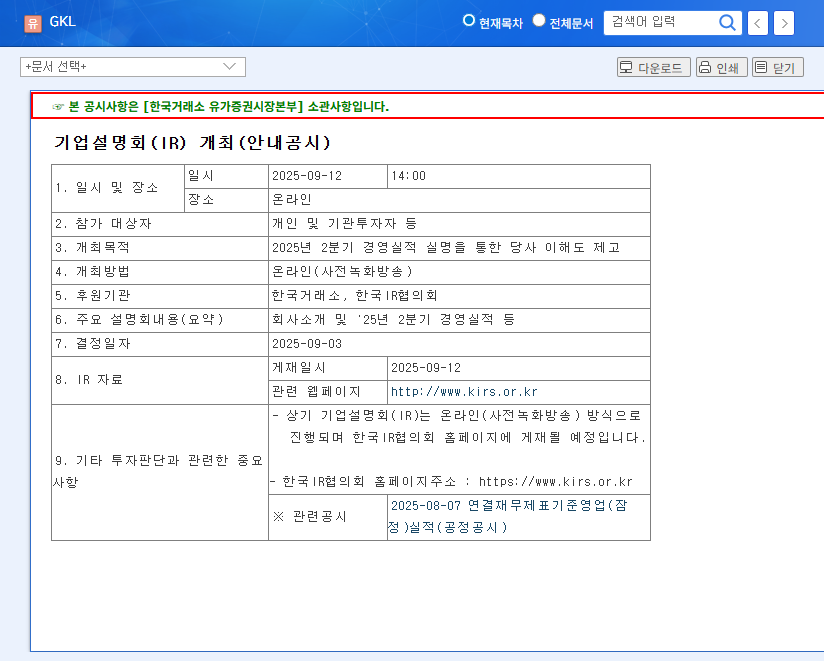

Investors are marking their calendars for November 18, 2025, as PARADISE.Co.,Ltd. (KRX: 034230), Korea’s premier integrated resort operator, prepares to host a pivotal Investor Relations (IR) conference. This upcoming PARADISE.Co.,Ltd. IR is more than a routine earnings call; it’s a critical juncture for the company to address pressing concerns about profitability and chart a clear course for future growth. The event will dissect the Q3 2025 earnings, review comprehensive half-year results, and unveil future management strategies that could profoundly influence the company’s valuation and stock performance.

This report provides a deep-dive PARADISE investor analysis, examining the company’s H1 2025 financial performance, the turbulent market environment, and the key questions that every stakeholder should be asking. From the paradox of rising revenue and falling profits to a significant cash flow reduction, we will uncover the essential insights needed to navigate your investment in PARADISE.

Deconstructing the H1 2025 Financial Performance

The first half of 2025 painted a complex picture for PARADISE.Co.,Ltd. While the top line showed healthy growth, the bottom line revealed significant pressures. This dichotomy is at the heart of investor uncertainty and will be a central theme of the upcoming PARADISE.Co.,Ltd. IR.

The core challenge for PARADISE is explaining how a 5.5% revenue increase led to a 24.7% drop in operating profit. Investors need clarity on cost control and future margin recovery.

Key Financial Metrics Unpacked

- •Revenue: Reached KRW 567.77 billion, a 5.5% year-over-year increase, fueled by the strong performance of its integrated resort division, which now accounts for over half of total revenue.

- •Operating Profit: Declined sharply to KRW 100.13 billion, a 24.7% decrease. The company attributes this to rising selling, general, and administrative (SG&A) expenses.

- •Net Income: Dropped by 38.3% to KRW 75.46 billion, impacted by higher financial costs and non-operating expenses.

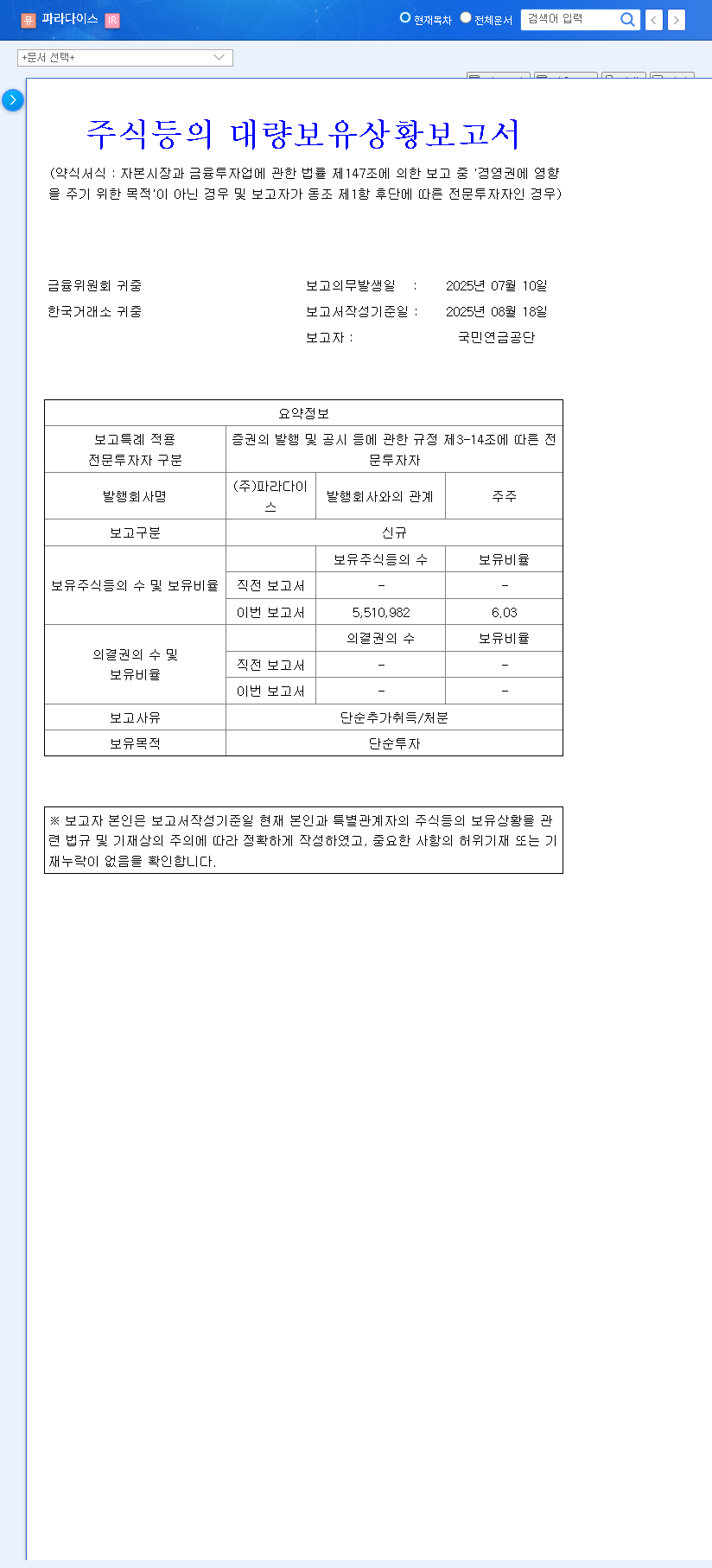

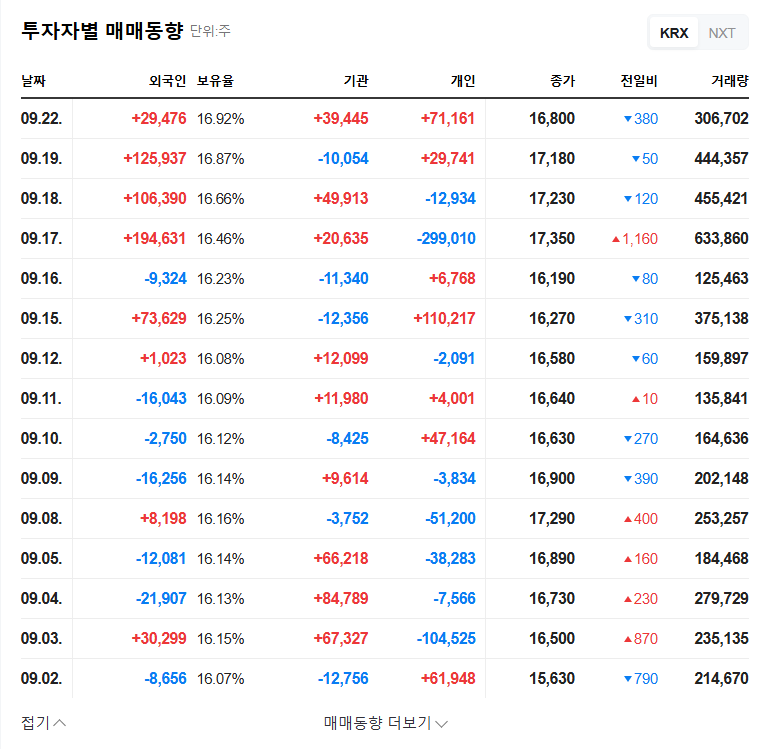

- •Cash Position: Cash and cash equivalents fell by a concerning 50.51% to KRW 287.94 billion, primarily due to investment outflows and dividend payments, raising questions about liquidity management.

Macroeconomic Winds: Challenges and Opportunities

PARADISE’s business is sensitive to global economic shifts. The current climate presents both tailwinds and headwinds. Interest rate cuts in the U.S. and Korea could lower financing costs and spur consumer spending. However, volatility in the USD/KRW exchange rate can impact the spending power of foreign VIPs and increase import costs. Similarly, rising commodity prices, as noted by sources like Reuters, could inflate operational costs. The company’s strategy to navigate this complex environment will be a key indicator of its resilience.

Investor Action Guide for the PARADISE.Co.,Ltd. IR

This IR event is a critical opportunity for due diligence. Investors should focus on the substance behind the numbers. A clear understanding of the company’s strategy is paramount, similar to what’s advised in our Guide to Investing in Korean Hospitality Stocks. Pay close attention to the following areas:

- •Profitability Restoration Plan: Demand a detailed, actionable plan for controlling SG&A expenses and improving operational efficiency to restore margins.

- •Core Business Growth: Scrutinize the strategy for sustaining growth in the integrated resort segment. What are the plans for attracting new demographics and competing in the region?

- •New Venture Viability: Assess the potential of new businesses, like the proposed liquor venture. Are these a distraction or a genuine path to diversified revenue?

- •Capital Allocation & Liquidity: Question the significant drop in cash reserves. What is the future capital allocation strategy, and how will financial health be maintained? For raw data, refer to the Official Disclosure.

Frequently Asked Questions (FAQ)

Q1: What is the main concern with PARADISE’s H1 2025 financial performance?

The primary concern is the significant decline in profitability despite revenue growth. Operating profit fell 24.7% and net income fell 38.3%, mainly due to increased administrative expenses and financial costs, signaling potential issues with cost control.

Q2: What should investors listen for during the PARADISE Q3 earnings call?

Investors should listen for a clear, convincing strategy to improve cost efficiency, specific plans for managing liquidity after the large cash decrease, and a realistic outlook for the core integrated resort business.

Q3: Are there any positive catalysts for the 034230 stock?

Yes. Positive catalysts include the robust growth of the main integrated resort division, the company’s recent move to the KOSPI market which could attract more institutional investors, and potential success from new business diversification like the liquor segment.

Ultimately, the upcoming PARADISE.Co.,Ltd. IR will be a test of management’s transparency and strategic foresight. The ability to provide credible answers and a confident vision will be pivotal in rebuilding investor trust and shaping the future trajectory of the 034230 stock.