The recent announcement of the DGP convertible bond exercise has sent ripples through the investment community, raising critical questions about the company’s future stock price and financial stability. For shareholders and potential investors, understanding the mechanics and implications of this event is paramount. A convertible bond exercise isn’t merely a financial transaction; it’s a strategic move that can signal both risk and opportunity, directly impacting corporate value and investor returns.

This comprehensive analysis will dissect the DGP convertible bond exercise, providing an expert evaluation of its overview, the company’s fundamental health, the projected market impact, and a prudent investment strategy to navigate the path forward. Let’s delve into what this means for DGP’s trajectory in 2025 and beyond.

The Announcement: Unpacking the 33rd Convertible Bond Exercise

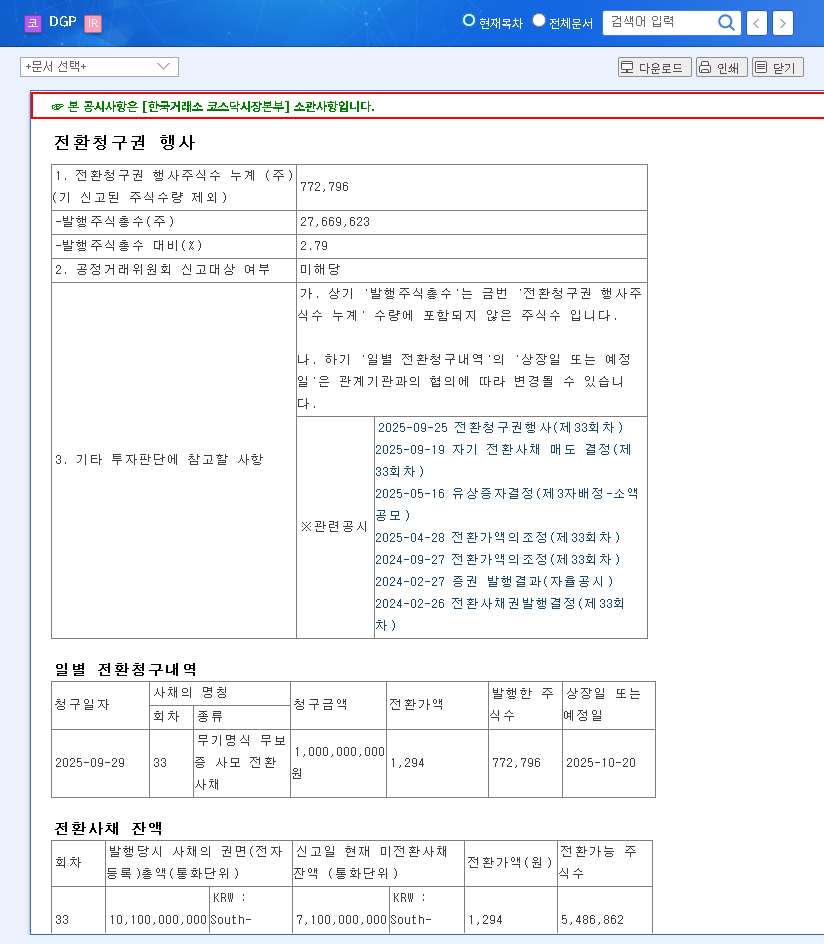

On September 29, 2025, DGP officially announced the exercise of its 33rd convertible bond (CB) call option. According to the Official Disclosure filed with DART, this action allows bondholders to convert their debt instruments into equity. In simple terms, debt is being swapped for new company shares. For a deeper understanding of the mechanics, you can review this guide on how convertible bonds work from a trusted financial source.

Key Details of the Conversion

- •Shares Claimed: 772,796 new shares, representing a 2.79% increase in market capitalization.

- •Conversion Price: KRW 1,294 per share.

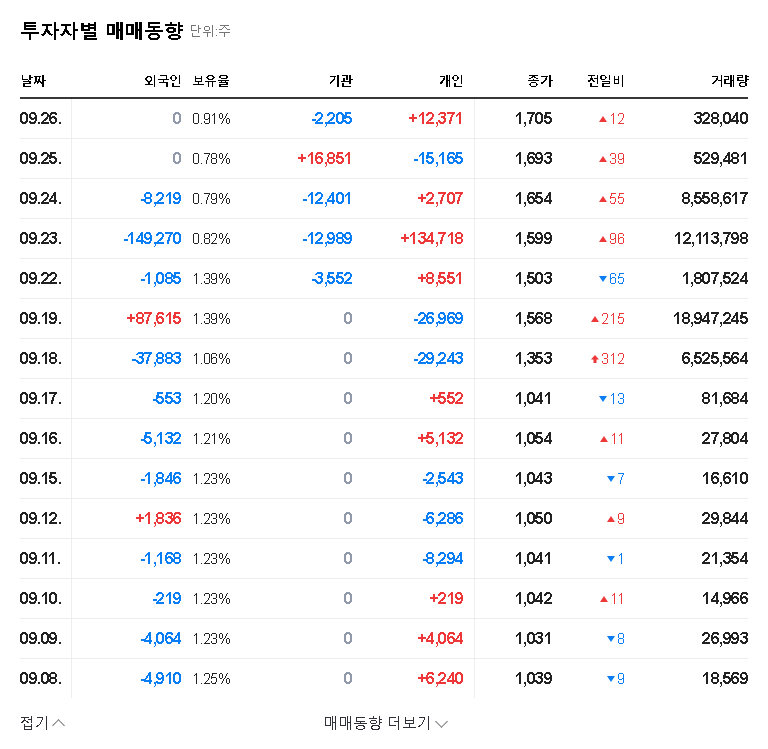

- •Current Stock Price (at time of announcement): KRW 1,588 per share.

- •Scheduled Conversion Date: October 20, 2025.

The significant gap between the conversion price and the current market price makes conversion highly attractive for bondholders, virtually guaranteeing that this new supply of shares will enter the market. This immediate share dilution is a central factor for current stockholders.

DGP Stock Analysis: A Company at a Crossroads

DGP’s core business revolves around renewable energy generation and EPC/O&M services. The company is strategically pivoting towards high-growth sectors like hydrogen, EV charging, and Energy Storage Systems (ESS). However, a deep fundamental DGP stock analysis reveals a tale of two opposing forces: promising growth potential versus significant financial risks.

Positive Catalysts: The Path to Growth

- •Future-Facing Ventures: Alignment with global green energy trends and supportive government policies provides a strong tailwind for its new ventures in hydrogen and EV charging.

- •Improving Financial Health: Recent data from H1 2025 shows efforts to deleverage, with a decrease in total liabilities and a lower net debt ratio.

- •Strategic Portfolio Management: The company is actively divesting non-core assets to streamline operations and focus capital on high-potential areas.

Negative Headwinds: Significant Risks to Overcome

- •Massive Accumulated Deficit: An undisposed deficit of KRW 102.47 billion is a major red flag, eroding shareholder value and financial stability.

- •Weak Operating Performance: In H1 2025, sales declined 39.27% while operating losses widened to -KRW 3.233 billion, signaling urgent operational issues.

- •High Investment Costs: New ventures require substantial capital (KRW 25.8 billion from 2025-2027), and intense competition could delay profitability.

Convertible Bond Impact on Stock Price

The convertible bond impact on DGP’s stock is a classic case of short-term pain versus potential long-term gain. Investors must weigh these conflicting outcomes carefully.

The core dilemma for investors is whether DGP’s long-term vision in renewable energy can outweigh the immediate negative pressure from share dilution and its current weak financial standing.

Short-Term Downward Pressure

The primary short-term effect is negative due to the share dilution. With nearly 773,000 new shares flooding the market, the value of each existing share is mathematically reduced. This dilution of earnings per share (EPS), combined with already poor performance and a large deficit, is likely to spook risk-averse investors and could trigger a sell-off, pushing the stock price down.

Long-Term Financial Improvement

Conversely, the long-term picture could brighten. By converting debt to equity, DGP improves its balance sheet. The debt-to-equity ratio decreases, and the company’s capital base is strengthened. This de-risking of the financial structure can make the company more attractive to long-term institutional investors and improve its ability to secure financing for its growth projects in the future.

Investment Strategy: A Prudent Action Plan for DGP

Given the complexities of the DGP convertible bond exercise, a cautious and highly analytical approach is essential. A speculative bet is ill-advised; instead, investors should adopt a monitor-and-verify strategy.

Investor Checklist for DGP

- •Adopt a Conservative Stance: The immediate negative factors likely outweigh the long-term positives. Avoid taking a large position until clear signs of a turnaround emerge.

- •Monitor Financial Health: Track quarterly reports for a reduction in the accumulated deficit and improvements in operating margins. To learn more, read our guide on How to Analyze a Company’s Balance Sheet.

- •Verify New Business Traction: Look for tangible evidence of success in the new ventures—signed contracts, revenue growth, and market share gains in EV charging, hydrogen, or ESS.

- •Assess Macroeconomic Winds: Keep an eye on interest rates, exchange rates, and regulatory changes in the renewable energy sector, as these external factors will heavily influence DGP’s success.

Conclusion: A Calculated Approach is Key

The DGP convertible bond exercise is a pivotal event that amplifies the company’s existing weaknesses while simultaneously paving a path toward a healthier financial future. The short-term outlook is fraught with risk due to share dilution and poor fundamentals. A sustainable stock price recovery is contingent on DGP’s ability to execute its growth strategy flawlessly and deliver concrete financial results. Investors should proceed with caution, armed with a long-term perspective and a commitment to diligently monitoring the company’s progress before making any significant capital commitments.