The recent announcement of the HJ Shipbuilding & Construction asset disposal has sent ripples through the investment community. The company’s decision to sell off ₩22.1 billion in corporate shares and equity securities is officially aimed at ‘securing liquidity.’ However, against a backdrop of deteriorating financial health, investors are right to question whether this move is a savvy financial maneuver or a desperate measure to stay afloat. This comprehensive analysis will delve into the specifics of the sale, the company’s precarious financial state, and what this means for potential and current investors.

While an injection of ₩22.1 billion provides immediate breathing room, it doesn’t solve the core issue: a fundamental decline in profitability. This asset sale must be viewed as a symptom, not a cure, for HJSC’s current challenges.

Unpacking the ₩22.1 Billion Asset Disposal

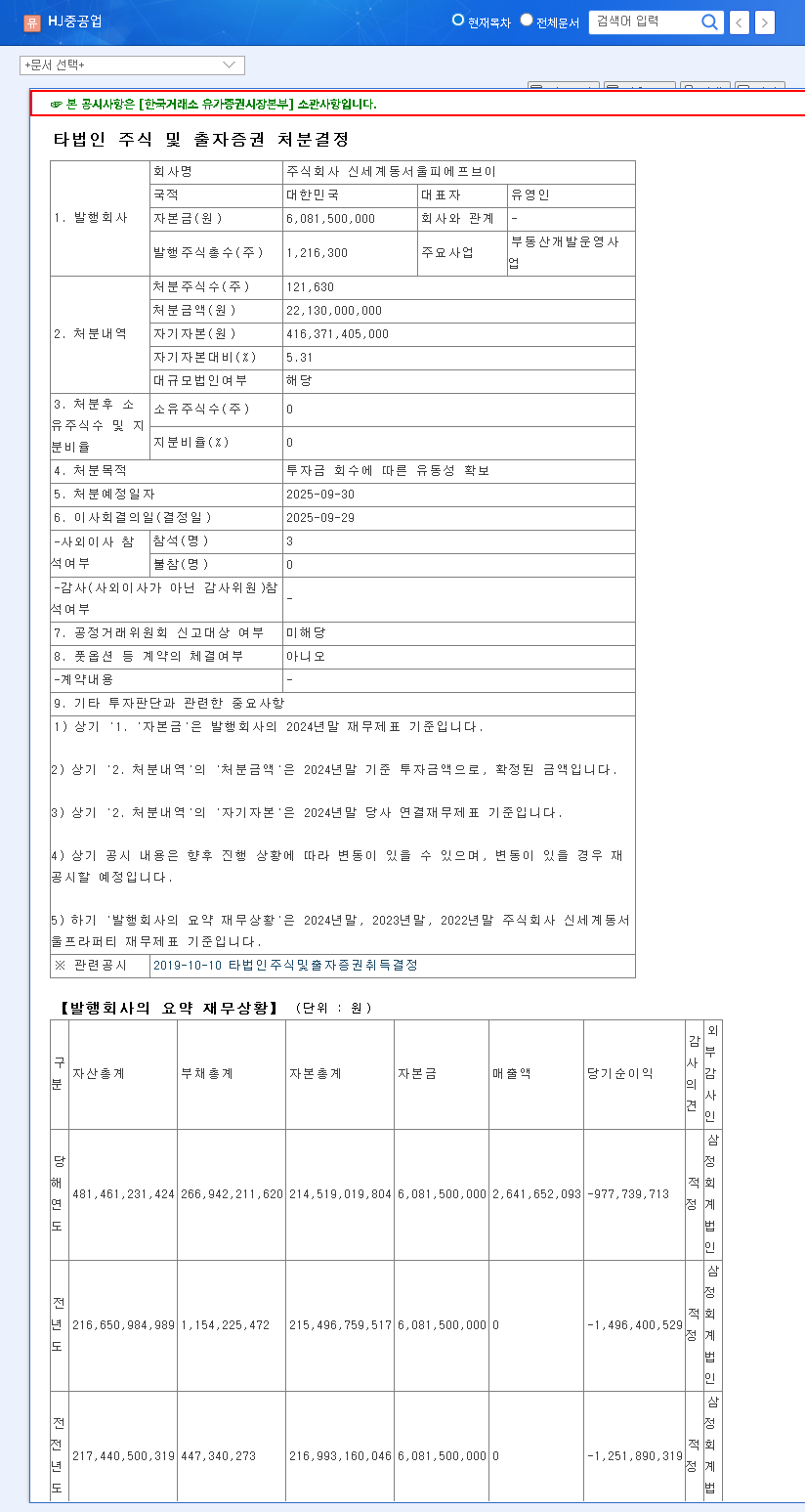

On September 29, 2025, HJ Shipbuilding & Construction (HJSC) confirmed the disposal of its entire stake in Shinsegae Dongseoul PFV, a real estate development and operation business. The transaction, valued at ₩22.1 billion, represents a significant 5.31% of HJSC’s total capital. The company’s stated purpose is clear: to recover its investment and enhance its liquidity position. While on the surface this seems like a standard corporate finance strategy, the timing and context of this decision raise critical questions about the company’s underlying stability and future prospects.

A Deeper Look: The Financial Storm Behind the Sale

To fully understand the gravity of this asset sale, one must examine HJSC’s recent financial performance, which paints a troubling picture. The decision was not made from a position of strength but rather amidst a period of significant operational and financial decline.

Plummeting Revenue and Deepening Losses

The company’s fundamentals have been weakening alarmingly. The sharp decline in key performance indicators highlights a core profitability crisis that the HJ Shipbuilding & Construction asset disposal aims to temporarily patch.

- •Revenue Collapse: Annual revenue plummeted from ₩91.2 billion in 2022 to a mere ₩31.6 billion in 2024, a staggering drop that signals a severe contraction in business operations.

- •Profitability Crisis: The company swung from a healthy operating profit of ₩10.3 billion in 2022 to an operating loss of ₩15.9 billion in 2024. Key metrics like net profit margin and Return on Equity (ROE) have also turned negative, falling from 10.97% to -0.84%.

- •Misleading Stability: Paradoxically, the debt-to-equity ratio improved to 7.90%. However, this is likely a result of asset sales and a shrinking equity base rather than genuine financial strengthening, creating a deceptive picture of stability.

Industry and Macroeconomic Headwinds

HJSC’s struggles are compounded by a complex global economic environment. Fluctuating exchange rates, particularly the weakening Won, can impact material costs and foreign contracts. Furthermore, global interest rate policies and fluctuating freight indices create an unpredictable landscape for the shipbuilding and construction sectors. According to analyses from sources like Reuters, geopolitical tensions and supply chain disruptions continue to pose significant risks to the industry, making operational efficiency and a strong balance sheet more critical than ever.

A Prudent Investor’s Action Plan

Given the negative context surrounding the HJ Shipbuilding & Construction asset disposal, investors should proceed with extreme caution. The short-term liquidity boost is overshadowed by long-term concerns about the company’s core business viability. A defensive and analytical approach is warranted.

- •Demand Transparency: Scrutinize future company announcements for a clear, strategic plan to address the root causes of the revenue decline and operating losses. Vague statements are a major red flag.

- •Analyze Financial Reports: Look beyond the headlines. Dig into the next quarterly report to see how the proceeds from the sale are being used. Are they funding new, profitable projects or simply covering operational shortfalls?

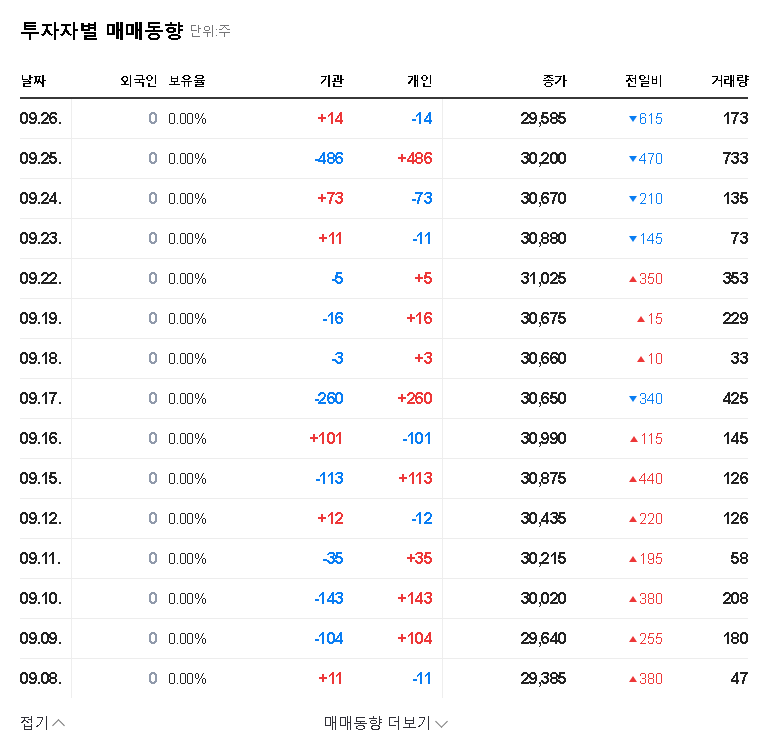

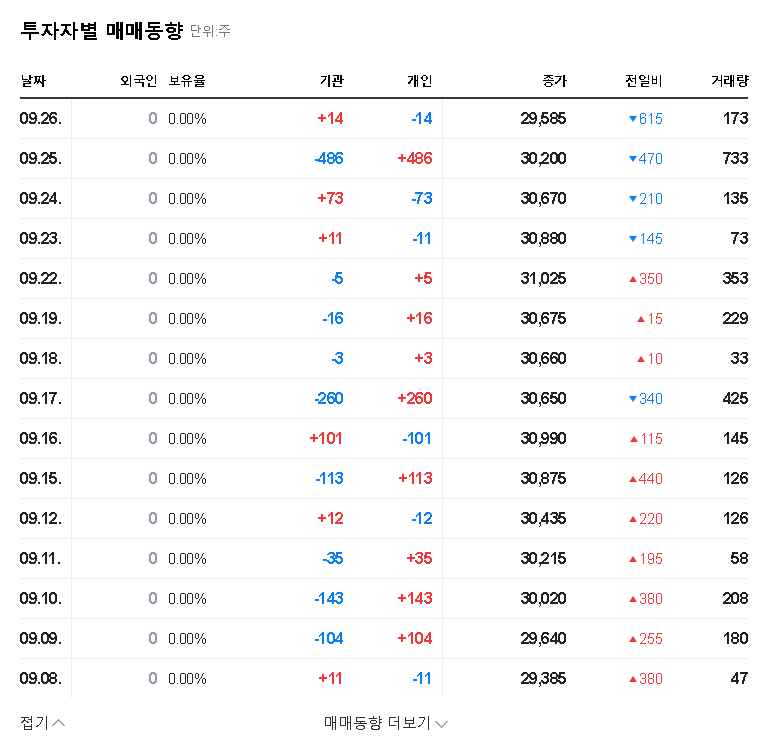

- •Monitor Stock Volatility: HJSC’s stock has a history of high volatility. This event is likely to create further instability. Avoid making aggressive moves and consider the high-risk nature of this investment. For more on this, see our guide to analyzing volatile industrial stocks.

Final Verdict: A Signal for Caution

In conclusion, the ₩22.1 billion asset disposal by HJ Shipbuilding & Construction should be interpreted primarily as a negative signal. It is a reactive move to combat severe financial distress, not a proactive step towards strategic growth. While the cash infusion may delay a liquidity crisis, it does not address the fundamental erosion of the company’s profitability. Investors should view this event as a clear warning sign and demand a comprehensive turnaround plan before considering this a viable long-term investment.