A recent HYBE shareholding change disclosure has caught the attention of the market, raising questions among investors about the future of the K-POP entertainment powerhouse. On October 2, 2025, a report detailed a minor adjustment in Chairman Bang Si-hyuk’s stake in HYBE (352820). While the shift was minuscule, any change in a founder’s holdings warrants a closer look. Is this a routine corporate maneuver, or does it signal a deeper strategic shift? This in-depth analysis will dissect the official disclosure, evaluate HYBE’s robust fundamentals, and provide a clear outlook on what this event means for the HYBE stock price and long-term investors.

Decoding the HYBE Shareholding Change: What Actually Happened?

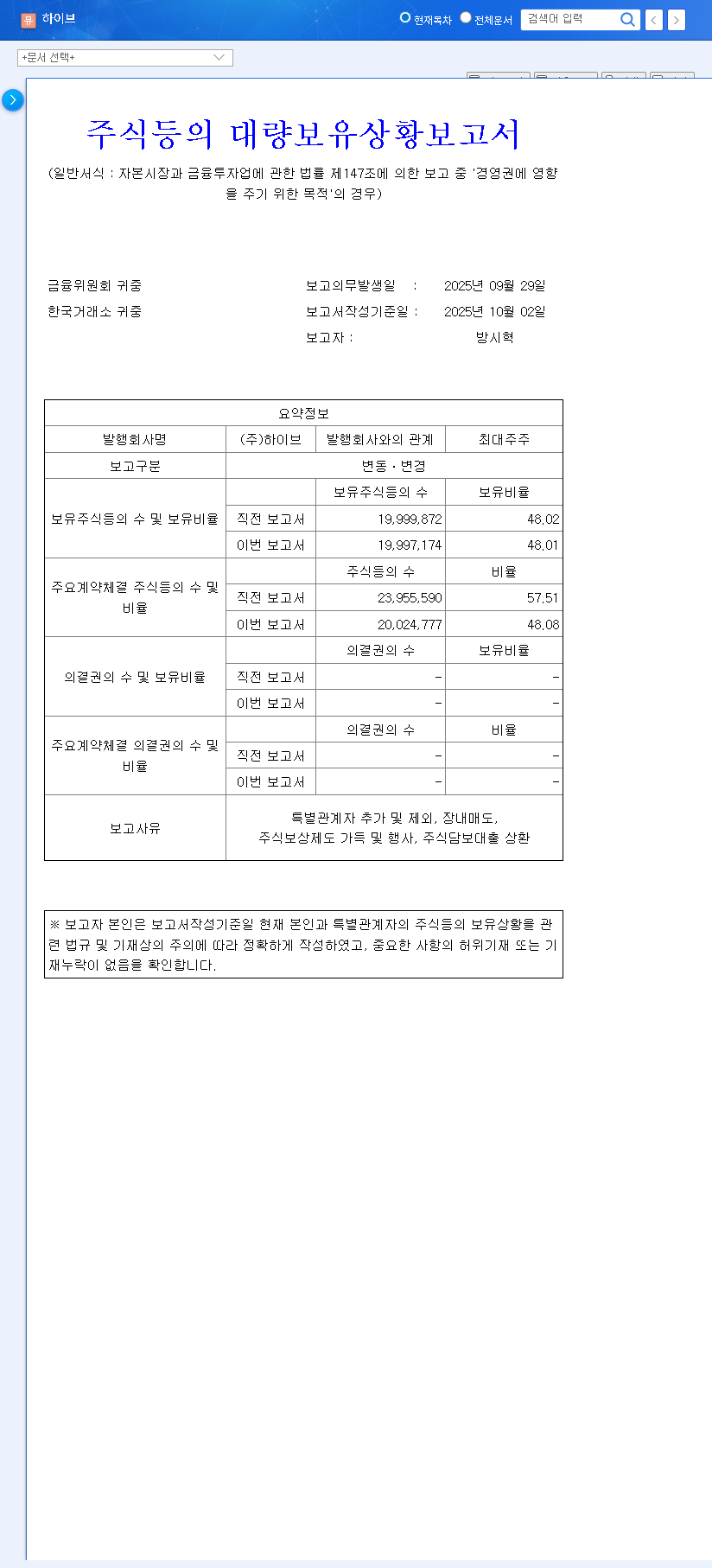

The catalyst for this discussion is the ‘Report on Status of Large Shareholder’s Holding (General)’ filed on October 2, 2025. You can view the Official Disclosure on DART. At first glance, the numbers seem almost negligible, but the reasons behind them tell a story of internal strategy and financial prudence.

The Key Figures at a Glance

- •Main Reporting Party: Chairman Bang Si-hyuk

- •Ownership Before Change: 48.02%

- •Ownership After Change: 48.01%

- •Net Change: A slight decrease of 0.01%

The primary drivers behind this adjustment were multifaceted, involving standard corporate operations rather than a single large transaction. These include the vesting of employee stock options, minor on-market sales by executives for personal financial management, and, notably, the repayment of stock-backed loans. This indicates a focus on rewarding talent and strengthening the company’s financial footing.

“Minor adjustments in a founder’s stake are common. The key for investors is to analyze the ‘why’ behind the change. In HYBE’s case, the reasons—employee compensation and debt reduction—point towards healthy, long-term corporate governance, not a lack of confidence.”

Beyond the Numbers: HYBE’s Unshakable Fundamentals

To truly understand the minimal impact of this shareholding change, one must look at the powerhouse fundamentals HYBE has built. The H1 2025 financial report paints a picture of a company that is not just surviving but thriving through strategic diversification and innovation.

Core Strengths Fueling Growth

- •Profitability on the Rise: Despite market fluctuations, operating profit surged by over 34%. This wasn’t driven by revenue alone but by masterful cost control and focusing on high-margin sectors like world tours and merchandise.

- •Diversified Revenue Streams: HYBE has successfully reduced its dependency on physical album sales. The explosive growth in concerts (featuring artists like SEVENTEEN and LE SSERAFIM) and high-demand MD/licensing has created a more resilient and balanced business model.

- •Weverse Platform Dominance: The fan community platform Weverse is a critical growth engine. It deepens fan engagement and serves as a powerful e-commerce hub, creating a direct-to-consumer flywheel. For more on this, read our deep dive into HYBE’s Weverse platform strategy.

- •Investing in the Future: HYBE is not just a music label; it’s a tech company. Significant investments in game development and proprietary AI solutions signal a commitment to owning the future of entertainment technology.

Investor Outlook: Long-Term Value Over Short-Term Noise

Given the context, the 0.01% HYBE shareholding change is unlikely to have any meaningful negative impact on the stock price. In fact, the underlying reasons can be interpreted as net positives. Motivating key employees with stock compensation ensures talent retention, while repaying loans enhances financial stability—both are hallmarks of a well-run company. As reported by leading financial outlets like Bloomberg, market sentiment often rewards companies with strong governance and a clear vision for the future.

Key Factors to Monitor Moving Forward:

Instead of over-analyzing this minor stock ownership shift, a prudent HYBE investor analysis should focus on the strategic drivers that will truly shape its value:

- •Global Artist Pipeline: The success of upcoming group debuts and the continued global expansion of established acts will be paramount.

- •Weverse Monetization: Keep an eye on user growth, new feature rollouts, and the expansion of its e-commerce and subscription services.

- •New Venture Performance: The tangible results from investments in gaming and technology will be crucial for long-term diversification.

In conclusion, the recent news about the HYBE shareholding change should be seen as business as usual. It’s a small technical adjustment within a much larger, compelling growth story. For investors, the focus should remain on the company’s strong execution, its multi-layered business strategy, and its dominant position in the expanding global market for K-POP entertainment stocks. The intrinsic value of HYBE lies in its innovation and vision, not in the third decimal place of its founder’s ownership percentage.