy?

Given the severe Sangji Construction financial crisis, compounded by negative insider signals and a hostile market environment, an extremely cautious and defensive investment approach is warranted. Investing now would be highly speculative and carry substantial risk.

- •Recommendation: Postpone & Observe. This is a high-risk period. Aggressive investment is ill-advised. It is prudent to remain on the sidelines and monitor for signs of a genuine, sustainable turnaround.

- •Monitor Key Developments: Keep a close watch on future shareholder filings, any announcements of concrete business restructuring or new financing, and the overall health of the real estate market.

- •Beware of Volatility: While shake-ups in management control can sometimes create short-term trading opportunities, the overwhelming weight of financial and operational risk is more likely to suppress the stock price than create a buying opportunity.

In conclusion, the long-term viability of Sangji Construction hinges on a radical overhaul of its business model and a significant improvement in its financial health. Until there is clear, undeniable evidence of such a turnaround, investors are best served by exercising extreme caution and seeking opportunities elsewhere.