This comprehensive analysis of the Purit Co Ltd Q3 2025 earnings report provides investors with a critical look into the company’s performance, financial health, and future prospects. As Purit approaches its pivotal Investor Relations (IR) announcement, we will dissect the numbers, evaluate the impact of the booming semiconductor chemical market, and offer a detailed Purit investment guide to navigate what comes next.

Since its public listing in October 2023, Purit Co., Ltd. has captured significant market attention. With its upcoming earnings call, investors are keen to know if the company can sustain its growth trajectory and capitalize on the robust semiconductor industry. Let’s delve into the data to understand the full picture.

Official Q3 2025 Earnings Announcement Highlights

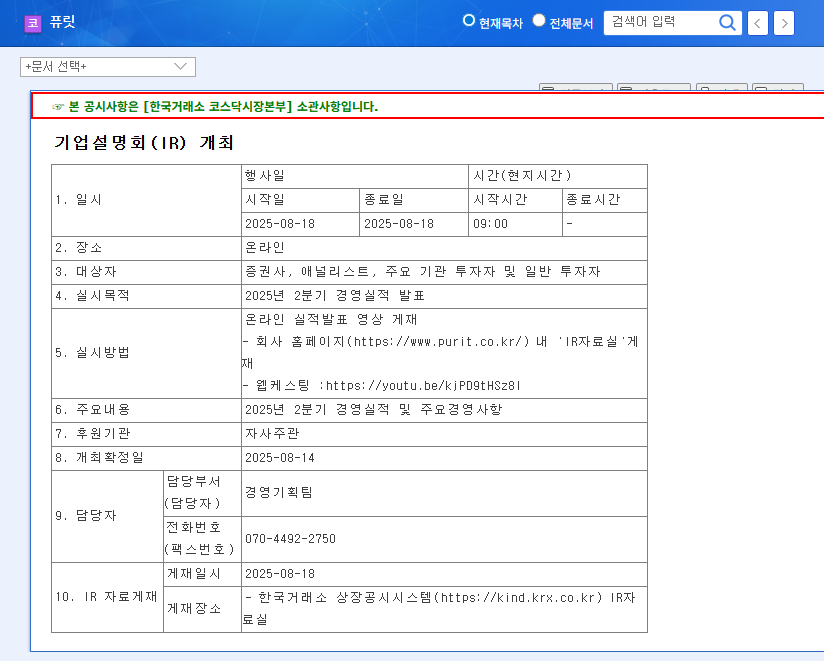

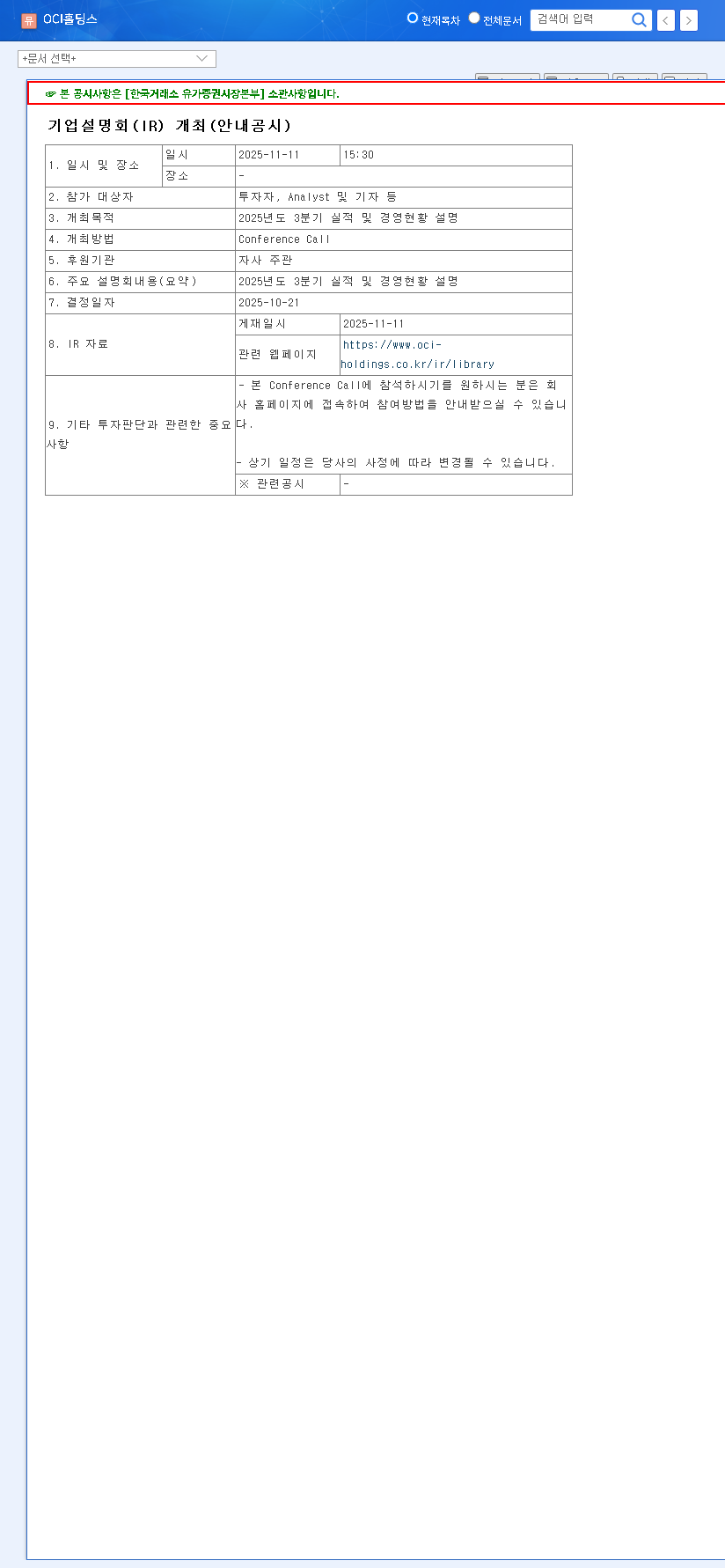

Purit Co., Ltd. has scheduled its official Investor Relations (IR) session for November 17, 2025, to present its third-quarter management performance and strategic business updates. This event is crucial for transparency and direct communication with shareholders. For a detailed look at the official filing, you can view the Official Disclosure on DART.

The market has shown cautious optimism, with Purit’s stock price gradually climbing in anticipation of this announcement. The Q3 results will either validate this positive sentiment or introduce a period of reassessment.

In-Depth Fundamental Analysis of Purit Co.

Business Performance: Riding the Semiconductor Wave

Purit’s growth story in 2025 is fundamentally tied to the health of the global semiconductor industry. The company’s core business, semiconductor chemicals, has been the primary engine of its expansion. According to market research from sources like Gartner, the demand for advanced semiconductors continues to surge, directly benefiting suppliers like Purit.

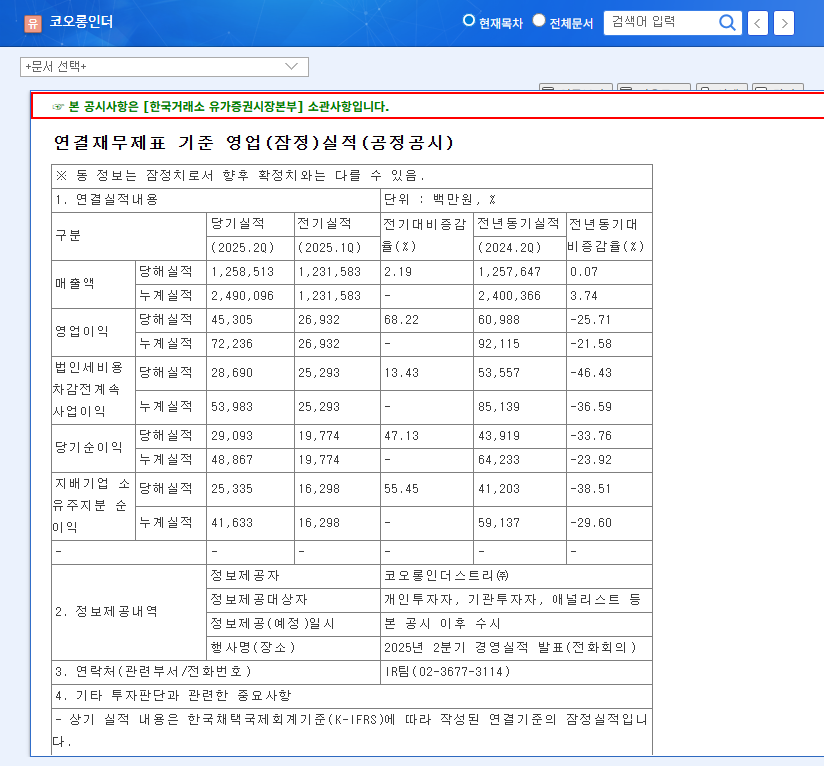

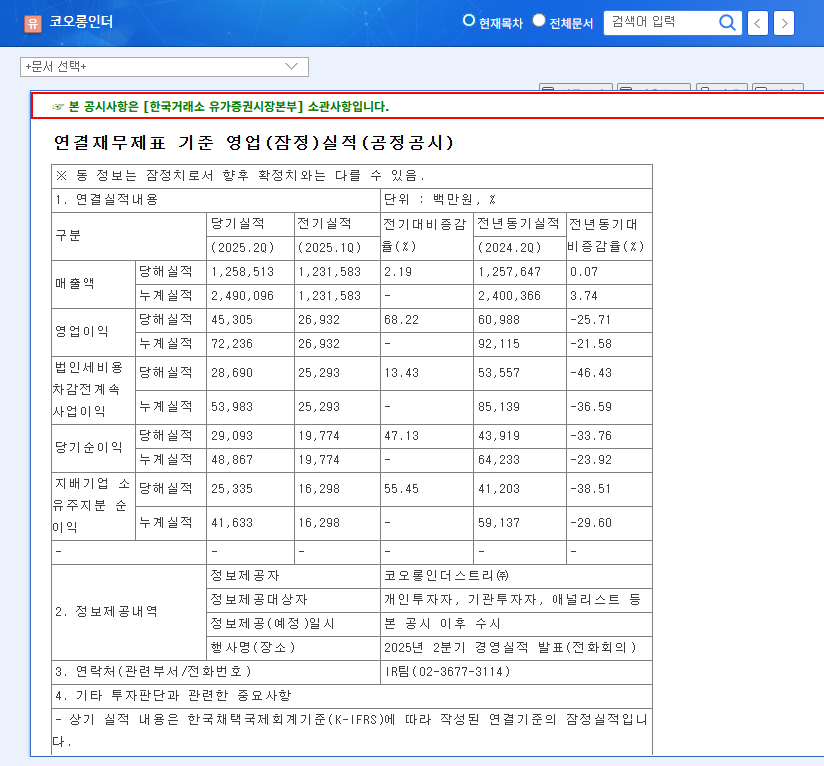

- •Impressive Revenue Growth: Cumulative revenue for Q3 2025 hit KRW 106.197 billion, a significant 13.2% increase year-over-year.

- •Semiconductor Dominance: The semiconductor chemical division contributed KRW 79.330 billion, making up a staggering 74.7% of total revenue.

- •Enhanced Profitability: Higher sales prices for its core products and stable raw material costs have improved margins.

- •Strategic Expansion: With a 73.8% utilization rate, the company is actively expanding capacity by building new distillation towers and securing a new factory site to meet future demand.

However, the business isn’t without its challenges. Sales in the display chemical sector have seen a notable decrease, largely due to the market’s shift from LCD to OLED technology. This highlights the need for strategic diversification, a key point investors will be watching in the Purit Co Ltd Q3 2025 earnings call.

Purit Financial Health: A Fortress Balance Sheet

A strong company needs a strong foundation. A close look at Purit financial health reveals a stable and well-managed enterprise capable of weathering economic shifts and funding future growth initiatives. The balance sheet provides a clear picture of this stability.

- •Growing Asset Base: Total assets climbed to KRW 117.864 billion.

- •Robust Cash Position: Cash holdings saw a major boost, reaching KRW 25.700 billion, providing excellent liquidity.

- •Low Leverage: The debt-to-equity ratio remains exceptionally low at just 13.59%.

- •Improving Margins: The operating profit margin improved significantly from 9.44% to 12.06%, demonstrating operational efficiency.

Future Outlook & Investment Strategy

The Bull Case: Why Investors are Optimistic

A positive Purit stock analysis hinges on the company’s ability to execute its growth strategy. If the IR confirms strong profitability and provides a clear roadmap for the new factory’s contribution, investor confidence could surge. Key catalysts include further penetration into the semiconductor chemical market, successful R&D breakthroughs, and enhanced corporate transparency, all of which would strengthen its long-term investment appeal.

The Bear Case: Risks to Monitor

Conversely, several risks could negatively impact the stock. If the Q3 earnings fall short of expectations, particularly if the decline in the display segment worsens, it could trigger a sell-off. Furthermore, vague or unconvincing plans for new business ventures could dampen enthusiasm. Investors must also remain vigilant of macroeconomic headwinds, including interest rate volatility and rising commodity prices, which could compress margins. For more on this, consider reading our analysis on the global supply chain’s impact on tech stocks.

Actionable Investment Recommendations

Based on this analysis, here are key recommendations for current and potential investors:

- •Analyze the IR Call: Pay close attention to management’s commentary on profit margins, the timeline for new facility operations, and specific details on R&D progress.

- •Monitor Macro Trends: Keep an eye on global interest rates, currency fluctuations, and oil prices, as these can directly affect Purit’s costs and profitability.

- •Watch for Diversification: The key to long-term, sustainable growth will be Purit’s success in developing new revenue streams to offset the decline in its legacy display business.

Disclaimer: This report is for informational purposes only and is based on publicly available data. Investment decisions should be made after consulting with a qualified financial advisor.