The recent announcement of an nTels treasury stock disposal has captured the attention of the market. On November 14, 2023, nTelsCo.,Ltd. (엔텔스) disclosed its plan to dispose of treasury shares specifically for employee bonuses. This move, while a common corporate action, arrives at a pivotal moment, following a quarter of significant financial improvement. For investors, the key question is whether this is a routine financial maneuver or a strategic signal of confidence in the company’s future growth trajectory. This comprehensive financial analysis will unpack the implications of this decision, examine the robust Q3 2023 performance, and outline what investors need to know to make informed decisions.

Is the nTels treasury stock disposal a simple compensation plan or a bullish indicator? By combining this event with a detailed look at the company’s fundamentals, we can uncover the true narrative for nTels stock.

Disposal Details and Company Context

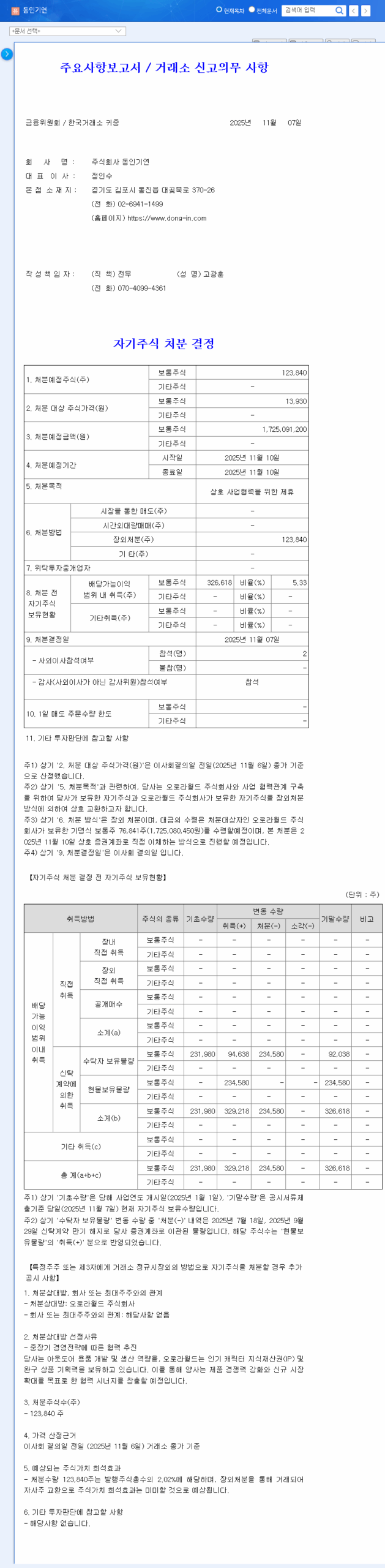

nTelsCo.,Ltd., a key player in providing telecommunications software and solutions like Business/Operations Support Systems (B/OSS), is navigating the dynamic landscape of 5G and IoT integration. The company’s decision, as per the Official Disclosure (DART Report), involves the disposal of 140,000 common shares. This represents approximately 1.37% of the total outstanding shares, valued at around KRW 700 million.

The stated purpose is explicit: to grant bonuses to executives and employees. This is a crucial detail. Unlike disposals aimed at raising capital, which can lead to share dilution, this action is designed to incentivize and retain key talent—a move often interpreted by the market as a sign of management’s confidence in sustained future performance.

Deep Dive: nTels Financial Analysis for Q3 2023

The treasury stock disposal does not happen in a vacuum. It is framed by an exceptionally strong third quarter in 2023, which suggests a fundamental turnaround. Let’s examine the key performance indicators:

- •Surging Revenue & Profitability: Revenue skyrocketed by 59.2% year-over-year to KRW 46.647 billion. Even more impressively, operating profit shifted from a loss to a surplus of KRW 1.44 billion, signaling a significant operational turnaround fueled by its core B/OSS solution business.

- •Explosive Global Growth: International sales were a standout performer, surging 119.8% to KRW 8.088 billion. This indicates that nTels is successfully expanding its footprint beyond domestic markets, a critical driver for long-term growth.

- •Robust Order Backlog: The total order backlog swelled by 93.5% from the end of the previous year to KRW 72.254 billion. This provides strong revenue visibility and a stable foundation for the upcoming quarters.

Areas for Continued Scrutiny

Despite the stellar top-line growth, a complete nTels financial analysis requires a balanced view. Key profitability metrics like Return on Equity (ROE) at 0.13% and Earnings Per Share (EPS) at 4 KRW remain low. Furthermore, operating cash flow is still negative. This suggests that while the company is growing rapidly, it must now focus on converting that growth into efficient, sustainable profit and positive cash flow.

Impact of the nTels Treasury Stock Disposal

Short-Term Market Implications

In the short term, the impact on the nTels stock price is expected to be minimal. The volume (1.37%) is too small to create significant selling pressure. More importantly, the market often views disposals for employee compensation positively, as it aligns employee interests with shareholder value and signals a commitment to retaining talent. When combined with the strong Q3 results, the immediate market reaction is likely to be neutral to positive.

Mid-to-Long-Term Strategic Value

The long-term effect is more strategic than financial. By rewarding performance, nTels aims to boost morale and productivity, which can serve as an indirect catalyst for innovation and operational excellence. This internal strengthening aligns perfectly with the company’s external growth story, driven by its expanding order backlog and international success. It’s a move to ensure the internal engine is just as robust as the external opportunities.

Actionable Investor Checklist

For those considering an investment in nTels, the focus should be on the underlying fundamentals rather than the disposal event itself. Here are key points to monitor:

- •Sustainability of Growth: Is the Q3 performance a one-time event or the start of a new, sustainable growth phase? Look for continued strength in international sales and new contracts in the 5G and IoT sectors in subsequent earnings reports.

- •Path to Profitability: Keep a close eye on ROE, EPS, and operating cash flow. The next step in nTels’ evolution is to translate its impressive revenue growth into bottom-line profit and positive cash generation.

- •Competitive Landscape: How is nTels positioned against its competitors in the B/OSS and telecom software space? Understanding their competitive advantage is key to assessing long-term viability. Consider reading our broader report on Investing in the Korean Tech Sector for more context.

Conclusion: A Bullish Signal Backed by Fundamentals

The nTels treasury stock disposal should be viewed not as an isolated event, but as a confident internal maneuver that complements a powerful external growth story. The action itself is a healthy sign of a company investing in its people. However, the true investment thesis rests on the impressive fundamental improvements seen in Q3 2023. Investors should focus on the company’s ability to maintain its growth momentum, particularly in international markets, and its strategic efforts to enhance profitability. If nTels can continue this trajectory, this period may be remembered as a significant inflection point for the company.