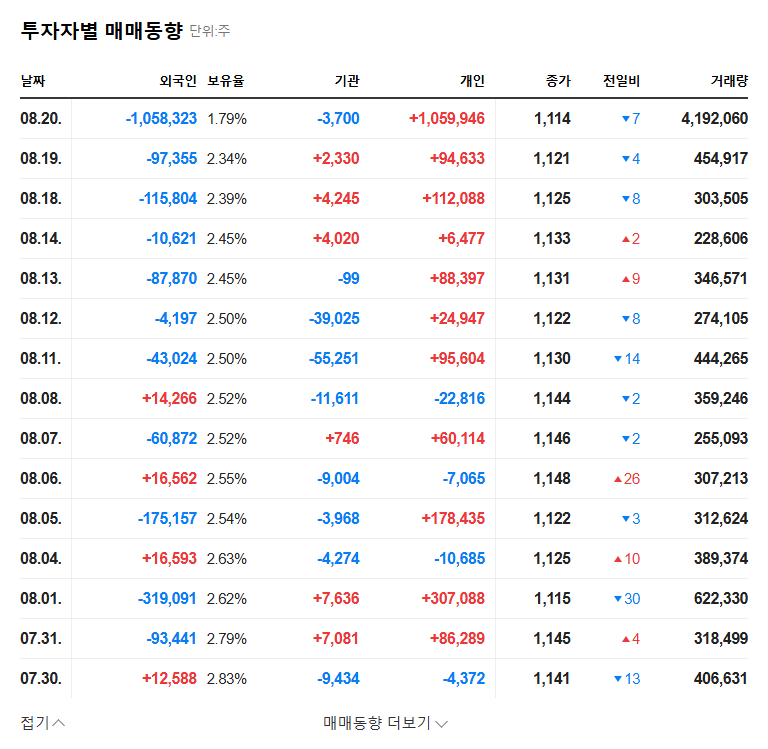

The recent announcement of the HanWool Semiconductor convertible bond (CB) issuance has sent ripples through the investment community. The decision to raise KRW 5 billion through a privately placed CB raises a critical question: is this a savvy move to fuel future growth, or does it signal underlying financial strain and pose a significant dilution risk for current shareholders? This comprehensive guide will dissect every facet of this financial instrument, analyze the company’s strategy, and provide a clear roadmap for investors navigating this pivotal moment.

We’ll explore the immediate implications and long-term potential, ensuring you have the data-driven insights needed to make an informed decision about your investment in HanWool Semiconductor.

The Details: Breaking Down the HanWool Semiconductor CB Issuance

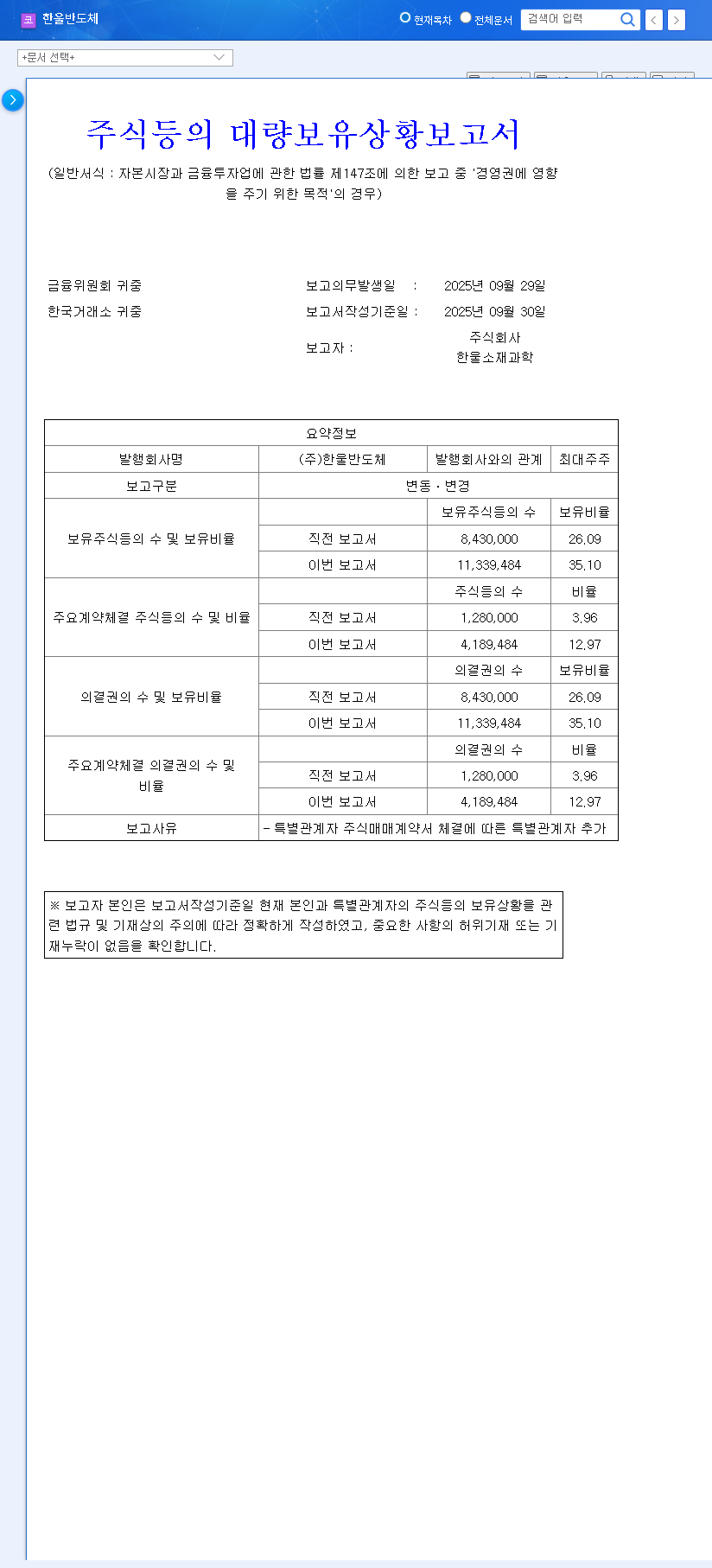

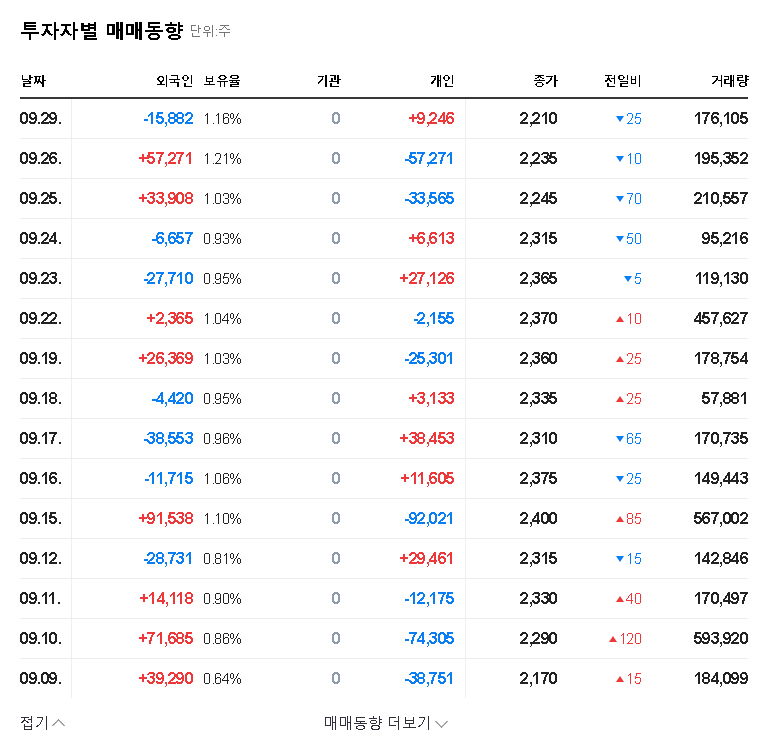

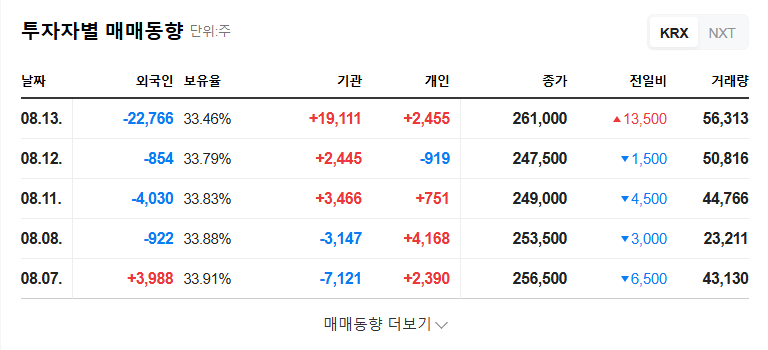

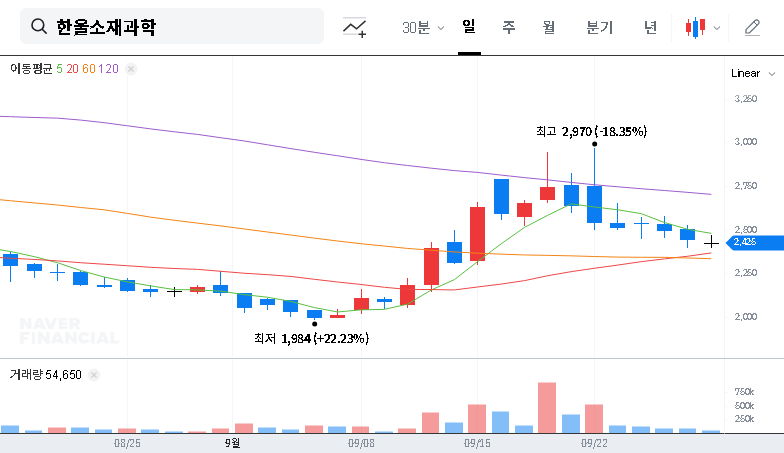

On November 13, 2025, HanWool Semiconductor, Inc. officially confirmed its plan to issue a privately placed convertible bond valued at KRW 5 billion. As detailed in the Official Disclosure on DART (Source), the key terms are critical for investors to understand:

- •Investor: The entire issuance is allocated to ‘Excel Fund No. 1’.

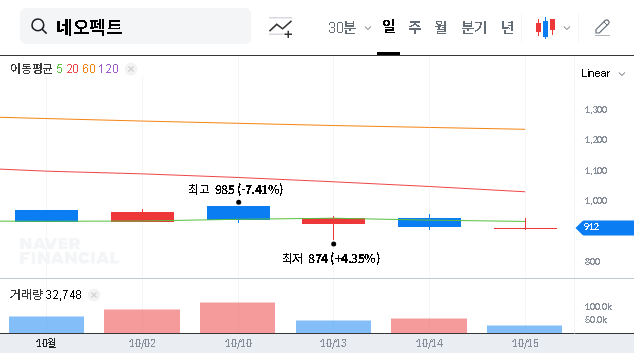

- •Conversion Price: Set at KRW 1,928, which is a discount from the prevailing market price of KRW 2,200 at the time of the announcement.

- •Coupon & Maturity Rate: A fixed rate of 3% for both.

- •Payment & Conversion Timeline: Payment is due December 12, 2025, with the conversion period opening one year later on December 12, 2026.

A convertible bond is a hybrid security that starts as a bond but can be converted into a specified number of common shares. The discounted conversion price (KRW 1,928) creates a strong incentive for the bondholder to convert to stock if HanWool’s share price remains above this level, leading to potential equity dilution. For more on this, see this comprehensive guide from Investopedia.

Why Now? The Strategy Behind the Capital Injection

This fundraising initiative is not happening in a vacuum. A look at HanWool’s 2025 semi-annual report reveals a company at a crossroads, facing significant headwinds but actively pivoting towards new, high-growth sectors.

Confronting Financial Challenges

The company has been battling declining revenue and widening operating losses. This is primarily due to a slowdown in the broader semiconductor and display industries, which has depressed sales of its core Film inspection equipment. Compounding this issue are rising administrative costs and the unpredictable nature of global exchange rates, which impacts a company with a 53% export ratio.

Investing in a High-Tech Future

Despite these pressures, HanWool is not standing still. The KRW 5 billion from the HanWool Semiconductor convertible bond is earmarked as strategic capital to fuel its expansion into promising new ventures:

- •AI Machine Vision: A rapidly growing field essential for automated quality control and inspection in advanced manufacturing.

- •Semiconductor IP: Developing and licensing intellectual property for chip designs, a high-margin business that leverages its core expertise.

- •Advanced Materials: Innovating in the materials space, which is fundamental to the next generation of semiconductors.

This financing is a calculated move to bridge the gap from a challenging present to a potentially lucrative future, powered by innovation.

The Investor’s Dilemma: Opportunity vs. Risk

The Bull Case: Fuel for Growth

The primary positive outcome is the injection of vital capital. This KRW 5 billion infusion improves liquidity and provides the necessary funds for R&D and strategic investments. If the new ventures in AI and semiconductor IP succeed, they could transform HanWool’s revenue streams and lead to significant long-term appreciation in shareholder value. This aligns with the company’s efforts to improve its financial health, as seen in previous capital increases and a focus on its extensive patent portfolio.

The Bear Case: Dilution and Debt

The most significant risk is equity dilution. If and when the bonds are converted, the total number of outstanding shares will increase, which can decrease the value and ownership stake of each existing share. The 3% interest on the bonds also adds a new financial burden. If the company’s turnaround is delayed, these interest payments could become a strain on cash flow. The private placement nature of the deal also means less transparency for retail investors. For more analysis on this topic, consider our guide to analyzing semiconductor stocks.

Investor Takeaway: A Cautious but Watchful Approach

The HanWool Semiconductor convertible bond is a double-edged sword. It presents a clear path to funding innovation but comes with the unavoidable risk of future dilution.

The key factor for investors is execution. Your focus should be on monitoring the tangible progress of HanWool’s new business divisions. Are they securing contracts? Are they hitting R&D milestones? Is the capital being deployed effectively to generate future revenue?

While the conversion price suggests a short-term stock price collapse is unlikely, the overhang of potential new shares will persist. A prudent strategy involves closely tracking the company’s quarterly reports for signs of fundamental improvement while keeping an eye on macroeconomic factors like the recovery of the front-end semiconductor industry. This is an investment that requires patience and diligent monitoring.