In a significant move for investors, ASIA HOLDINGS CO.,LTD (아세아) has announced a 4 billion KRW stock cancellation. This decision to retire treasury shares comes amidst challenging market conditions and raises critical questions for current and potential shareholders. What does this maneuver truly signal about the company’s confidence and future? This comprehensive analysis explores the implications of the ASIA HOLDINGS CO.,LTD stock cancellation, from potential short-term share price benefits to the underlying fundamental health of the company, providing strategic insights for your investment portfolio.

The 4 Billion Won Treasury Share Cancellation Explained

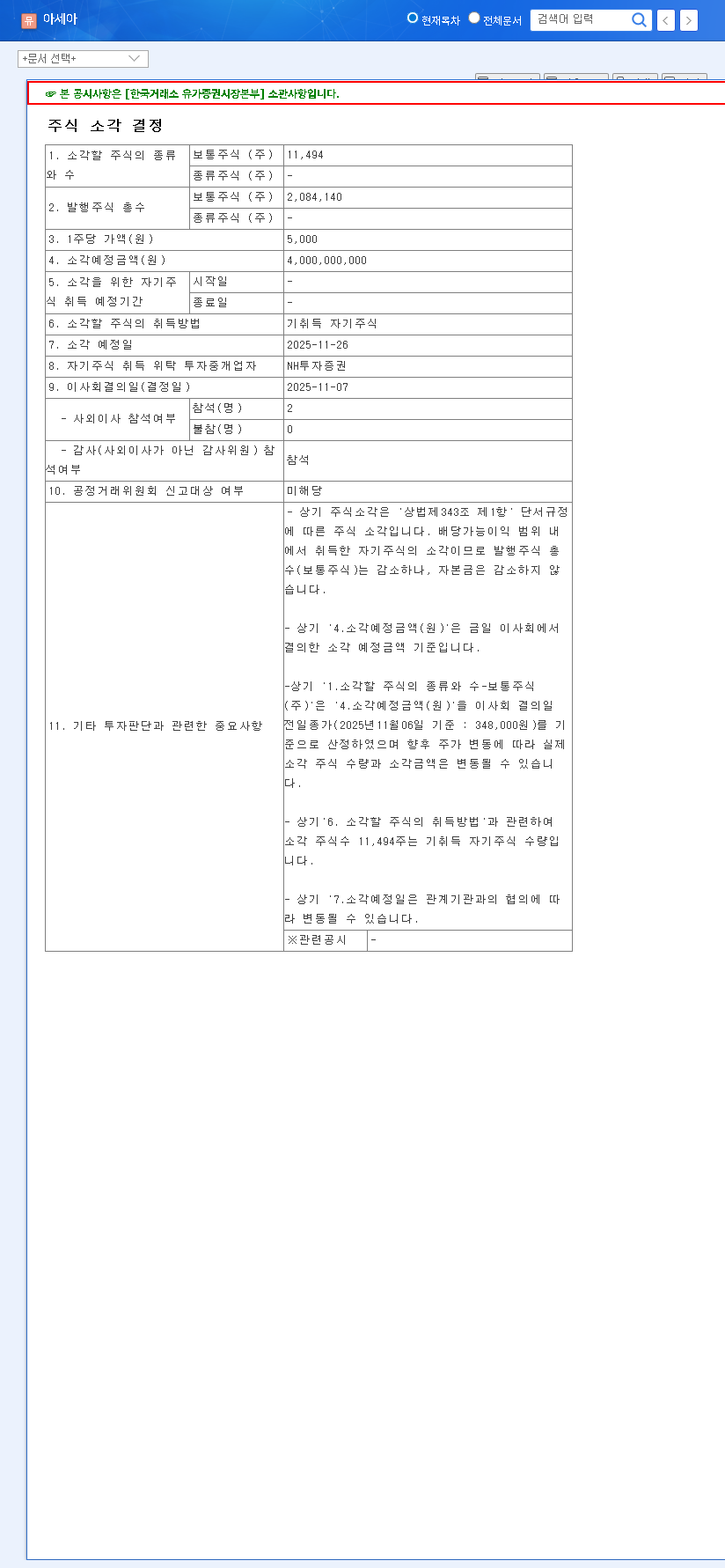

On November 7, 2025, ASIA HOLDINGS CO.,LTD formally announced its resolution to cancel 11,494 of its common treasury shares. This transaction, valued at approximately 4 billion KRW, is slated for completion on November 26, 2025. While this represents a modest 0.55% of the company’s 712.8 billion KRW market capitalization, the strategic timing and intent behind the move warrant a closer look. A treasury share cancellation is essentially a company buying back its own stock from the open market and then permanently retiring it, reducing the total number of shares outstanding. The official disclosure for this event can be found on DART, Korea’s electronic disclosure system (Source).

Context: Unpacking the Company’s Current Landscape

To fully grasp the significance of the stock cancellation, we must analyze the fundamental and market pressures ASIA HOLDINGS CO.,LTD is currently facing. The decision is not just about shareholder value; it’s a strategic response to a complex business environment.

Underperforming Business Segments

The first half of 2025 painted a challenging picture. The company reported sales of 935.4 billion KRW (an 8.1% decrease YoY) and an operating profit of 76.7 billion KRW (a sharp 33.8% decrease YoY). This downturn is not isolated to one area but stems from headwinds across its core operations:

- •Construction Market Downturn: The cement business has been significantly impacted, with low production utilization rates at ASIA Cement (58.8%) and Halla Cement (48.3%) directly hitting sales and profitability.

- •Paper Industry Stagnation: Weakening demand, rising raw material costs, and an industry-wide slowdown have squeezed margins in the paper division.

- •Cost and Currency Volatility: Fluctuations in raw material prices and foreign exchange rates have created significant cost-side pressure on the company’s core businesses.

- •Diversified Business Headwinds: Other ventures, including Wooshin Venture Investment and the Gyeongju World theme park, have also faced performance impacts due to changing investment climates and external factors.

Potential Impact of the Stock Cancellation

This treasury stock cancellation can create several ripples, affecting both stock valuation metrics and investor perception. Understanding these potential outcomes is key for any ASIA HOLDINGS CO.,LTD investment strategy.

The Bull Case: Enhancing Shareholder Value

- •Boost to Per-Share Metrics: By reducing the number of outstanding shares, the company mechanically increases its Earnings Per Share (EPS) and Book Value Per Share (BPS), making the stock appear more valuable on paper.

- •Increased Scarcity and Stability: A smaller float (the number of shares available for public trading) can increase the scarcity of the stock, potentially supporting the price and reducing volatility during market swings.

- •Signal of Confidence: This action is a classic shareholder-friendly policy. It signals to the market that management believes the stock is undervalued and is committed to returning value to its investors.

The Bear Case: Limitations and Realities

Despite the positives, investors should remain grounded. The cancellation’s scale (0.55% of market cap) is not substantial enough to single-handedly drive a massive price surge. Its direct impact may be limited and quickly priced in by the market. Furthermore, it represents a 4 billion KRW cash outflow, which, while manageable for the company, is still capital that could have been used for other growth initiatives. A deeper look into analyzing corporate financial health can provide more context.

While a positive signal, this stock cancellation is a tool, not a magic bullet. True long-term value will be driven by a fundamental recovery in ASIA HOLDINGS CO.,LTD’s core business operations.

Strategic Investment Approaches for ASIA HOLDINGS CO.,LTD

Given this complex backdrop, a one-size-fits-all investment strategy is ill-advised. Investors should tailor their approach based on their time horizon and risk tolerance.

For the Short-Term Trader

The announcement may create positive short-term momentum. Traders could capitalize on this sentiment, but it’s crucial to monitor trading volumes and price action closely. A strategy based solely on this news is risky without watching for signs of genuine improvement in the company’s quarterly reports.

For the Long-Term Investor

Long-term investors should view the stock cancellation as a minor positive in a much larger story. The key drivers for sustainable price appreciation lie in the recovery of the construction and paper markets. A patient, value-oriented approach is necessary. Watch for signs of stabilizing raw material prices and improving profit margins before committing significant capital.

Conclusion: A Cautious but Optimistic Outlook

The ASIA HOLDINGS CO.,LTD stock cancellation is a commendable step towards enhancing shareholder value and demonstrates management’s proactive stance. It provides a welcome, albeit small, tailwind for the stock. However, investors must weigh this against the significant macroeconomic and industry-specific headwinds the company faces. The path to sustained growth will be paved by fundamental business improvements, not just financial engineering. Therefore, a prudent, well-researched, and cautious investment approach is the most sensible path forward.

Frequently Asked Questions (FAQ)

Q1: What is a treasury stock cancellation?

A1: It’s when a company uses its cash to repurchase its own shares and then officially cancels them. This reduces the total number of shares in existence, which can increase metrics like Earnings Per Share (EPS) and signal management’s confidence in the company’s value.

Q2: Why is ASIA HOLDINGS CO.,LTD doing this now?

A2: The move is likely a strategic effort to boost investor confidence and support the stock price during a period of underperformance in its core cement and paper businesses, which are facing market downturns and cost pressures.

Q3: Will this stock cancellation guarantee the stock price goes up?

A3: No, it does not guarantee a price increase. While it is a positive factor that can create short-term momentum, the long-term stock performance will depend more heavily on the company’s ability to improve its financial results and navigate the challenging economic environment.