The GC CELL FUCASO deal has sent ripples through the biotech investment community. In a strategic move to bolster its pipeline, GC CELL CORPORATION (GC CELL) has secured exclusive domestic rights to ‘FUCASO’, a promising CAR-T cell therapy for multiple myeloma. This pivotal agreement represents a significant gamble—one that could secure its position as a leader in next-generation cell therapies or exacerbate its existing financial pressures.

For investors, this news presents a classic high-risk, high-reward scenario. While the potential for a breakthrough multiple myeloma treatment is immense, the path to commercialization is fraught with clinical uncertainty and substantial costs. This comprehensive analysis will dissect the opportunities and risks tied to the GC CELL FUCASO agreement, providing a clear, data-driven investment perspective for 2025 and beyond.

Unpacking the FUCASO Agreement: What Investors Need to Know

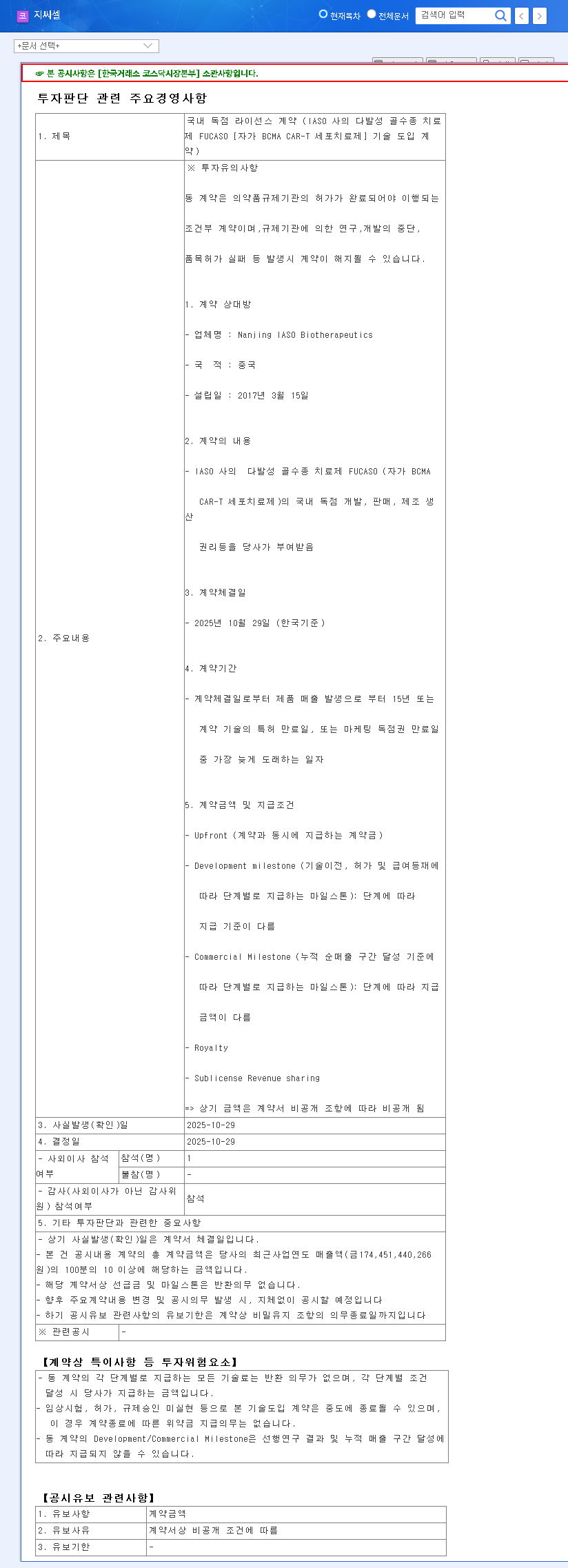

On October 29, 2025, GC CELL announced a technology licensing agreement with China’s Nanjing IASO Biotherapeutics. This deal grants GC CELL the exclusive rights to develop, manufacture, and commercialize FUCASO within South Korea. The move is a clear signal of GC CELL’s ambition to become a major player in the cutting-edge field of CAR-T cell therapy.

What is FUCASO? A Primer on CAR-T Technology

FUCASO is an autologous BCMA CAR-T cell therapy. In simple terms, CAR-T cell therapy is a revolutionary form of immunotherapy where a patient’s own T-cells (a type of immune cell) are extracted, genetically engineered in a lab to recognize and attack cancer cells, and then reinfused back into the patient. FUCASO specifically targets the BCMA protein, which is commonly found on the surface of multiple myeloma cells, making it a highly targeted and potent potential treatment.

The Fine Print: A Conditional Contract

A critical detail for investors is the conditional nature of the agreement. The deal’s continuation is contingent upon successful clinical development and regulatory approval. This means that if FUCASO fails to meet clinical endpoints or is rejected by regulatory bodies like the Ministry of Food and Drug Safety (MFDS), the contract could be terminated, potentially leading to a significant loss of invested capital. The complete terms can be reviewed in the Official Disclosure (DART).

The Bull Case: Potential for Exponential Growth

Despite the risks, the upside of the GC CELL FUCASO deal is substantial. Successfully bringing this therapy to market could transform the company’s trajectory.

- •Pipeline Enhancement: Acquiring FUCASO diversifies GC CELL’s pipeline with a high-value, next-generation asset, reducing reliance on existing revenue streams.

- •Market Leadership: A successful FUCASO launch could establish GC CELL as a leader in the lucrative oncology and cell therapy market in South Korea.

- •Synergistic Opportunities: GC CELL can leverage its existing experience in cell therapy development and its CDMO (Contract Development and Manufacturing Organization) business, creating powerful operational synergies. You can learn more about their comprehensive CDMO capabilities here.

The Bear Case: Navigating Financial and Clinical Headwinds

Conversely, the path forward is laden with significant challenges that warrant a cautious approach from investors evaluating GC CELL stock.

The high cost of CAR-T development, combined with GC CELL’s ongoing operating losses, creates a precarious financial situation that cannot be overlooked. Clinical success is not guaranteed.

Persistent Financial Strain

GC CELL’s financial health is a primary concern. As of the first half of 2025, the company reported an operating loss of KRW 9.07 billion and a net loss of KRW 27.43 billion. These expanding losses, coupled with rising short-term borrowings, raise questions about the company’s ability to fund the costly development of FUCASO without further diluting shareholder value or taking on unsustainable debt.

Intense Market Competition

The global CAR-T market is fiercely competitive. Numerous major pharmaceutical giants and agile biotech firms are developing their own therapies. GC CELL will need to demonstrate superior efficacy, safety, and a clear path to market to compete effectively against established and emerging players.

Investment Outlook: A ‘Hold’ Recommendation

Considering the balance of immense long-term potential against severe short-term financial and clinical risks, a ‘Hold’ recommendation for GC CELL stock is prudent at this time. Investors should closely monitor several key developments before reassessing their position.

- •Clinical Trial Data: Any release of FUCASO’s clinical data from IASO Biotherapeutics will be a major catalyst.

- •Regulatory Milestones: Progress with the Korean MFDS will be a critical indicator of the timeline to commercialization.

- •Financial Management: Watch for the company’s strategy to fund development and improve its underlying profitability from existing businesses like ‘Immuncell-LC Inj.’

In conclusion, the GC CELL FUCASO agreement is a defining moment for the company. While the ambition is commendable, the execution risk is high. Cautious observation is the best course of action until the company provides tangible proof of clinical success and a clear path to financial stability.

Disclaimer: This report is for informational purposes only and does not constitute investment advice. All investment decisions must be made at the investor’s own discretion and responsibility.