This comprehensive AMOREPACIFIC Q3 2025 earnings analysis unpacks the latest financial results from the K-beauty powerhouse. The recent preliminary earnings announcement for the third quarter of 2025 has sent mixed signals to investors. While a surprising beat in operating profit has generated optimism, misses in revenue and net profit highlight persistent challenges that require careful consideration. This deep dive will explore the key drivers behind these numbers, from the powerhouse performance of overseas markets fueled by the COSRX acquisition to the ongoing sluggishness in the crucial Chinese market.

For investors evaluating their position in AMOREPACIFIC stock, understanding the nuances behind the headline figures is paramount. We will dissect the fundamental strengths, potential risks, and strategic initiatives shaping the company’s future trajectory.

AMOREPACIFIC Q3 2025 Earnings: The Headline Figures

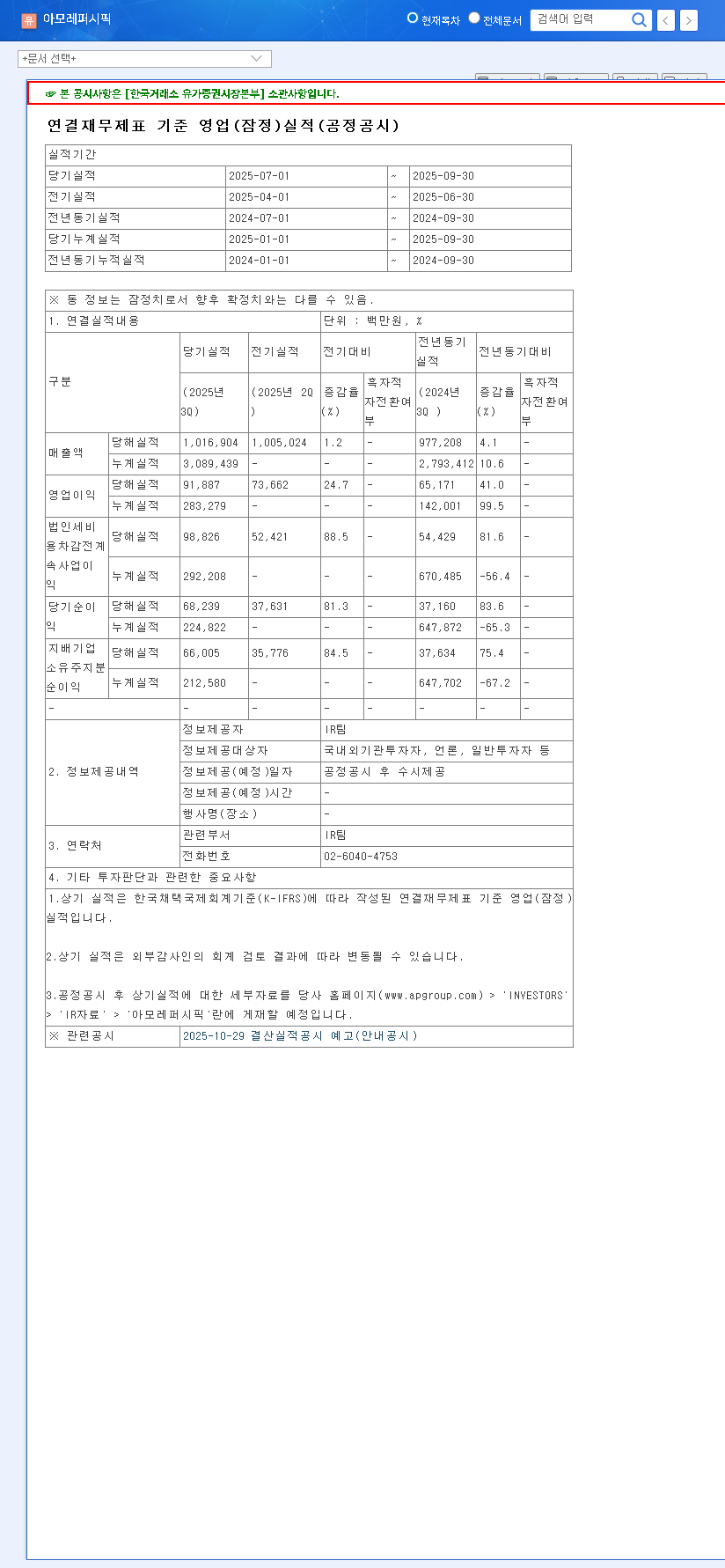

AMOREPACIFIC announced its preliminary consolidated financial results for the third quarter, which can be verified via the company’s Official Disclosure (DART). The results presented a complex picture when compared against market consensus, as reported by sources like Bloomberg.

While the market focused on the revenue miss, the significant outperformance in operating profit suggests underlying operational strengths and successful cost management initiatives are taking hold.

- •Revenue: KRW 1,016.9 billion, a 1% miss compared to the market expectation of KRW 1,031.4 billion.

- •Operating Profit: KRW 91.9 billion, a solid 2% beat against the forecast of KRW 89.8 billion.

- •Net Profit: KRW 66.0 billion, a significant 9% miss from the expected KRW 72.8 billion.

This divergence between operating profit and other key metrics demands a closer AMOREPACIFIC earnings analysis to understand the core factors at play.

Factors Driving the Operating Profit Surprise

The unexpected strength in operating profit wasn’t a fluke. It stemmed from a combination of successful strategic execution and disciplined financial management.

1. Explosive Growth in Global Markets

The standout performer was the overseas business, which saw a remarkable 26.6% increase in sales across the Americas, EMEA (Europe, Middle East, Africa), and other Asian markets (excluding China). This growth is a testament to the rising global demand for K-beauty stocks and brands. Critically, the integration of COSRX has proven to be a masterstroke. The brand’s focus on simple, effective ingredients at an accessible price point has resonated strongly with Western consumers, turbocharging growth in these key regions and validating the company’s M&A strategy.

2. Domestic Market Stabilization and Enhanced Profitability

On the home front, the domestic cosmetics business demonstrated resilience with 5.1% revenue growth. This was achieved by strengthening the competitiveness of core brands and adapting to new growth channels like Olive Young and online live commerce platforms. More impressively, stringent cost controls and a strategic shift toward higher-margin products led to a staggering 149.1% year-over-year surge in domestic operating profit, showcasing a significant improvement in profitability.

Headwinds and Challenges on the Horizon

Despite the positive profit story, the AMOREPACIFIC Q3 2025 earnings also highlighted several risks that investors must monitor closely. For a deeper dive into market trends, you can review our previous analysis of the K-beauty market.

- •Lingering Weakness in China: The modest growth in the Chinese market remains a primary concern. The rise of domestic ‘C-beauty’ brands and shifting consumer preferences create a highly competitive landscape that AMOREPACIFIC must navigate proactively.

- •Macroeconomic Pressures: Volatility in the EUR/KRW exchange rate could impact overseas profitability. Furthermore, rising prices for key raw materials require continuous management through hedging and strategic product pricing.

- •Balance Sheet Scrutiny: While necessary for growth, investments like the COSRX acquisition have led to a higher debt ratio. Additionally, a slowing inventory turnover rate suggests a need for more efficient inventory management to prevent potential writedowns.

Investor Takeaway: A Cautiously Optimistic Outlook

So, what does this detailed AMOREPACIFIC earnings analysis mean for potential investors? The Q3 2025 report paints a picture of a company in transition. The bull case for AMOREPACIFIC stock is built on the phenomenal success of its global diversification strategy, particularly in North America and Europe. The ability to acquire and successfully integrate a high-growth brand like COSRX is a significant long-term positive.

However, the bear case hinges on the persistent challenges in China and macroeconomic headwinds. The key for long-term growth will be the company’s ability to maintain its momentum in Western markets while simultaneously engineering a turnaround in China. Investors should monitor the sustainability of global growth, trends in the Chinese market recovery, and the company’s ongoing profitability management. While short-term volatility is likely, the strategic moves being made today could pave the way for substantial long-term value creation.