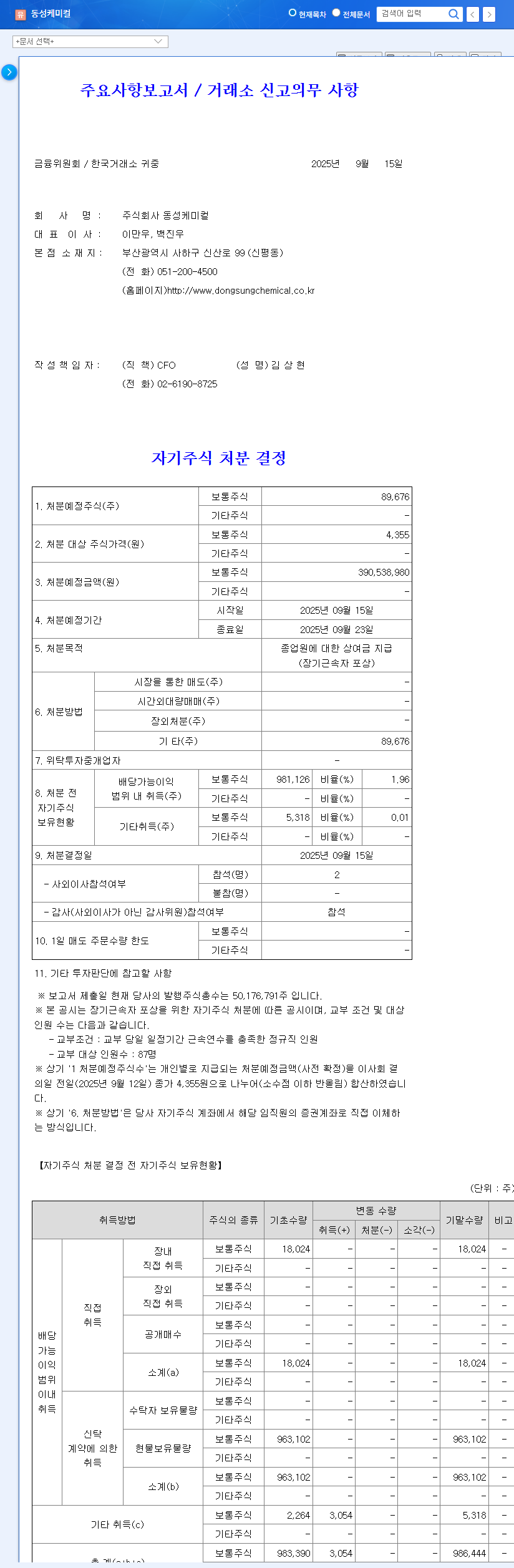

1. What Happened?: Treasury Stock Disposal Decision

DongSung Chemical announced the disposal of 89,676 treasury shares (0.18% of total outstanding shares) to fund employee bonuses. The purpose of the disposal is to reward long-term employees.

2. Why Dispose of Treasury Stock?: Background and Implications

This treasury stock disposal is part of a shareholder-friendly policy aimed at boosting employee morale and encouraging long-term service. It is expected to prevent the outflow of key personnel and enhance management stability. Due to the small size of the disposal relative to the total market capitalization, the short-term impact on the stock price is expected to be limited.

3. DongSung Chemical’s Future?: Growth Drivers and Investment Points

DongSung Chemical has a stable business structure with operations in chemicals (PU insulation, refrigerants, eco-friendly solvents) and bio (medical devices, derma cosmetics). In particular, the company has secured future growth engines, such as the strong performance of DongSung Finetec’s cryogenic insulation business driven by LNG market growth, and the development of eco-friendly and bio materials. However, continuous monitoring of macroeconomic conditions, such as exchange rate fluctuations and raw material price volatility, and the possibility of increased competition is necessary.

4. What Should Investors Do?: Action Plan

This treasury stock disposal alone is unlikely to significantly alter the investment outlook. However, considering DongSung Chemical’s business growth potential and efforts to secure future growth engines, a positive investment opinion can be maintained from a medium- to long-term perspective. It is important to develop an investment strategy while monitoring future announcements regarding additional treasury stock acquisitions or cancellations, and the realization of performance in key business segments.

Does treasury stock disposal negatively impact stock prices?

This treasury stock disposal is small in scale, so the short-term impact on the stock price is expected to be limited. It may even be positive for long-term growth by providing incentives to employees.

What are DongSung Chemical’s main businesses?

DongSung Chemical operates chemical (PU insulation, refrigerants, eco-friendly solvents) and bio (medical devices, derma cosmetics) businesses, and the growth potential of its LNG-related business is particularly promising.

Should I invest in DongSung Chemical?

This report is not an investment recommendation, and investment decisions should be made carefully based on individual judgment. However, DongSung Chemical has secured growth drivers and has a positive outlook in the medium to long term.