TKG Huchems Co., Ltd. (069260) recently unveiled its preliminary Q3 2025 financial results, presenting a complex picture for the investment community. The latest TKG Huchems earnings report revealed a significant shortfall in revenue against market consensus, yet simultaneously delivered an impressive operating profit that beat expectations. This divergence has left many investors wondering: Is this a sign of resilient operational efficiency or a warning of weakening demand?

This comprehensive analysis will dissect the Q3 2025 performance, explore the underlying macroeconomic currents, and evaluate the company’s strategic positioning. We aim to provide a clear, data-driven perspective to help you navigate the mixed signals and understand the future outlook for TKG Huchems stock.

While the top-line revenue weakness is a concern, TKG Huchems’ ability to expand profitability in a challenging environment showcases impressive cost discipline and strategic focus. The key question now is the sustainability of this trend.

Deep Dive into TKG Huchems Q3 2025 Earnings Performance

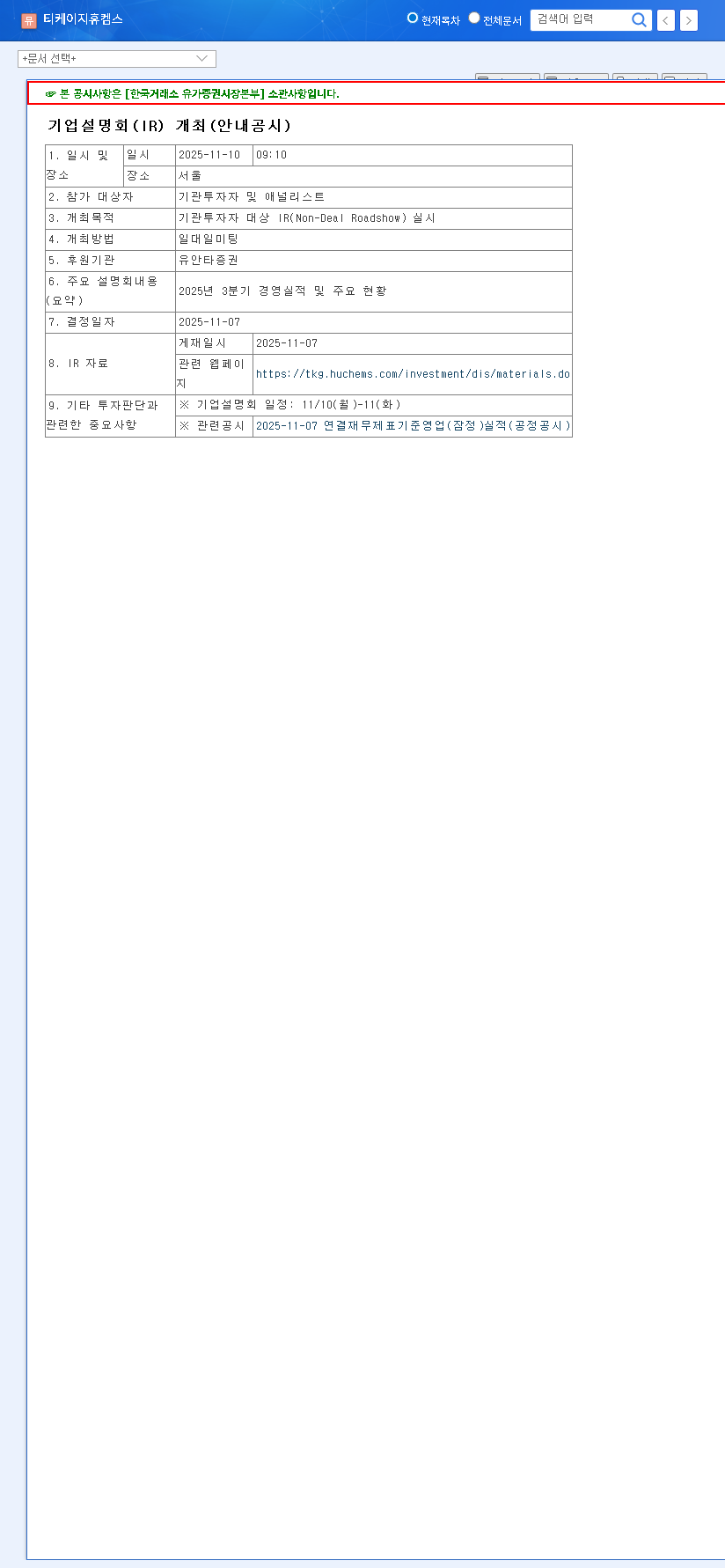

On November 7, 2025, TKG Huchems released its preliminary consolidated financial results, which can be verified via the Official Disclosure (DART). The numbers tell a story of two competing narratives.

The Headline Figures vs. Expectations

- •Revenue: KRW 291.7 billion. This figure fell short of the market consensus (KRW 332.1 billion) by a significant 12.0%. This points to persistent headwinds from a global demand slowdown, particularly affecting the company’s core NT (Nitrotoluene) series business which serves industries like construction and automotive.

- •Operating Profit: KRW 26.4 billion. In a surprising turn, this result surpassed market estimates (KRW 24.9 billion) by 6.0%. This outperformance suggests that internal cost control measures, production efficiencies, or a favorable shift in the product mix are effectively counteracting the weaker sales environment.

- •Net Profit: KRW 28.5 billion. The net profit came in even stronger than the operating profit, indicating positive contributions from non-operating activities. This could include gains on financial assets or favorable foreign exchange movements, though these are often one-time events.

Analyzing the Macro and Micro Factors

A company’s performance is never in a vacuum. The latest TKG Huchems earnings report is a direct reflection of both its internal strategies and the challenging external landscape.

The Global Economic Headwinds

The revenue miss is symptomatic of a broader trend reported by major financial outlets like Bloomberg. High interest rates in the U.S. (4.00%) and South Korea (2.50%) are designed to curb inflation but also slow economic activity, reducing demand for industrial chemicals. A volatile Won/Dollar exchange rate (avg. KRW 1,420 in Q3) creates a double-edged sword: it boosts the value of exports but increases the cost of imported raw materials, a critical factor for TKG Huchems’ profitability.

The Secrets to Profitability Resilience

How did the company beat profit forecasts? The answer likely lies in a combination of factors. Proactive cost management, renegotiated supplier contracts, and improved operational leverage from past investments are probable contributors. Furthermore, a strategic pivot towards higher-margin specialty products, even in small volumes, can significantly lift the overall profit margin. However, with raw material prices, linked to volatile oil prices, remaining a concern, the long-term sustainability of this high profitability requires close monitoring.

Strategic Outlook & Investor Action Plan

Looking beyond the quarter, an investor’s decision hinges on the company’s long-term strategy and its ability to navigate the chemical sector’s inherent cyclicality. The recent TKG Huchems stock analysis must weigh short-term challenges against long-term growth initiatives.

Pivoting for Future Growth

The company’s high dependency on the NT series highlights the need for diversification. Strategic investments in expanding the Nitric Acid Plant #6 and MNB Plant #2 are crucial steps. More importantly, R&D into high-value areas like P-PDA manufacturing for electronic materials could be a game-changer, reducing reliance on commoditized markets and building a more resilient business model for the future.

Considerations for Investors

- •Short-Term: The immediate focus should be on signs of revenue recovery. Watch for stabilization in global PMIs and downstream industry demand. The profit beat provides a cushion, but without top-line growth, the stock may remain range-bound.

- •Long-Term: The investment thesis rests on successful diversification. Monitor progress on new plant commissioning and the revenue contribution from new business segments. A successful transition to a specialty chemicals player could unlock significant value.

Frequently Asked Questions (FAQ)

Q1: What were the key takeaways from the TKG Huchems Q3 2025 earnings?

TKG Huchems reported Q3 2025 revenue of KRW 291.7 billion, missing estimates by 12.0%. However, its operating profit of KRW 26.4 billion beat expectations by 6.0%, showing strong cost management despite weak sales.

Q2: Why was operating profit strong if sales were weak?

The robust operating profit is attributed to successful internal initiatives, such as rigorous cost controls, production efficiency improvements, and a potentially more favorable high-margin product mix, which offset the negative impact of lower sales volume.

Q3: What are the primary risks for TKG Huchems stock?

The key risks include continued weakness in global demand affecting its core NT series business, volatility in raw material and energy prices, and the cyclical nature of the chemical industry which is tied to overall economic health.

Disclaimer: This analysis is based on publicly available information and is for informational purposes only. It is not intended as financial advice. All investment decisions should be made by the investor after conducting their own due diligence.