The recent CJ CGV lawsuit settlement has captured the attention of the market, sparking debate among investors. With the resolution of this long-standing legal battle, many are asking if this marks a genuine turning point for the company’s financial stability or if it’s merely a temporary reprieve. This analysis will move beyond the headlines to provide a comprehensive look at what this development means for the CJ CGV stock and your potential investment strategy.

We will dissect the company’s challenging H1 2025 fundamentals, evaluate the macroeconomic headwinds, and offer a clear, actionable plan for investors navigating this complex landscape. Is now the time to buy, sell, or hold? Let’s find out.

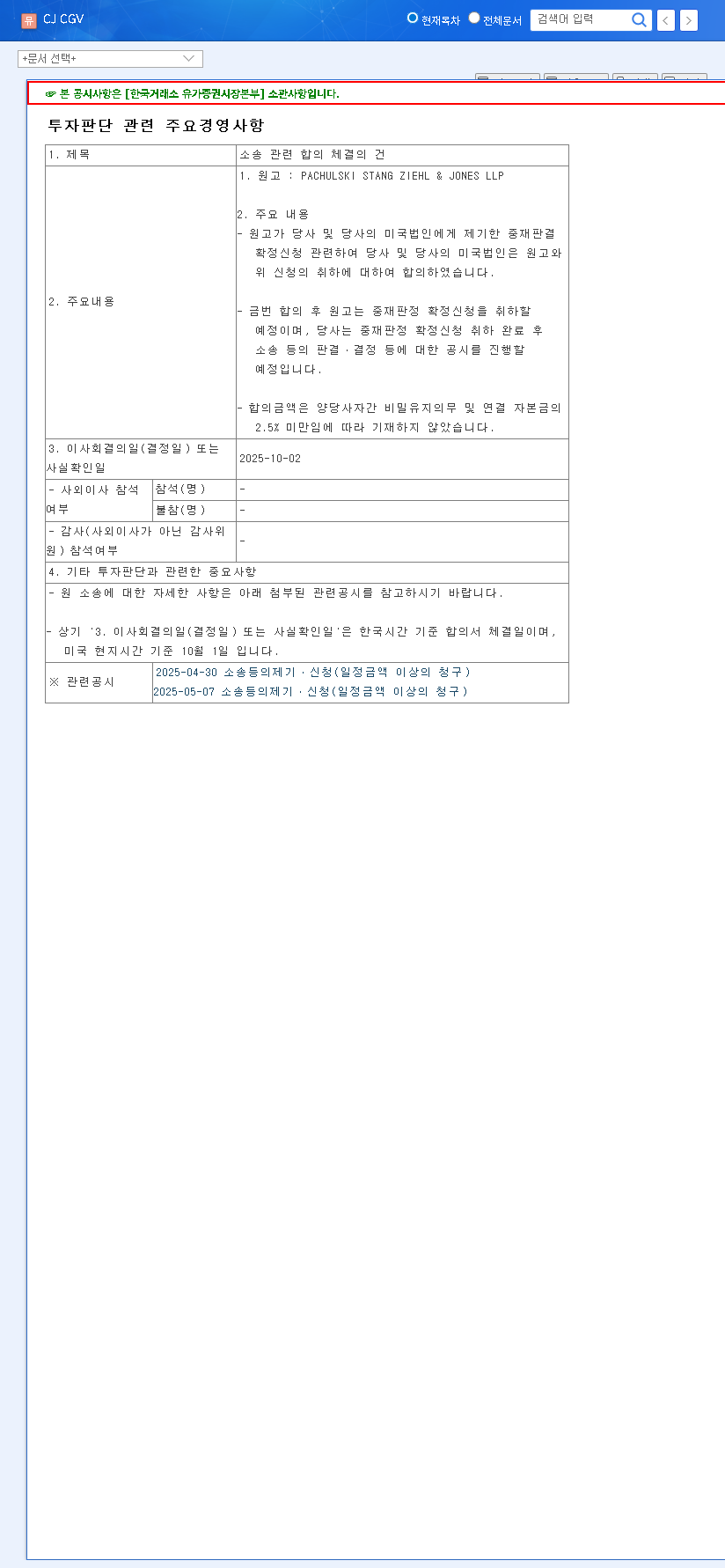

What Happened? The Lawsuit Settlement Explained

On October 2, 2025, CJ CGV officially announced an agreement with PACHULSKI STANG ZIEHL & JONES LLP, settling a petition to confirm an arbitration award. As part of the agreement, the plaintiff is set to withdraw their petition, bringing a close to a period of significant legal uncertainty for the entertainment giant. The full details were published in an Official Disclosure (DART Report).

While confidentiality clauses keep the exact settlement figure under wraps, sources confirm the amount is less than 2.5% of the company’s consolidated capital. This suggests a financially manageable outcome that avoids a catastrophic cash outflow, which is a positive sign. The primary benefit of the CJ CGV lawsuit settlement is not financial, but strategic—it removes a major distraction and a source of negative sentiment that has been looming over the company’s management and stock price.

CJ CGV’s Financial Health: A Look Under the Hood (H1 2025)

While the settlement is a step in the right direction, it doesn’t erase the fundamental financial challenges CJ CGV faces. The first half of 2025 painted a picture of a company struggling with profitability in its core business, even as revenue expanded.

The Revenue vs. Profitability Disconnect

Analysis of the H1 2025 report reveals several critical points:

- •Revenue Growth: Revenue saw a 24.6% year-on-year increase to KRW 1.025 trillion. However, this was primarily driven by the consolidation of the IT Service division (CJ OliveNetworks), not a robust recovery in the cinema business.

- •Plummeting Profits: Consolidated operating profit fell sharply to just KRW 4.918 billion. The core multiplex segment posted an operating loss of KRW 16.9 billion, signaling that getting audiences back into theaters remains a persistent challenge.

- •Widening Net Loss: The consolidated net loss expanded to KRW 76.304 billion, exacerbated by rising financial costs tied to the company’s significant debt.

The most alarming figure is the consolidated debt-to-equity ratio, which stands at a staggering 622%. This level of leverage makes the company highly vulnerable to interest rate fluctuations and severely restricts its financial flexibility.

Macroeconomic Headwinds and Market Pressures

CJ CGV is not operating in a vacuum. The global economic environment presents formidable challenges. Persistently high interest rates in major economies, including South Korea, continue to inflate the financial costs associated with CJ CGV’s large debt pile. According to financial news outlets like Reuters, central banks are remaining cautious, meaning relief from high borrowing costs may not come soon. Furthermore, fluctuating currency exchange rates and volatile logistics costs add layers of operational complexity and risk, particularly for its international ventures.

Investor Takeaway: A Balanced View of the Settlement

The Positive: Uncertainty Cleared

The key positive impact of the CJ CGV lawsuit settlement is the removal of a significant overhang. Litigation risk creates uncertainty that investors dislike, and its resolution can boost corporate image and investor sentiment. By settling for a modest amount, the company avoids a potentially much larger financial hit and can now refocus management attention on core operational improvements.

The Negative: Core Problems Persist

However, it’s crucial to recognize that this event is a painkiller, not a cure. The settlement does nothing to solve the underlying issues: a struggling multiplex division, fierce competition from streaming services, and a precarious balance sheet. The short-term cash outflow for the settlement, while manageable, is still a drain on a company that needs to preserve liquidity.

Revised CJ CGV Investment Strategy for 2025

Given this context, a prudent CJ CGV investment strategy requires careful monitoring of specific key performance indicators. While the settlement might cause a brief, positive rally in the CJ CGV stock, long-term value will be driven by fundamental improvements.

- •Focus on Deleveraging: The number one priority is debt reduction. Watch for asset sales, capital raising, or operational cash flow improvements specifically aimed at lowering the 622% debt-to-equity ratio.

- •Track the IT Division: The CJ OliveNetworks IT division is a bright spot. Monitor its growth trajectory and profit contribution. Its continued success is vital for offsetting losses in the cinema segment.

- •Multiplex Profitability Metrics: Look for signs of a turnaround in the core business. This includes higher audience numbers, increased per-patron revenue, and effective cost management. For more on this, see our guide on how to analyze entertainment sector stocks.

Conclusion: A Cautious Step Forward

In summary, the CJ CGV lawsuit settlement is a net positive, but its significance lies in risk mitigation rather than fundamental business enhancement. Investors should view it as one small piece of a much larger puzzle. The company’s future, and the trajectory of its stock, will be determined by its ability to tackle its deep-seated financial and operational challenges head-on. A cautious, data-driven approach is essential.

Disclaimer: This report is based on publicly available information and is for informational purposes only. It is not intended as investment advice. Investors bear sole responsibility for their investment decisions.