The recent announcement of the FINO INC. copper supply contract, a massive 11.8 billion KRW deal with CITIC Metal(HK) Limited, has sent ripples through the investment community. For stakeholders in FINO INC., the critical question is clear: Does this contract signal a new era of growth and profitability, or is it a short-term revenue spike with underlying risks? This analysis provides a comprehensive breakdown for investors, leveraging official data to explore both the significant opportunities and the crucial cautionary points.

We will dissect the contract’s details, evaluate its potential impact on FINO’s stock performance, and outline a strategic action plan for investors navigating this pivotal moment. This deep dive aims to move beyond the headlines, offering the clarity needed for informed decision-making.

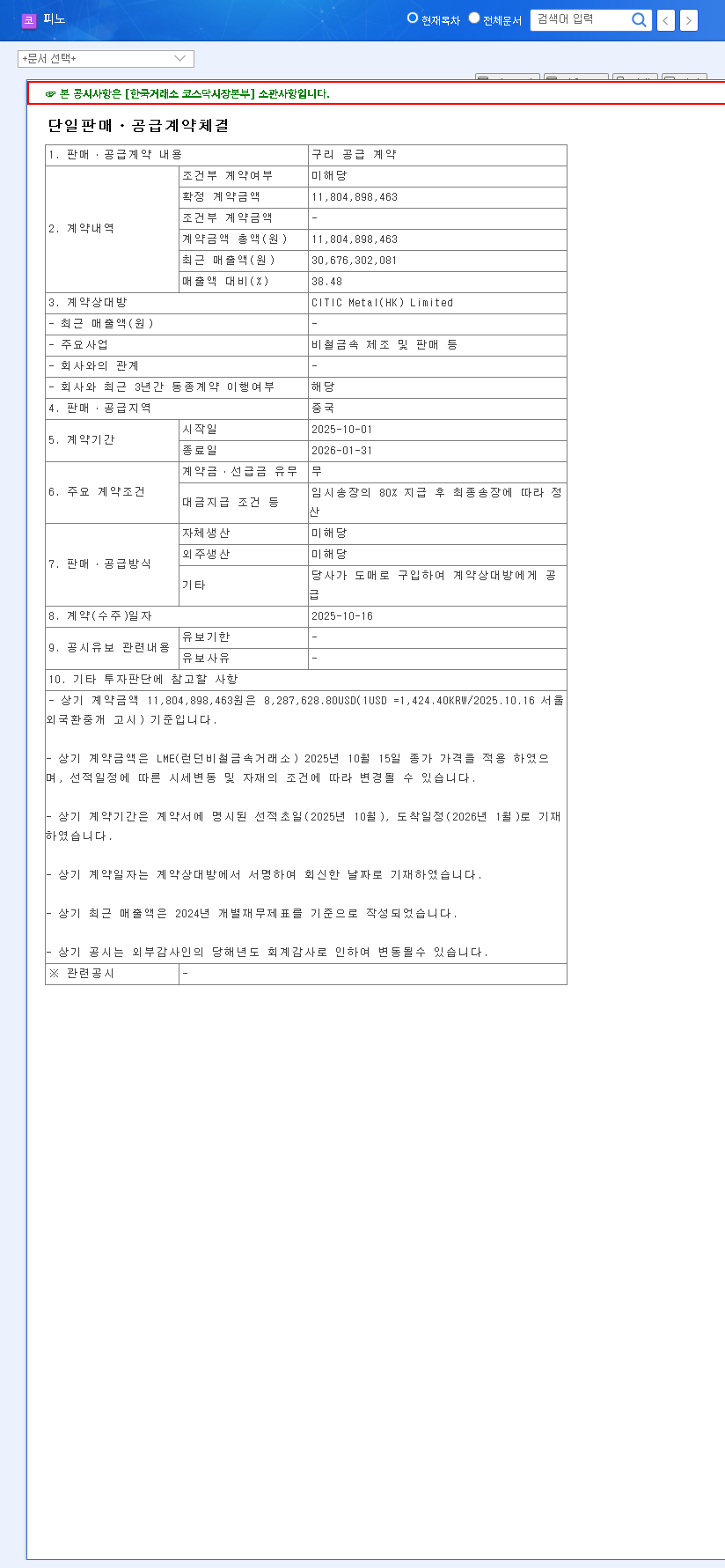

Breaking Down the 11.8 Billion KRW Deal

On October 16, 2025, FINO INC. formally announced a landmark agreement that demands investor attention. This analysis is based on information from the company’s Official Disclosure. The key parameters of this copper supply contract are as follows:

- •Counterparty: CITIC Metal(HK) Limited

- •Contract Value: 11,800,000,000 KRW (approximately 8.5 million USD)

- •Contract Period: October 1, 2025 – January 31, 2026 (4 months)

- •Supply Region: China

- •Significance: Represents a staggering 38.48% of the company’s sales for the equivalent period.

The Bull Case: Why This Contract is a Major Win

The immediate implications of this deal are overwhelmingly positive and could serve as a powerful catalyst for FINO INC.’s stock. Here’s why this is more than just another sale.

1. Substantial Short-Term Performance Boost

A revenue injection of 11.8 billion KRW concentrated over Q4 2025 and Q1 2026 is poised to dramatically improve FINO’s income statement. This isn’t a minor increase; it’s a significant event that will likely lead to a strong earnings report, potentially beating analyst expectations and driving positive investor sentiment.

2. Strategic Entry into the Chinese Market

Securing a contract with a major entity like CITIC Metal(HK) Limited provides FINO with a credible foothold in the vast Chinese market. This partnership serves as a powerful endorsement of FINO’s product quality and reliability, potentially opening doors to further contracts and long-term relationships in the region.

This deal is not just about revenue; it’s a strategic validator. Successfully fulfilling this contract could fundamentally change FINO INC.’s international standing and future growth trajectory.

The Bear Case: Potential Risks to Consider

While the upside is compelling, prudent investors must weigh the potential risks associated with the FINO INC. copper supply contract. These factors could temper the long-term outlook.

1. The ‘Revenue Cliff’ and Contract Continuity

The contract’s four-month duration is a double-edged sword. While it provides a quick boost, it raises concerns about what happens in Q2 2026. Is this a one-time transaction or the start of an ongoing partnership? Without confirmation of renewal or follow-on deals, FINO faces a potential ‘revenue cliff’ that could make year-over-year comparisons look poor in the future.

2. Commodity Price Volatility

The global copper market is notoriously volatile. Copper prices, influenced by global economic health, supply chain disruptions, and geopolitical events, can fluctuate wildly. As noted by sources like the London Metal Exchange, these shifts can severely impact profitability. If FINO’s contract doesn’t include hedging mechanisms, a sudden spike in raw material costs could erode or even erase the profit margins on this large deal.

3. Geopolitical and Market Concentration Risk

By supplying exclusively to China for this contract, FINO increases its exposure to a single market’s economic and political climate. Any shifts in Chinese industrial policy, trade relations, or economic slowdown could impact future business prospects and create a concentration risk that investors should monitor.

Investor Action Plan & Final Thoughts

The FINO INC. copper supply contract is undeniably a significant positive development. However, the associated risks necessitate a cautious and informed approach. Investors should prioritize the following actions:

- •Monitor Future Disclosures: Pay close attention to quarterly reports and any further announcements regarding contract extensions or new agreements with CITIC Metal.

- •Analyze Profit Margins: In the upcoming financial statements, scrutinize the gross profit margins. This will reveal how effectively FINO managed costs amidst copper price fluctuations. For more on this, see our guide to understanding FINO INC.’s financial health.

- •Track Copper Market Trends: Keep an eye on the broader copper market. Sustained high demand is a positive sign, while a downturn could signal headwinds for FINO.

In conclusion, this contract provides a powerful short-term tailwind for FINO INC. The key to unlocking long-term value will be the company’s ability to convert this single major deal into a sustainable international partnership. Cautious optimism, paired with diligent monitoring, is the recommended strategy.