A significant cloud of uncertainty has lifted for investors. The long-standing CJ CGV lawsuit, a major point of concern for the conglomerate, has been officially resolved, signaling a pivotal moment for both the subsidiary and its parent, CJ Group. This development removes a critical CJ CGV legal risk and paves the way for a renewed focus on growth and profitability, directly impacting the outlook for any CJ Group investment. This analysis explores the profound implications of this resolution on the company’s fundamentals, stock potential, and strategic future.

By understanding the details of this event, investors can more accurately assess the company’s value proposition and formulate more informed strategies for engaging with CJ CGV stock and the broader CJ Group portfolio.

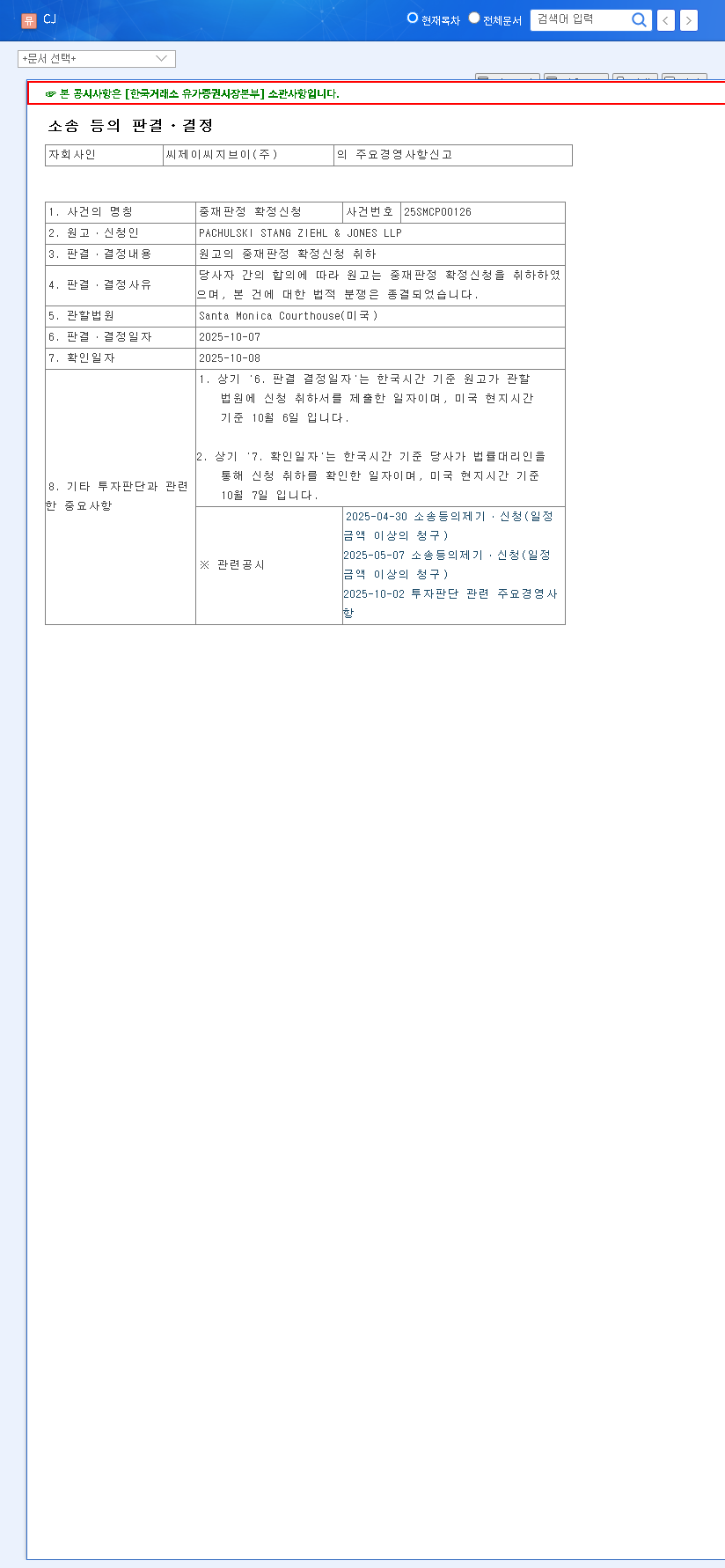

The Landmark Resolution: What Happened with the CJ CGV Lawsuit?

On October 10, 2025, a decisive action concluded a period of significant legal uncertainty. The plaintiff, PACHULSKI STANG ZIEHL & JONES LLP, officially withdrew its application for the confirmation of an arbitration award (Case No. 25SMCP00126) in a U.S. court. This withdrawal was the result of a mutual agreement between the involved parties, effectively ending the dispute before it could escalate into a more costly and prolonged legal battle. The formal announcement can be reviewed in the Official Disclosure filed with the regulatory authorities.

“The resolution of the CJ CGV lawsuit is a classic case of de-risking. When a known negative variable is removed from the equation, the market is free to re-evaluate the company based on its core operational strength and future potential. We see this as a clear positive for CJ Group fundamentals.”

Why This Matters: A Deep Dive into the Impact

The end of this legal challenge is far more than a simple footnote in a corporate filing. It triggers a cascade of positive effects across the organization, from financial stability to strategic focus.

1. Bolstering CJ Group’s Core Fundamentals

A healthy subsidiary is crucial for a healthy parent company. By resolving this issue, CJ CGV removes a potential financial drain and reputational risk, which in turn strengthens the entire CJ Group’s profile. This enhances financial stability by averting potential litigation costs and damage awards, a factor that rating agencies and large-scale investors watch closely. A stable financial base is critical for maintaining the group’s ‘AA-‘ credit rating and managing debt efficiently, as noted by financial analysts at sources like Bloomberg.

2. Unlocking Strategic Focus and Synergy

With legal distractions in the rearview mirror, CJ CGV’s management can now dedicate 100% of its attention to its core business: innovating the cinema experience and navigating the post-pandemic entertainment landscape. This renewed focus is expected to accelerate performance improvements and strengthen synergies with sister company CJ ENM. The potential to create a seamless content pipeline—from production (CJ ENM) to exhibition (CJ CGV)—is a cornerstone of a sound CJ Group investment thesis. For more on this, you can read our analysis of CJ ENM’s content strategy.

3. Reshaping Market and Investor Perceptions

For months, the CJ CGV legal risk was an overhang on the stock, potentially suppressing its value. Its removal is a powerful catalyst for a market re-rating. Investors who were previously hesitant may now view the company with renewed confidence. This positive sentiment is expected to reduce perceived business risk for the entire group, enhancing its overall investment appeal and potentially leading to a more favorable valuation for CJ CGV stock.

The Path Forward: Outlook & Investor Takeaways

The resolution of the CJ CGV lawsuit has both immediate and long-term implications that investors should monitor closely.

- •Short-Term Outlook: Expect a positive reaction in the market as uncertainty is priced out. The removal of this risk factor should improve investor sentiment and could provide an immediate lift to both CJ and CJ CGV’s stock prices.

- •Mid-to-Long-Term Outlook: The true test will be in execution. Investors should watch for tangible signs of progress, such as improved profitability at CJ CGV, new strategic initiatives focused on growth, and concrete examples of enhanced synergy with CJ ENM. These will be key indicators that the company is capitalizing on its newfound stability.

Frequently Asked Questions (FAQ)

How does this directly affect CJ CGV’s finances?

While not a direct revenue event, it’s a significant cost-avoidance victory. It eliminates the risk of a large financial payout and ongoing legal fees. This preserves capital that can now be reinvested into core business operations, technology upgrades (like 4DX and ScreenX), and strategic growth, thereby indirectly strengthening the balance sheet.

Is CJ Group now a more attractive investment?

The removal of a major subsidiary’s legal risk certainly enhances the attractiveness of a CJ Group investment. It demonstrates proactive risk management and allows the market to focus on the group’s strong portfolio of businesses in food, logistics, and entertainment. This event strengthens the overall investment case by improving the stability and predictability of future earnings.